- Mills delay purchases due to poor rebar sales

- Procurement pause likely to last till late Jul’25

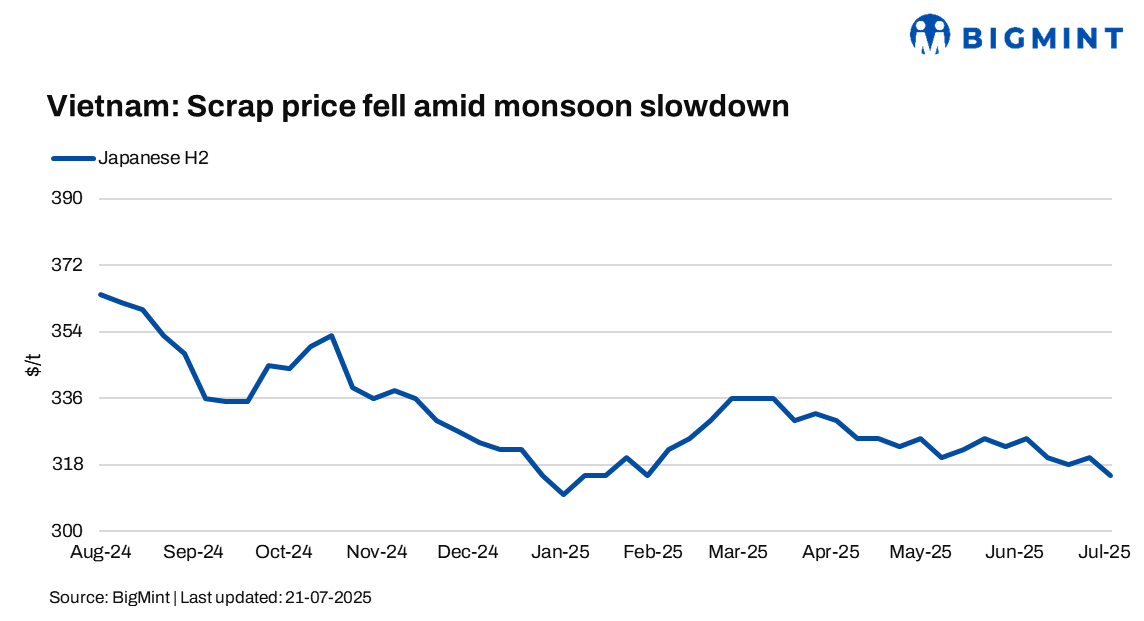

Imported ferrous scrap prices in Vietnam declined by up to $5/tonne (t) w-o-w, with persistent monsoon disruptions and sluggish demand continuing to suppress market activity.

Japan, Vietnam’s top ferrous scrap supplier, also faced subdued interest despite a weaker JPY that typically supports exports. Market participants attributed the muted demand to summer production cuts and ongoing trade uncertainties across Asia.

Weekly assessments

- Japanese H2 scrap was at $315/t CFR, down $5/t w-o-w.

- US-origin HMS 80:20 bulk stood at $335/t CFR Vietnam, also down $3/t w-o-w.

Market updates

H2 scrap offers were heard at $315-320/t CFR, while mill bids stayed at around $310/t. Domestic rebar sales continued to underperform, dampening mills’ buying appetite.

A trader commented, “Scrap demand in neighbouring South Korea, Taiwan, and Bangladesh has been weak, so more material is being redirected to Vietnam, putting pressure on local scrap prices.”

Offers for HMS 80:20 from the US remained firm at $340/t CFR Vietnam, narrowing slightly from the prior week’s $335-345/t range. Mills raised their bids to $330/t CFR, up from $325-330/t last week, although deals remained limited.

Domestic market

Vietnam’s domestic scrap market also remained quiet this week, with ongoing monsoon-related disruptions weighing on demand for finished steel. This, in turn, softened scrap consumption across much of the country.

Another participant said, “Rebar sales are very weak right now in Vietnam, and with sufficient scrap inventories mills are holding off purchases amid low production levels.”

Finished product demand is slow in the North and Central regions due to the seasonal rains, but government-driven infrastructure projects continue to support demand in the South.

A Vietnam-based source informed, “In the North, rebar sales are weak and inventories are high, so mills are avoiding new purchases. Some mills have paused procurement altogether and may resume buying by late July.”

Outlook

With rebar demand likely to stay muted in the short term and weather disruptions persisting, imported scrap prices may remain under pressure. Any notable recovery will hinge on a pickup in downstream demand and reduced availability from key suppliers later this quarter.

Leave a Reply