- Hindustan Zinc’s Q1 FY26 profit down 4.7%

- Asian demand firm but downstream concerns linger in China, EU

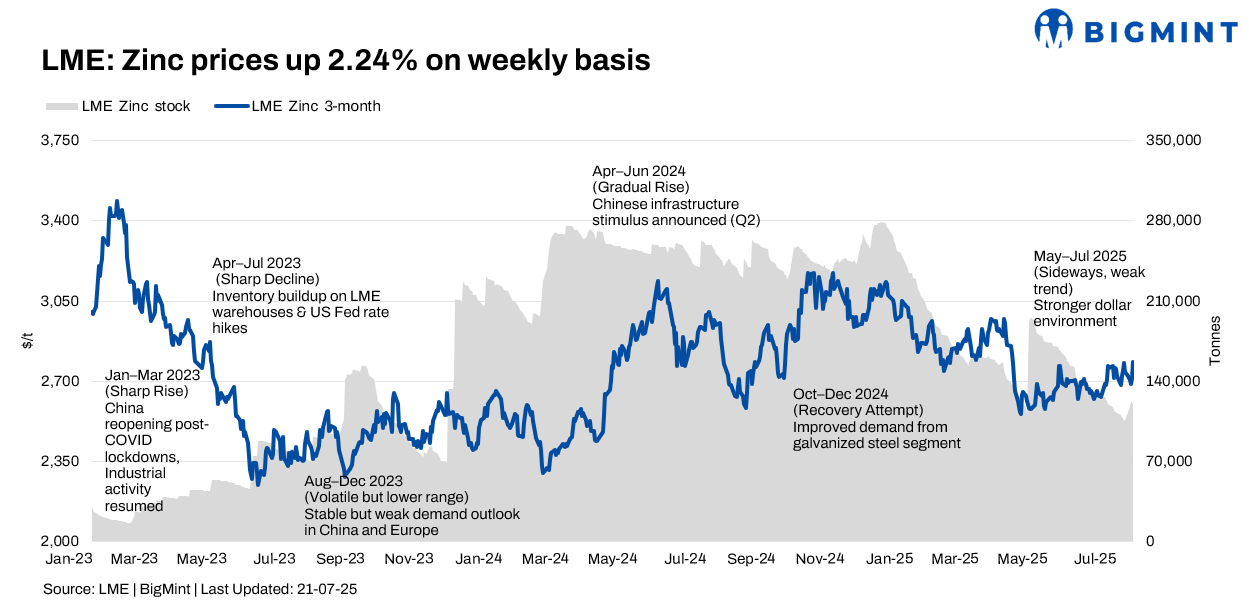

Zinc prices on the London Metal Exchange (LME) saw a slight decline during week 29 (14-18 July 2025), as increasing inventories and higher treatment charges (TCs) signalled improved refined metal supply. Meanwhile, demand stayed stable across Asia and the Middle East, keeping prices supported but within a tight band.

Prices up 2.24%, inventories dip

LME zinc cash-settlement prices began the week at $2,711/t on 14 July, dropping to a low of $2,677/t on 16 July. Prices rebounded in the latter half of the week, reaching $2,780/t on 18 July, an increase of 2.92% from the previous day’s close.

The three-month LME Zinc contract also mirrored this pattern, starting at $2,721/t on 14 July and closing the week at $2,782/t on 18 July.

LME Zinc stocks initially saw a significant increase on 14 July, rising by 8,150 t to 113,400 t. This inventory buildup initially eased supply concerns and contributed to the price decline early into the week. However, LME inventory subsequently decreased, falling to 119,100 t by 18 July.

MCX zinc trends (14-18 July)

MCX zinc prices initially declined, closing at 258.6 on 14 July due to demand concerns. However, prices recovered, closing higher at 258.55 on 18 July driven by short covering as supply constraints became apparent. Over the week, MCX zinc futures saw a net positive movement of 5.65 points, reflecting a cautiously optimistic sentiment.

Hindustan Zinc’s performance

Hindustan Zinc’s Q1 FY26 profit fell by 4.7% to INR 2,234 crore, with revenue down 4.4%. Despite this decline, the company reported its highest-ever first mined metal production in the quarter. The company also announced a phase-1 expansion project to double its capacity, indicating a positive long-term outlook.

Market factors

A generally positive macroeconomic sentiment emerged during the week, driven by better-than-expected US retail sales data for June and renewed calls from President Trump for the US Fed to cut interest rates. This positive macro environment outweighed concerns related to potential tariffs and supported LME zinc price increases.

The SHFE/LME price ratio continued to hover around the 8.1 mark, keeping the zinc ingot import window into China closed.

Downstream demand, particularly in the Chinese galvanising sector, reportedly remained lacklustre, contributing to the rise in domestic inventories. Indian zinc demand was mostly flat w-o-w. While production remained stable, buyers continued to operate on hand-to-mouth inventory models amid cautious sentiment.

Outlook

Zinc prices are expected to continue trading in a range of $2,680-2,780/t in the near term. Rising treatment charges, higher LME inventories, and steady-but unspectacular-demand suggest limited upside potential unless major smelter outages or fresh stimulus measures emerge.

Leave a Reply