- Tight vessel supply supports freights

- Baltic index hits 1-month high

Dry bulk coal freight rates to India witnessed mixed trends this week. Panamax rates inched down slightly w-o-w on the Australia-India route while South Africa-India route reported a w-o-w rise. Meanwhile, Supramax rates on the Indonesia-India corridor also moved higher on a weekly basis.

“The monsoon season continues to influence market activity in India, with some cargoes currently being deferred”, a source informed BigMint.

Another source from the industry said, “The freight market continues to show strength, primarily driven by robust grain exports from East Coast South America (ECSA). This surge in agricultural cargoes, particularly corn and soybeans from Brazil and Argentina, has tightened vessel availability in the region. As a result, freight rates have remained elevated, with charterers competing for limited tonnage. The seasonal peak in grain shipments, combined with steady demand from key importers such as China and Southeast Asia, is sustaining upward pressure on Panamax freight rates and overall market sentiment.”

Indian scenario

However, India’s demand has remained subdued, primarily due to slower offtake at ports and lower consumption levels, largely driven by heavy rainfall across regions.

Interestingly, demand for non-coking coal imports for India’s power sector is declining, driven by government initiatives to boost domestic production and supply. However, industrial sectors are increasingly seeking high-grade, low-ash imported coal, leading to a surge in demand from that segment.

Supporting the trend of declining demand, India’s non-coking coal imports – mainly used in power generation and industrial sectors – fell to 89 million tonnes (mnt) in January-June 2025 (H1CY’25), marking a y-o-y drop of over 4% from 93 mnt in the same period last year, as per provisional data from BigMint.

In June alone, imports fell sharply by 14% m-o-m to approximately 15.52 mnt, compared to 18.5 mnt in May. For the full calendar year 2024 (CY’24), India’s total non-coking coal imports reached over 173 mnt, reflecting a slight y-o-y decline of 1.16%.

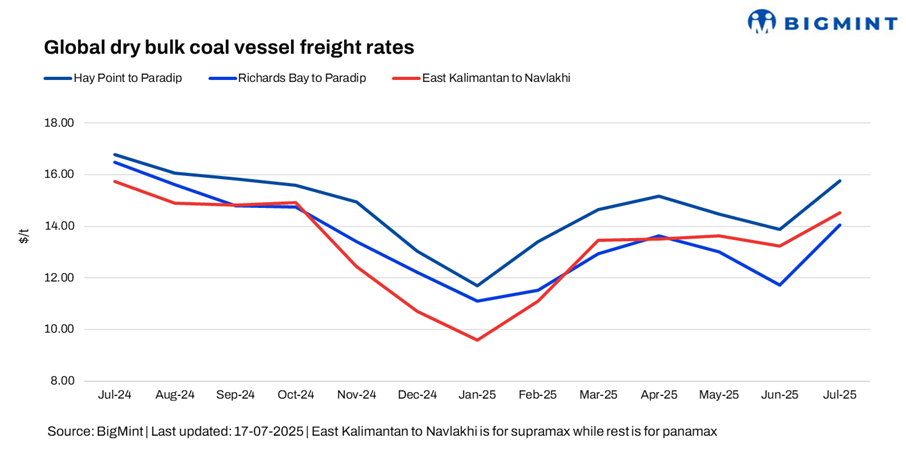

Route-wise updates

- Australia (Hay Point)-India (Paradip), Panamax: Freight rates from Australia to India decreased marginally by $0.2/dry metric tonne (DMT) w-o-w, with BigMint’s latest assessment placing the Hay Point to Paradip route at $15.90/DMT. Indian buyers, especially blast furnace operators, were actively procuring coking coal at significantly higher prices earlier in the week, which helped keep freight rates elevated. However, rates began to ease midweek as some fixtures were concluded at lower levels. Indian BF-based steel producers have started diversifying their coking coal import sources, with Russian cargoes gaining traction due to highly competitive prices amid ongoing sanctions. This shift is also reducing their dependence on Australian premium hard coking coal (PHCC).

- South Africa (Richards Bay)-India (Paradip), Panamax: Freight rates from Richards Bay Coal Terminal (RBCT) to Paradip edged up by $1.45/DMT w-o-w, reaching $15.05/DMT. Panamax freight rates for South African coal to India have risen despite subdued market activity, primarily due to logistical challenges and ongoing maintenance at the Richards Bay Coal Terminal (RBCT). A source noted, “Freights remain elevated amid logistics issues in South Africa, with RBCT undergoing maintenance for around 25 days, leading to a vessel shortage.”

Furthermore, portside offers for South African RB2 (5500 NAR) thermal coal in India edged higher w-o-w, supported by rising sponge iron prices and improved trader sentiment. The domestic sponge iron market witnessed an upward trend, with pellet-based and lump-based prices climbing by INR 100-300/tonne (t) ($1-3/t) d-o-d across major trading hubs.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Coal freight rates from East Kalimantan to Navlakhi rose by $1.47/DMT w-o-w, settling at $15.58/DMT. In the Indonesian market, strong cargo demand amid limited vessel availability continued to support freight rates. However, trading activity on the Indonesia-India coal route remained relatively muted amid lower bids, with limited information reported.

Meanwhile, portside thermal coal inventories in India remained largely stable in Week 28, standing at 15.84 mnt compared to 15.92 mnt the previous week. In Navlakhi, stocks edged up by 7% to 0.94mnt, data maintained with BigMint shows.

Baltic index hits 1-month high

The Baltic Exchange’s main sea freight index rose to a one-month high, driven by a sharp increase in Capesize vessel rates. The index, which tracks Capesize, Panamax, and Supramax segments, climbed 40 points to 1,906 – its highest since 17 June.

However, performance across vessel classes was mixed, with the Panamax index slipping 23 points to 1,967, while the supramax index gained 28 points to reach 1,315.

Outlook

In the near term, dry bulk coal freight rates are likely to stay firm to slightly bullish, supported by seasonal stockpiling in India during the monsoon, tighter vessel availability amid increased activity from regions like ECSA, and vessel allocation towards grain shipments during the season.

Despite subdued demand from key sectors like cement and power amid the ongoing monsoon, stable portside inventories and weather-related delays are expected to tighten vessel supply. Consequently, Panamax rates on routes such as Australia-India and South Africa-India may witness moderate gains, while Supramax rates on the Indonesia-India corridor likely to remain steady to slightly firm.

Leave a Reply