- Benchmark Mumbai HRC prices drop INR 700/t

- Prices may drop further by month-end

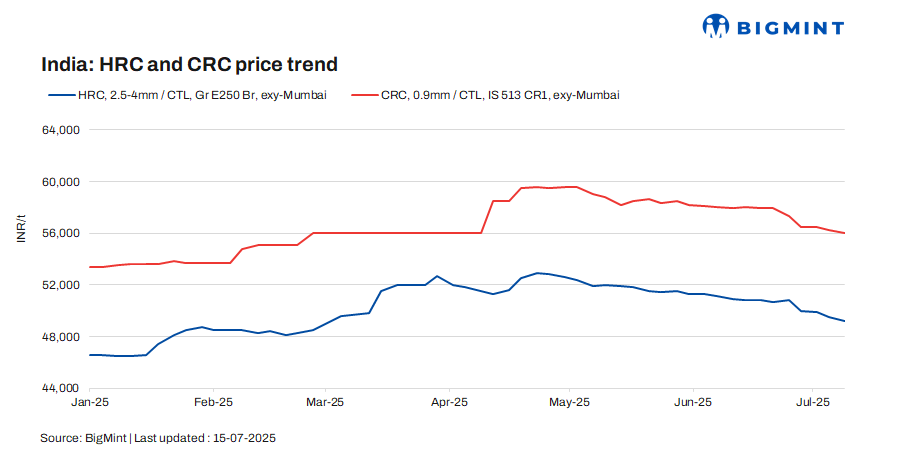

Trade-level prices of hot-rolled coils (HRCs) in India declined by up to INR 500/tonne (t) w-o-w to INR 49,200-51,400/t ($574-599/t) across markets. Moreover, cold-rolled coil (CRC) prices dropped by INR 800/t w-o-w to INR 55,000-59,500/t ($641-694/t).

BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) dropped by INR 700/t ($8/t) w-o-w to INR 49,200/t ($574/t) on 15 July 2025 against INR 49,900/t ($582/t) a week ago. On the other hand, CRC (IS513, Gr O, 0.9 mm/CTL) prices declined by INR 500/t ($6/t) w-o-w to INR 56,000/t ($653/t) on Tuesday against INR 56,500/t ($659/t). These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Market updates

Market sees demand slowdown: Market sentiment remains subdued as demand continues to be lacklustre, with no visible signs of recovery. Inventory levels at the distributor end also remain elevated, reflecting slow offtake. In response, buyers are largely adopting a “wait and watch” stance, anticipating a potential correction in prices before making fresh purchases.

“The market remains under significant pressure and is showing clear signs of weakness. Given the current downward trend, prices are likely to decline further, potentially reaching pre-safeguard duty levels. Based on prevailing indicators, HRC (CTL) prices may drop to around INR 48,000/t by the end of the month. The only potential support in the near term could come from a brief restocking window expected between Ganesh Chaturthi and Navratri,” a market participant noted.

Liquidity concerns impact purchases: Distributors and buyers are facing financial stress, marked by delayed payments and tighter cash flow.

“The ongoing financial strain is becoming increasingly evident across the market. Delayed payments and tight liquidity conditions are significantly hampering purchases. In many cases, transactions are now being executed on highly flexible payment terms – commonly referred to as “payable when able” – where buyers lift the material with deferred payment commitments, reflecting the prevailing cash flow challenges in the system,” a market participant informed BigMint.

Import volumes: India’s bulk imports of HRCs touched 201,211 t as of 12 July, based on vessel line-up data. Around 222,398 t of additional cargo are expected by the month-end.

Export volumes: India’s bulk exports of HRCs touched 43,357 t as of 12 July, based on vessel line-up data with BigMint.

Indian HRC export offers to the EU fell amid subdued European demand. Moreover, Indian mills held back offers due to strong domestic demand and overseas competition.

Outlook

In the near term, Indian HRC and CRC prices may stay under pressure due to weak seasonal demand, high inventories and liquidity constraints. Moreover, buyers remain cautious amid expectations of further price cuts and limited restocking interest.

Leave a Reply