- Spot sentiment cautious, global cues mixed

- HZL increases offers by INR 5,800/t

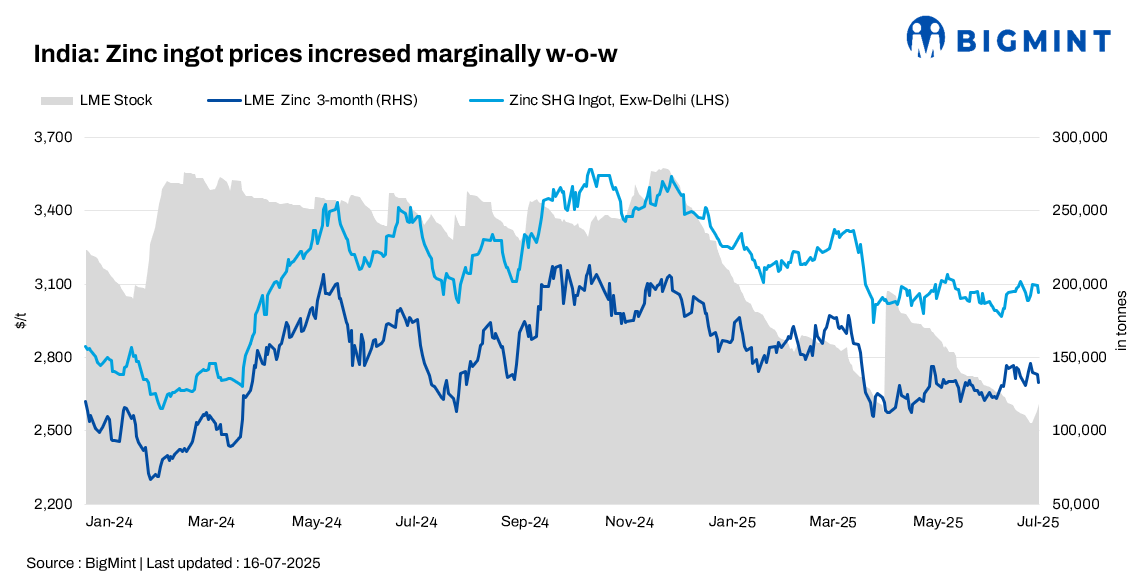

Zinc ingot (99.995%) was assessed at INR 263,000/t ex-Delhi, up by INR 3,000/t w-o-w, according to BigMint.

On 14 July 2025, Hindustan Zinc Limited (HZL) raised its zinc ingot price by INR 5,800/t ($67/t) to INR 278,100/t ($3,234/t), citing raw material shortages. This move was largely sentiment-driven, with limited impact on spot market transactions, which remained conservative.

Traders reported HZL SHG ingot was traded at INR 262,000-263,000/t ex-Delhi, while Australian zinc continued to attract a notable premium, quoted at INR 294,000-295,000/t due to its high-grade quality and tighter import availability.

In the import market, traders noted that non-duty zinc ingot premiums stood at $145-155/t CIF Nhava Sheva over LME. For domestic zinc, premiums hovered around $168/t on an ex-plant basis, excluding 5.5% import duty – highlighting stronger buying interest for duty-free cargoes. However, space constraints on vessels persist, with no space confirmations available for the remainder of July.

Market comments

“There is still no urgency in the market. Bulk buying has not resumed, and most downstream players are running lean due to liquidity constraints and seasonal slowdowns,” said a trader in Ghaziabad.

“Buyers are confused. HZL has raised prices, but demand has not picked up yet. Traders are hesitant about inventory given the sluggish offtake,” said a Delhi-based zinc distributor.

Global zinc futures snapshot

As of 15 July, LME 3-month zinc traded in the $2,697/t range, reflecting continued caution amid weak global macroeconomic indicators. SHFE zinc August contract was at RMB 22,105/t, slightly lower from last week as Chinese demand showed limited recovery. On MCX, zinc August futures moved in the INR 254,000-256,500/t band. Participants remained cautious due to low offtake and sluggish restocking trends.

Outlook

The domestic zinc market continues to face weak demand, with buyers expected to remain cautious in the short term. Hopes are pinned on late-July restocking from key sectors like auto, infrastructure, and galvanising. Until then, prices are likely to remain range-bound, with minor fluctuations driven by global cues, exchange movements, and monsoon-related constraints.

Leave a Reply