- Bangladesh, Pak miss HKC deadline, stare at empty yards

- India’s volumes up 36% on progress in HKC compliance

- Declining steel prices, economic pressures impact recycling

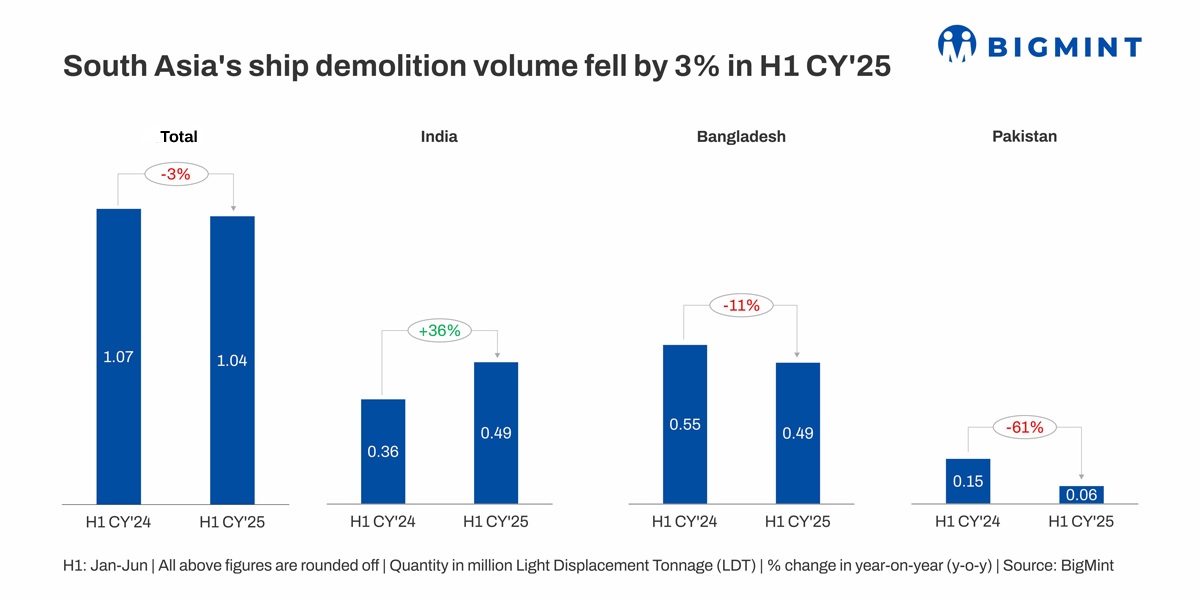

Morning Brief: South Asia’s ship-breaking volumes fell a minor 3% in H1CY’25 to 1.04 million light displacement tonnes (LDT) from 1.06 million LDT in H1CY’24. This followed a 27% drop in the number of ships dismantled, to 114 units from 156 a year earlier.

The Hong Kong Convention (HKC), which came into effect on 26 June 2025, was the primary driver behind the lower volumes overall. Among the key recycling hubs, both Bangladesh’s Chattogram and Pakistan’s Gadani struggled to upgrade yards to HKC standards.

However, India’s Alang, being an early adopter, saw a robust 36% uptick in tonnage. Several vessels were also diverted to Alang due to slow progress in Pakistan and Bangladesh.

Region-wise trends

India emerged as the top recycler in H1CY’25, narrowly beating out Bangladesh. Meanwhile, Pakistan contributed a modest share to the total.

India: Volumes reached 491,486 LDT a robust 36% rise y-o-y. The number of vessels dismantled rose modestly to 52 units in H1CY’25, compared with 50 during the same period last year.

Bangladesh: A total of 489,324 LDT was processed in H1CY’25, down 11% y-o-y, with 53 vessels dismantled versus 86 a year earlier.

Pakistan: The country recycles only 59,871 LDT, a steep 61% drop y-o-y, with only 9 vessels dismantled from 20 a year earlier.

Prices decline across vessel types, regions

Price tags of both containers and tankers fell across regions in H1CY’25, in sync with weakening steel tags. Bangladesh’s prices recorded the largest absolute declines, while India and Pakistan also faced notable reductions y-o-y. Despite this, vessels fetched the steepest prices in Bangladesh, while India’s offers were the lowest on average.

Containers

Containers

- India: Tags dropped $68/LDT y-o-y to $467/LDT.

- Bangladesh: Prices fell $73/LDT y-o-y to an average of $478/LDT in H1CY’25.

- Pakistan: Average container prices stood at $469/LDT, declining by $69/LDT y-o-y.

Tankers

- India: Prices dropped $59/LDT to $457/LDT.

- Bangladesh: Tankers were priced at $478/LDT in H1CY’25, falling by $73/LDT y-o-y.

- Pakistan: Tags were down by $62/LDT y-o-y at $459/LDT.

Factors impacting subcontinental markets in H1CY’25

India: India’s Alang ship-breaking hub progressed swiftly on HKC compliance, which enabled it to actively secure tonnage. Presently, 112 of 131 yards are certified, with many yards exceeding minimum standards through stricter safety and environmental measures.

However, weakening steel plate prices and concerns regarding imports and trade tensions strained market sentiment. Overall, recyclers faced poor margins and heavy financial pressures.

However, weakening steel plate prices and concerns regarding imports and trade tensions strained market sentiment. Overall, recyclers faced poor margins and heavy financial pressures.

Bangladesh: Bangladesh’s ship recycling sector struggled with HKC compliance delays and limited no objection certificate (NOC) approvals. While some certified yards operated, many remained idle or at capacity, causing cash buyers to divert ships to India.

Additionally, limited infrastructure activity, economic instability, and a weak steel market affected activity. If Bangladesh’s yards do not move towards HKC compliance, currently achieved by only 9 out of over 130 yards, they risk losing further tonnage in the ship recycling market.

Pakistan: The Pakistani market struggled amid political tensions, letter of credit (LC) issues, currency depreciation, and declining steel prices. Trade restrictions and uncertainty over regulations also kept recyclers cautious about future prospects. As a result, Pakistan’s yards were inactive for prolonged stretches in H1CY’25, which ultimately led to the sharp y-o-y drop in the tonnage processed.

Moreover, most Pakistani yards remained far from meeting HKC standards. The sector also faced uncertainty as the government deliberated on banning imports following 26 June, unless those ships had new mandatory environmental or safety certifications.

Consequently, buyers rushed to purchase vessels in June, even outbidding Indian rivals. Such a ban could sharply cut Pakistan’s recycling volumes, giving Alang an advantage.

Outlook

The global ship recycling market is expected to remain subdued in H2CY’25 due to tight vessel availability, firm freights, and ongoing Red Sea disruptions. However, increasing regulatory pressure will gradually lead to scrapping of older, non-compliant vessels.

India is set to maintain its lead, backed by strong HKC compliance at Alang, while Bangladesh and Pakistan may continue to lag amid compliance delays and policy uncertainties. A mild recovery is possible post-Diwali.

Leave a Reply