- HRC offers to the EU drop by $5/t w-o-w

- Prices for Nepal unchanged amid unconfirmed deal

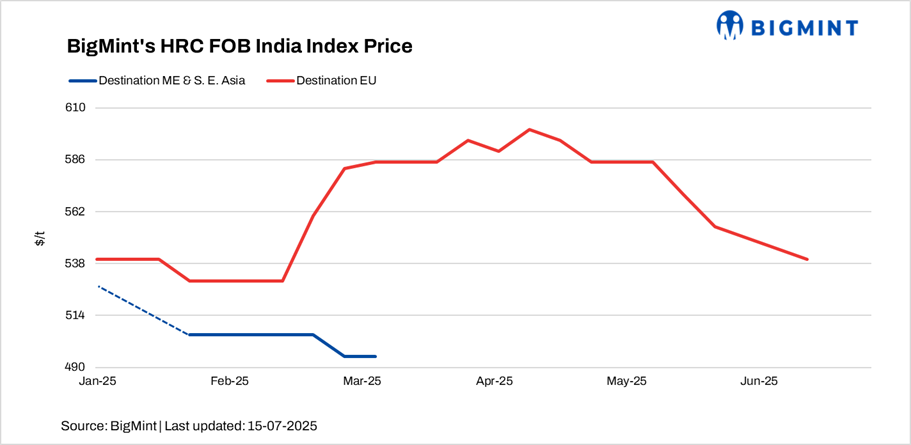

BigMint’s India HRC (S275) exports index dropped by $5/t w-o-w to $540/tonne (t) FOB main port, reflecting slow demand. India’s steel industry faces significant challenges from the EU’s Carbon Border Adjustment Mechanism (CBAM) which will become fully operational in 2026. This carbon tax could add costs to Indian steel exports.

Indian mills maintained a cautious approach in floating offers for the Middle East (ME). They chose to hold offers due to higher domestic realisations, competitive pricing from China, and prevailing geopolitical tensions in the region.

1. Indian HRC export offers to EU drop w-o-w: Indian HRC export offers to the EU dropped by $5/t w-o-w to $590/t CFR Antwerp ($540/t FOB main port India) as compared to $595/t CFR Antwerp last week. This decline in offers is attributed to slow domestic demand in the EU. A source said, “The EU’s CBAM could significantly impact Indian steel exports, potentially leading to a decline in shipments to the European market due to added carbon costs”.

European HRC prices are under pressure from weak demand, strong competition, and uncertainty, with low mill utilisation and oversupply expected to persist through summer, fuelling expectations of price declines amid cautious buying and minimal restocking.

2. Chinese HRC offers to ME remain rangebound: Chinese HRC (S235 and S275) export offers to the ME remained range-bound w-o-w at $475-480/t CFR UAE. Furthermore, the Middle East’s hot-rolled coil (HRC) market activity remained slow due to the summer slowdown, geopolitical tensions and lingering trade uncertainties. Moreover, Indian mills held back HRC offers to the ME amid stronger domestic demand and increased competition from overseas suppliers.

HRC futures on the Shanghai Futures Exchange (SHFE) increased by RMB 72/t ($10/t) w-o-w to RMB 3,259/t ($454/t) as compared to RMB 3,187/t ($444/t) a week ago. However, d-o-d, contracts edged down by RMB 10/t ($1/t) from RMB 3,269/t ($456/t).

3. Indian HRC export offers to Nepal: Indian HRC export offers to Nepal remained unchanged for the week at $550/t CFR Raxaul. An unconfirmed deal of approximately 5,000 t was heard concluded at similar price levels for July shipment. However, demand in the region remained low.

Outlook: Indian steel exports may face headwinds in the short term due to slow demand in the EU and ME. Prices are expected to remain under pressure amid oversupply and weak consumption. EU’s CBAM will significantly impact Indian steel exports in 2026, potentially reducing shipments and profit margins. This necessitates long-term strategic adjustments for Indian mills to mitigate carbon costs and maintain competitiveness.

Leave a Reply