- Mills eye Japanese scrap amid competitive prices

- Weak construction activity to hinder trade in July

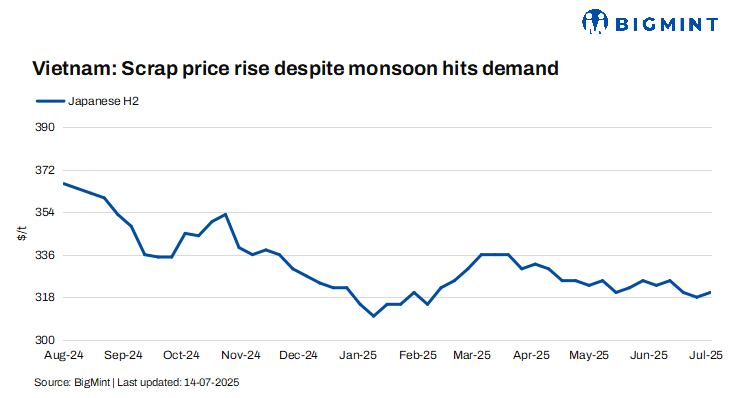

Imported ferrous scrap prices in Vietnam edged up by $2/tonne (t) w-o-w, despite subdued trading interest, influenced by monsoon-related logistical disruptions and weak construction demand.

Vietnamese buyers maintained a restrained approach this week, primarily focusing on Japanese-origin scrap. The ongoing rainy season continued to hinder construction activity, keeping finished steel demand low. Despite sluggish downstream sales, domestic longs producers opted to hold official prices steady after cutting them last week.

A market participant stated, “We can manage to get small discounts, but demand is very weak at the moment. We are not expecting any improvement in July, as the weather continues to impact construction.”

Weekly assessments

- Japanese H2 scrap was at $320/t CFR, up $2/t w-o-w.

- US-origin HMS 80:20 bulk stood at $338/t CFR Vietnam, also up $2/t w-o-w.

Market updates

A representative from a mill reported that buyers were targeting $320-325/t CFR for Japanese H2 scrap, slightly firmer than the $316-320/t seen the previous week. Corresponding FOB offers stood at JPY 41,000-42,000/t ($278-285/t).

Meanwhile, offers for US-origin HMS 80:20 deep-sea cargoes were heard at $338-340/t CFR, up slightly from $336-340/t CFR in the prior week, though no fresh deals were reported.

A trader noted that some mills needed to replenish inventories, and Japanese scrap remained competitively priced.

HS scrap offers were heard lower at $345/t CFR, while bids were at around $340/t CFR, reflecting limited buying enthusiasm.

Outlook

Market participants expect a mixed trend in the coming days. There is not much momentum in the Vietnamese market for now, as buyers are not comfortable with the current prices. Some material is also being diverted to Bangladesh. Prices might remain firm this week, supported by the Kanto tender results, but they might soften again next week.

Leave a Reply