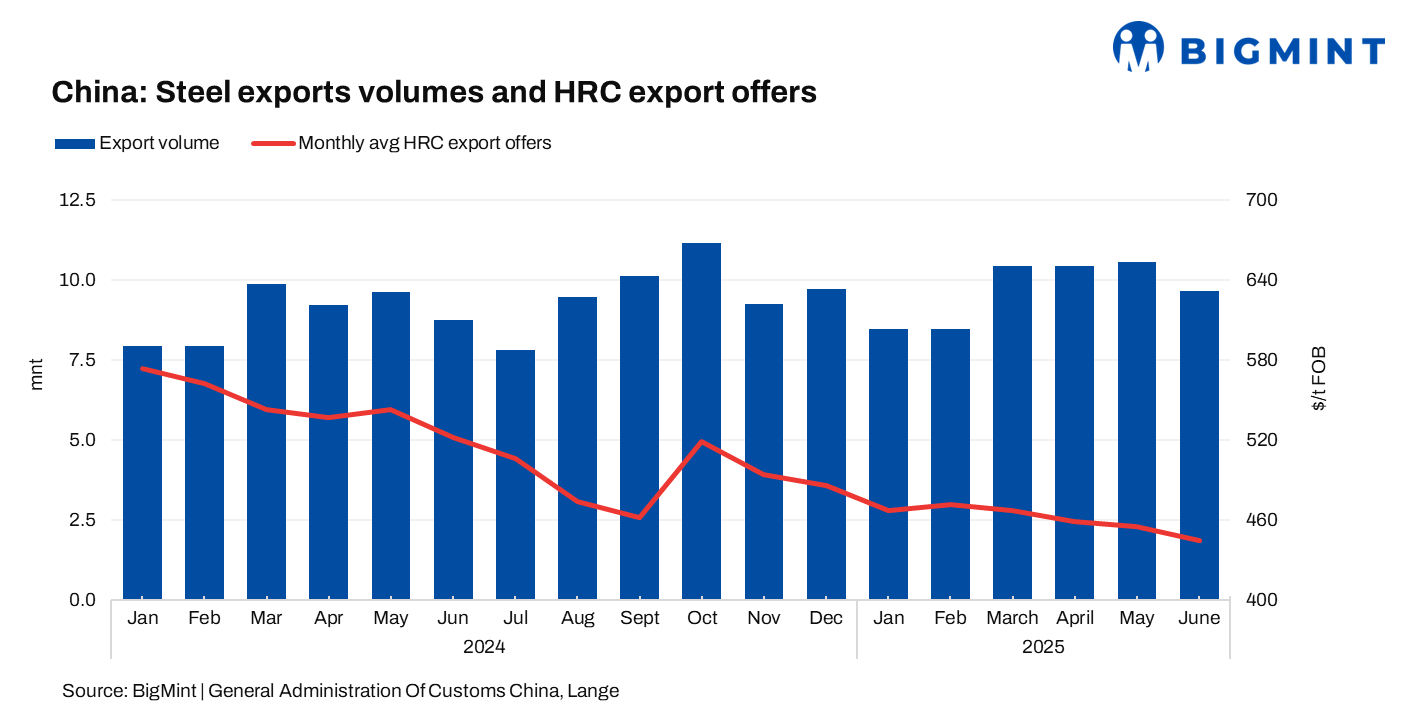

- Export volumes decline by 8.5% m-o-m

- Trade restrictions pressure export prices

China’s steel exports rose by 10.7% y-o-y to 9.678 million tonnes (mnt) in June 2025, as per data released by the country’s General Administration of Customs. In July 2024, exports had stood at around 8.75 mnt.

On a m-o-m basis, volumes declined by 8.5% against 10.58 mnt in May 2025.

Cumulative steel exports for H1CY’25 (January-June 2025) reached 58.147 mnt, up by 9.2% compared to 53.38 mnt in the same period last year.

In contrast, steel imports in June were recorded at 470,000 tonnes (t), down by 18.3% y-o-y. For the first half of 2025, total steel imports declined by 16.4% y-o-y to 3.023 mnt.

Market overview

Steel prices decline in H1CY’25: Chinese steel prices have experienced a downtrend for most of H1CY’25. Concerns about muted global demand, rising competition, and stringent safeguard measures announced by major importing countries, such as the US, EU, and some Southeast Asian countries, impacted export volumes this year.

For instance, the monthly average export offers for Chinese-origin hot-rolled coils (HRC) dropped to $445/tonne (t) FOB Rizhao in June 2025, down by $10/t m-o-m and $22.5/t from January 2025. On a y-o-y basis, the same is about $77/t lower as compared to $522/t FOB in June 2024.

Domestic demand slump leads to export push: China’s steel industry is increasingly relying on exports as a primary outlet for its production, driven by a significant downturn in domestic demand. The ongoing struggles within China’s construction sector, marked by declining property prices and investments, have led to a substantial oversupply of steel in the domestic market.

With Chinese steel consumption projected to drop by 1.5% y-o-y in 2025, the drive to export the surplus production is likely to persist. Additionally, export-driven manufacturing growth has become a crucial support for steel demand, mitigating the impact of the contracting construction industry.

Outlook

Despite an m-o-m dip in June 2025, China’s steel exports remain robust y-o-y and cumulatively for the first half of 2025, demonstrating the continued reliance on overseas markets to absorb domestic oversupply. However, the recent rebound in China’s domestic steel market signals a potential shift. The market is increasingly optimistic about government intervention to address overcapacity and the supply-demand imbalance. This suggests an improving supply-demand dynamics domestically, which, combined with growing global trade restrictions, could lead to a more balanced approach to steel production and exports in the latter half of the year.

Leave a Reply