- Crude steel production drop weighs on H1 imports

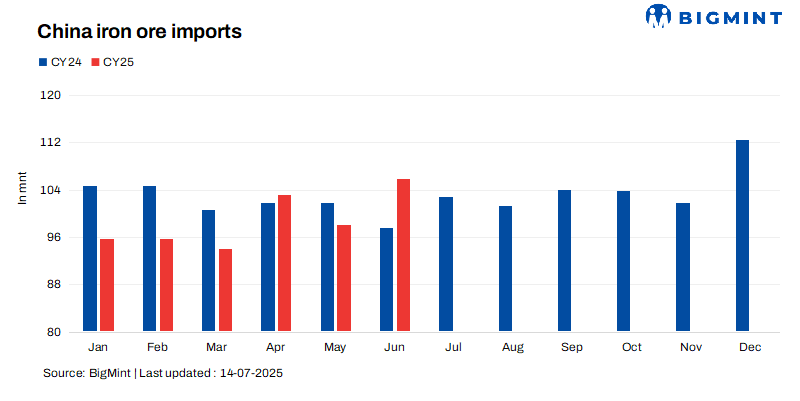

- Imports rise 8% m-o-m in Jun on restocking activity

China, the world’s largest iron ore consumer and importer, recorded iron ore and pellet imports at 592.21 million tonnes (mnt) in H1CY’25 (January-June 2025), according to the General Administration of Customs. Imports dropped 2.98% y-o-y from 610.42 mnt in the same period last year.

While China hit a record high in iron ore imports in CY’24, early signs of economic sluggishness reappeared in April 2025, as reported by the National Bureau of Statistics (NBS). Weak macro indicators reinforced expectations of a slow and uneven recovery in industrial activity, particularly in the ferrous sector. This led to a decline in iron ore imports y-o-y.

Additionally, crude steel production in January-May 2025 recorded a nominal 1.7% y-o-y decline to 431.6 mnt as against 436.53 mnt in the same period last year. Meanwhile, China’s steel demand also remained under pressure, particularly due to the property sector, which continues to struggle despite government stimulus.

Interestingly, imports rose by 7.97% m-o-m in June 2025, driven by restocking activity amid low mill inventories and prices dropping to an eight-month low of around $92.75/dmtu CFR China.

Factors affecting iron ore imports

- Steel production cuts in China: China’s crude steel production fell by 1.7% y-o-y to 431.6 mnt during January-May. A drop in steel output pressured demand for iron ore.

- Falling domestic demand: China’s steel demand from construction and infrastructure activity remained muted in H1CY’25, with limited impact from policy stimulus. Chinese steelmakers faced low profits due to the property downturn and trade frictions.

- Geopolitical turbulence, uncertainty: With Trump’s ascension to the Oval Office and his announcement of new tariff policies, global trade flows remained strained in the period, amid a cautious stance among stakeholders. Sino-US trade relations also faced a critical downturn as a part of the back- and- forth between the two economies regarding Trump’s retaliatory tariffs.

Other highlights

- Global iron ore tags see sharp $10/t fall: Reflecting poor demand from China, benchmark Fe 62% Australian fines prices dropped sharply by $18/t y-o-y to $100/t CFR China in January-June 2025 from $118/t in January-June 2024. This was largely due to subdued global steel production, lower demand, and mills opting for cost-efficient sintering blends.

- Portside inventories rise despite lower imports: Iron ore inventories at Chinese ports rose to 139 mnt in H1CY’25 from 137 mnt in H1CY’24, according to SteelHome data. The increase, despite lower imports, reflects strategic restocking amid falling prices.

Outlook

The outlook remains cautious, with global trade increasingly challenged by tariffs and export restrictions. China’s crude steel production in H2 is expected to decline by 8-10 mnt, due to stricter environmental protection regulations, decarbonisation targets, and output control policies, Mysteel suggests. This is likely to weigh on iron ore imports. On the other hand, global iron ore supplies are likely to remain high, which may keep prices under pressure.

Leave a Reply