- LME stocks up, mine output rises in key regions

- Expectations of short-term oversupply increase

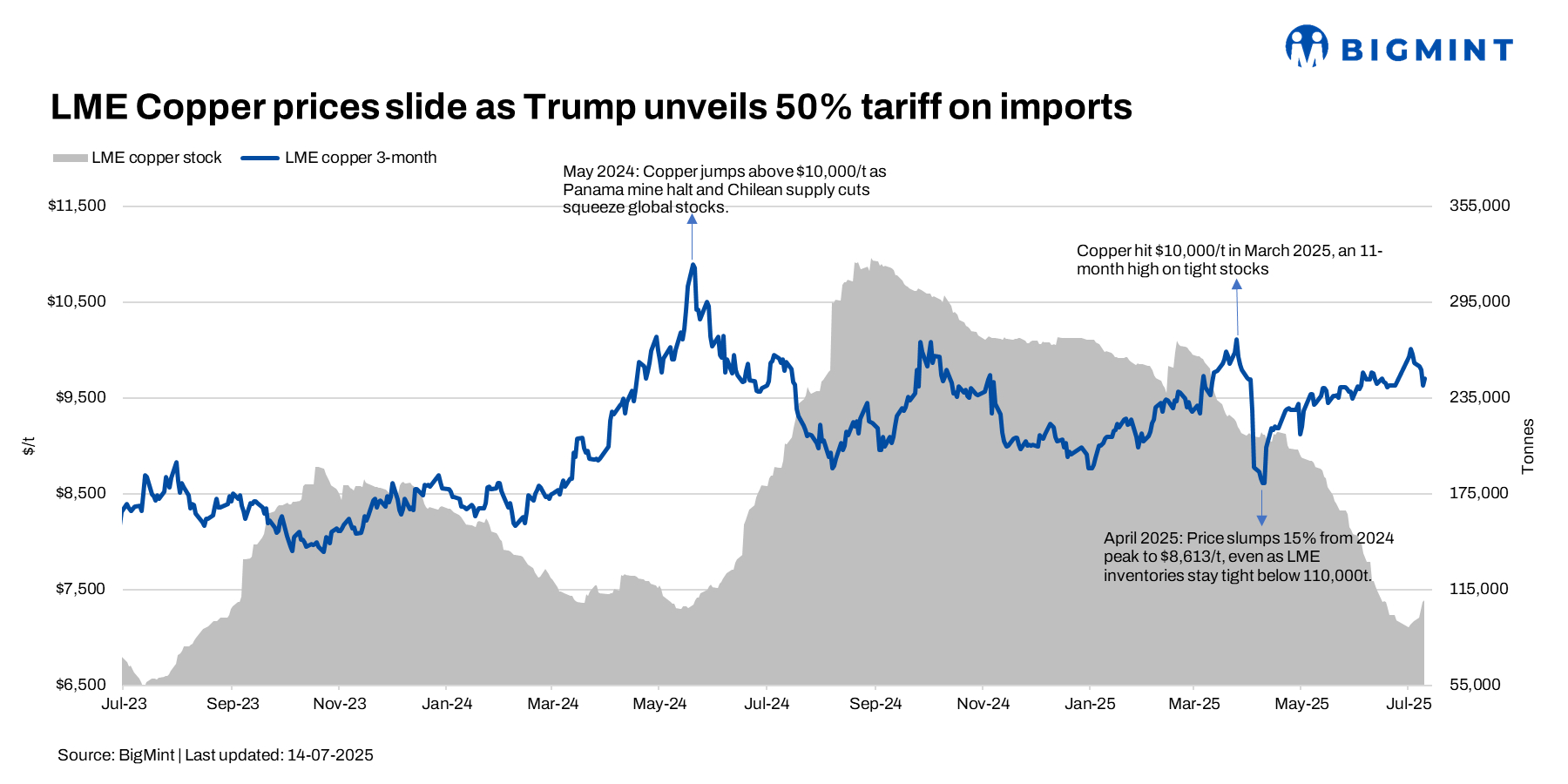

Copper prices eased last week on the London Metal Exchange (LME), with the 3-month contract hovering at around $9,730/tonne (t), down 2% w-o-w, due to a mix of macroeconomic uncertainty, speculative shifts, and changing market fundamentals.

Over 30 June-4 July 2025, LME copper stocks rose to 95,275 t from 90,625 t, a w-o-w increase of 4,650 t or about 5.1%; in contrast, during the following week, over 7-11 July, stocks surged to 108,725 t from 97,400 t, marking a much sharper rise of 11,325 t or approximately 11.6%

Tariff uncertainty disturbs trade flows

Uncertainty around the upcoming US copper import tariff (up to 50%) has unsettled global markets. While some buyers are rushing to secure material ahead of the August 2025 deadline, others have stepped back, awaiting clarity. This uneven demand has created volatility and limited price momentum.

Speculative selling, inventory build-up pressure prices

After copper approached the key $10,000/t resistance, profit-taking and long position unwinding by funds led to a price correction. Meanwhile, LME inventories rose by 4,625 t in a single day (up 4.5%), suggesting easing tightness. The market structure also shifted from backwardation to a mild contango, indicating growing expectations of short-term oversupply.

Mine production ramps up across key regions

Kamoa-Kakula (DRC): Produced 112,009 t of copper in Q2CY’25, an 11% y-o-y increase. The mine successfully restarted operations on its western side, ramping up production and processing rates, and expects higher grades later in the year.

Codelco (Chile): Output is up 9% in the first half of 2025 as the company recovers toward pre-pandemic production levels.

Barrick’s Lumwana Expansion (Zambia): The expansion project is in full swing, aiming to double annual copper production to 240,000 t.

Outlook

While increased mine production (not just from Kamoa-Kakula, but also from Peru, Chile, and others) has eased some immediate supply concerns, the copper market remains volatile. Policy uncertainty – especially around US tariffs, which are set to take effect in August 2025 -continues to distort trade flows and create price swings.

Leave a Reply