- Iran’s steel exports down 11% over Apr’24-Mar’25

- China’s longs exports surge 100% y-o-y in Q1CY’25

- Tariff-stonewalled China seeks newer global markets

Madhumita Mookerji

With the Israel-Iran tensions sustaining despite the Gaza ceasefire, the latter’s steel exports prospects may become uncertain, going forward. The latest salvo comes in the form of the Iran-aligned Houthi militants’ attack on a Liberian-flagged vessel that has resulted in four casualties and the fate of 11 crew members uncertain. Israeli Prime Minister Benjamin Netanyahu recently indicated that the war against Hamas is “far from over”. In such an eventuality, there is a possibility of China gaining from such circumstances.

Iran is the largest exporter of steel from the Middle East and it exports mainly to countries within that region, as well as to Southeast Asia. Many now feel, if the tensions between Iran and Israel escalate, China could take over Iran’s export markets, mainly of longs, much to the latter’s disadvantage. Such a scenario would make sense for China, especially since it is being stonewalled by trade barriers from across the world. From Section 301 duties in the US to anti-dumping tariffs enforced by the EU, protectionist trade instruments continue to influence global supply chains, cost structures, and corporate strategies, forcing China to seek greener export pastures.

Iran steel exports show mixed trend

Iran’s steel exports, as per BigMint data, have already provisionally declined more than 11% to 10.04 million tonnes (mnt) over April 2024-March 2025 against 11.30 mnt seen in the same period last year. Iran’s semi-finished steel exports in the first two months of the current Persian Year (21 March-May 2025) increased by 31% y-o-y, while production edged down y-o-y 6%, according to data from Petrometals. The increase in semis’ exports can be attributed to several factors: sluggish domestic demand, which prompted a shift to exports; favourable pricing in international markets; and expanded production by key steelmakers despite ongoing energy constraints.

However, exports of long products were recorded at 488,000 t, down 21% y-o-y, while shipments of flats increased sharply by 154% y-o-y to 127,000 t.

Despite the ongoing war, power restrictions, and shortages disrupting industrial activities, Iran has tried to keep its steel exports resilient so far, even as production has been adversely affected by the same challenges. But, for how long? US and EU sanctions on the country’s exporters are making it challenging to close financial transactions, especially through the SWIFT system.

China’s aggression impacts SEA exporters

Chinese long steel exporters, on the other hand, have started pushing out Southeast Asians mills, which had dominated the market so far. Chinese long product exports surged by over 100% y-o-y in the first quarter of 2025. “Reduced blast furnace costs, sustained fall in domestic demand, and export subsidies mean this wave of Chinese exports will not slow as it is policy-driven, not market-driven,” says the report.

A serious shift is taking place — Vietnam, Malaysia and Indonesia are all fighting for markets in the face of the Chinese aggression, including South Korean mills, “which were deemed to be bulletproof previously”. Chinese mills are offering their material cheap and are desperately seeking newer markets to offset the sustained lack of home demand.

In fact, Chinese HRC export offers to the Middle East have fallen 5% to $475/tonne CNF Abu Dhabi, in May 2025, from $499/t in January.

Oil prices are also weak which is good for Chinese steel exporters since this is translating into lower freight costs.

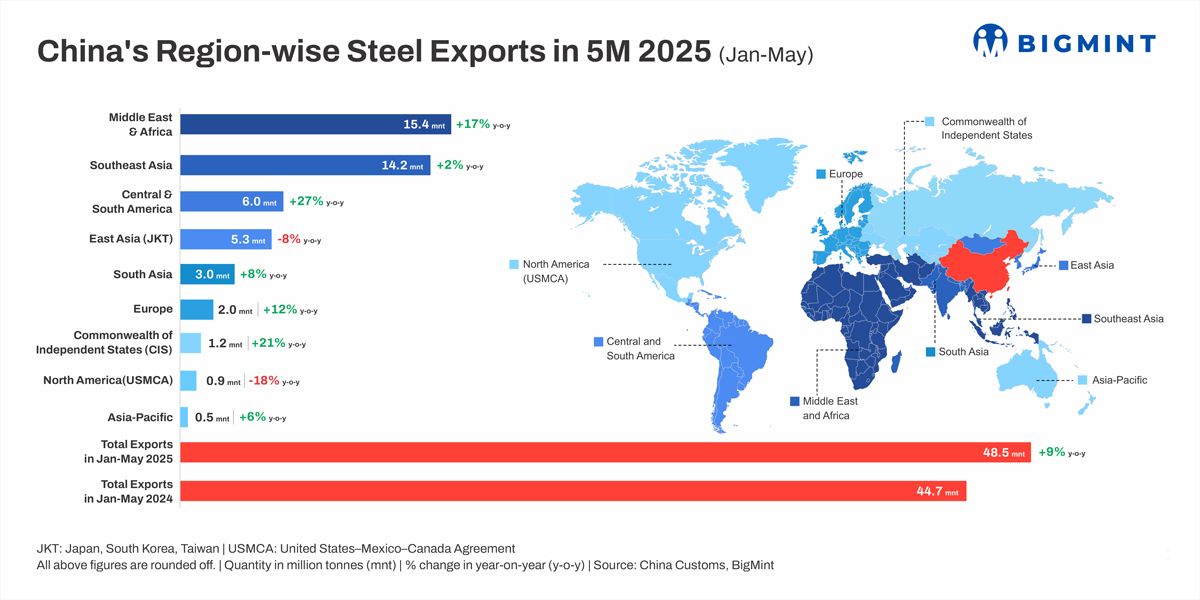

China’s total steel exports are up 9% over January-May, 2025 at well over 48 mnt against 45 mnt seen in the same period last calendar.

When asked if China could benefit from an extended Iran-Israel conflict, a source in China corroborated, “Yes, there is a chance since the stimulus programmes have not really helped to boost domestic steel demand.”

Outlook

The expected demand recovery in the aftermath of the Lunar New Year holidays in China failed to materialise and so competitively-priced Chinese steel is expected to be sold in export markets. However, the extent to which this will happen depends on the level of demand in global markets as well as domestic demand in China. The cut-throat competition will expectedly keep exports terrain uncharted in the short-to-medium term

Leave a Reply