- Steel exports reach 48.5 mnt in 5MCY’25

- Exports to India drop sharply by 27% y-o-y

- Chinese steel consumption may drop 1.5% y-o-y in CY’25

Morning Brief: Despite global trade protectionism reaching new heights under Trump 2.0 and tariff warfare continuing unabated, Chinese exports of steel are saturating the global market and stoking fears of a prolonged slump in the industry.

BigMint data show that exports of steel by China increased by 8.5% y-o-y to 48.5 million tonnes (mnt) in January-May 2025 (5MCY’25) from 44.7 mnt in the same period last year.

In May, however, export momentum would appear to have flagged somewhat: total shipments rose by just 1% m-o-m in May to 10.6 mnt compared with 10.5 mnt in April.

At over 111 mnt, China’s steel exports in 2024 had hit a nine-year high even as domestic steel production saw a marginal contraction.

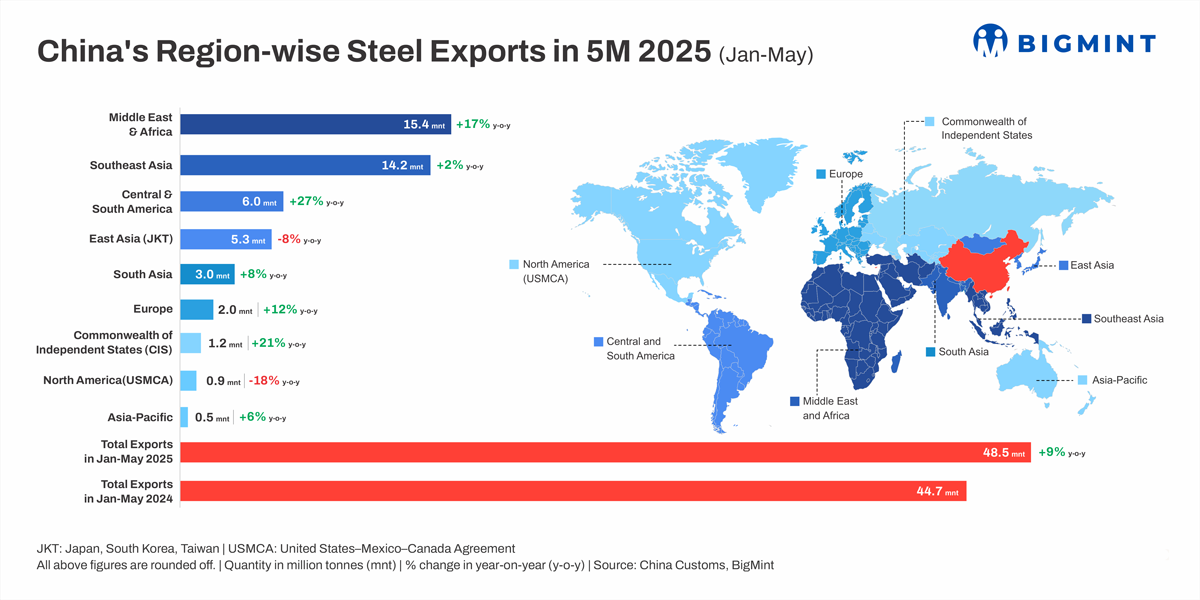

Region-wise steel exports

The Middle East and Africa region emerged as the largest importer of Chinese steel in 5MCY’25, with total imports into the region increasing by an impressive 17% y-o-y to 15.38 mnt. The top importers in the region – UAE and Saudi Arabia – witnessed steady growth in imports. Imports by Turkiye dropped just 1% y-o-y despite an anti-dumping duty on Chinese HRC imposed in October last year.

Southeast Asia’s imports of steel from China stood at 14.2 mnt in 5MCY’25, a marginal increase of 2% y-o-y. Volumes to Vietnam fell 26% y-o-y due to AD duty imposed on Chinese steel. However, existing tariffs in Thailand, Malaysia and Indonesia seem to have failed to rein in rising imports from China.

In East Asia, on the other hand, total imports of Chinese steel recorded a decline of 8% y-o-y in 5MCY’25. South Korea and Taiwan witnessed a decrease in imports amid trade protections and tariffs. Japan’s imports were largely flat y-o-y.

China’s exports to the South and Central American countries increased by 27% y-o-y to nearly 6 mnt in 5MCY’25. The capacity utilization of Latin American steel producers seem to have been impacted owing to high Chinese steel exports into the region, according to industry bodies. Brazil, despite clamping down safeguard measures and a quota-based tariff system, saw imports rising by 7% y-o-y in 5MCY’25.

While China’s exports to South Asia (mainly India and Pakistan) rose by 8% y-o-y, exports to India dropped 27% during the review period due to safeguard measures and other non-tariff barriers related to quality certification. Steel exports to the EU and CIS countries increased by 12% and 21%, respectively, in 5MCY’25.

China’s steel exports rise 9% y-o-y in Jan-May’25.

Why did China’s steel exports edge up in 5MCY’25?

Tariff fear leads to front loading of shipments: While China’s steel exports to the US were meagre, just 0.36 mnt in 5MCY’25, the imposition of tariffs, counter tariffs and reciprocal tariffs by both countries preceding a 90-day truce triggered panic in the market. This resulted in exporters as well as buyers frontloading booked shipments in order to avoid the tariff impact. The tariff announcements and the subsequent knee-jerk reaction of market participants contributed to a surge in shipments in March and April.

Weak domestic demand propels exports: As the construction sector in China faces headwinds and property prices and investments continue to decline, the dearth of steel demand from this sector is creating a supply glut in the domestic market. And the only way to release this oversupply is through exports.

China’s steel consumption is projected to decline by 1.5% y-o-y in 2025 and, therefore, the export momentum is likely to continue. Moreover, export-led manufacturing growth has emerged as a key pillar supporting steel demand amid the construction slump.

Competitive prices boost exports: Chinese steel prices enjoy the advantage of being super competitive compared with Japan, South Korea and even India. This is because, unlike its peers, the Chinese steel industry gets to avail of state largesse and subsidies that provide considerable cost advantage to producers.

Also, as the domestic demand slump continues, steel prices in China are languishing, which explains the rapid decline in steel export prices. So, China is in a position to elbow out other competitors from emerging markets such as the Middle East.

Outlook

That said, China’s exports-led growth strategy in the steel sector has hit the brickwall of protectionism and tariffs. From Vietnam to South Korea and from Turkiye to India, all major steel importing countries have taken recourse to anti-dumping and safeguard measures against Chinese imports. In 2024 alone, as many as 24 countries started AD and safeguard investigations. Therefore, continued growth in China’s exports is unlikely.

On the other hand, indirect steel exports by China in the form of appliances and machinery are also going to be hit as US tariffs batter the major exporting sectors. Key exporting countries such as Vietnam and South Korea may drastically reduce steel purchases from China as tariffs impact their downstream sectors.

In H2CY’25, possible reduction in Chinese crude steel production, the financial impact of tariffs, and growing trade barriers are poised to mount a formidable challenge to Chinese steel exports.

Leave a Reply