- Buying activities remain weak on low demand

- Imported scrap market remains sluggish

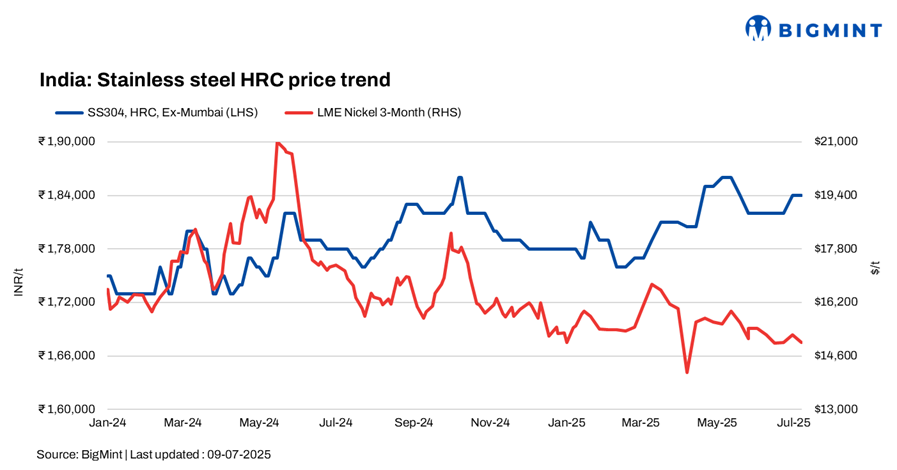

India’s stainless steel (SS) finished flats prices inched up this week despite of drop in LME Nickel prices while finished longs prices dipped w-o-w amid persistent weak demand.

BigMint’s benchmark assessment for stainless steel 304 series hot-rolled coils (HRCs) hovered at 184,000/tonne (t) up by INR 2,000/t, while 304L (25-100 mm) black round bars stood at INR 158,000/t, up by INR 1,000/t, both ex-Mumbai.

LME nickel dip, Asian NPI remain steady w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,000/t, showing a drop of 2% from last week’s $15,265/t. Nickel stocks in LME-registered warehouses stood at 202,620 t, range-bound compared to 203,886 t in the previous week.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) stood at RMB 915/t ($129/t). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $110/t. Both were steady w-o-w.

Market insights

According to market participants, “Buying activities remained weak, as buyers were asking for much lower prices due to minimal infrastructure-related activity.”

Additionally, as per BigMint’s assessment, SS 316 HRCs stood at INR 330,000/t up by INR 3,000/t and 316 cold-rolled coils (CRCs) at INR 336,000/t ex-Mumbai, up by INR 1,000/t w-o-w.

As per sources, Stainless steel IF route longs for 304 black round bars were heard at INR 140,000-142,000/t while 316 black round bars were heard at INR 150,000-152,000/t.

Chinese stainless steel prices steady

In China, prices of domestic stainless steel 304-grade cold-rolled coils (CRCs) stood at RMB 13,450/t ($1,874/t) exw, stable w-o-w, while FOB tags of 304-grade CRCs were stable at $1,910/t.

Raw material scenario

Ferro Molybdenum: Indian ferro molybdenum prices rose further by INR 30,000/t ($349/t) in comparison to the previous assessment on 2 July. Prices reached their highest levels since July last year amid a shortage of molybdenum oxide in the domestic market.

As per BigMint’s assessment on 9 July, ferro molybdenum prices in India were at INR 2,730,000/t ($31,803/t) exw. Deals for around 65 t were recorded by BigMint in this assessment window in the price bracket of INR 2,620,000-2,750,000/t ($30,521-32,036/t) exw.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 99,500/t ($1,160/t) exw-Jajpur, range-bound w-o-w.

Vedanta-FACOR’s ferro chrome production jumped 150% q-o-q to 28,000 t in Q1FY’26 from 11,000 t in Q4FY’25. Chrome ore output rose 66% q-o-q to 108,000 t, the highest ever quarterly figure, compared to 65,000 t in the previous quarter. The surge was attributed to the recommissioning of a second furnace, which boosted smelting capacity, along with improved ore availability.

Ferro silicon: Indian ferro silicon (70%) prices dropped INR 1,400/tonne (t) ($16/t) in comparison to the previous assessment on 30 June. As per sources, Bhutan opened July prices at INR 88,000/t ($1,027/t) exw. However, most sellers quoted lower offers.

As per BigMint’s assessment on 7 July, ferro silicon prices in India were at INR 87,000/t ($1,015/t) exw-Guwahati. In Bhutan, prices dropped by INR 900/t ($11/t) w-o-w to INR 87,100/t ($1,016/t) exw. Deals for around 4,000 t were concluded in both regions in this assessment window, within the price bracket of INR 85,000-88,000/t ($992-1,027/t) exw.

Ferrous scrap: India’s imported ferrous scrap market remains sluggish as weak steel demand and abundant domestic scrap supplies keep buyers on the sidelines.

Shredded scrap offers are holding around $365/t CFR Nhava Sheva, but most buyers are only willing to bid closer to $355/t. HMS sellers are seeking $330-335/t CFR, yet actual deals remain scarce as many buyers increasingly opt for sponge iron, given its competitive pricing and steady availability.

Distress sales continue in the market, while fresh bookings are limited due to a significant gap between bids and offers. Buyers are largely purchasing only what’s strictly needed.

Outlook

Stainless steel market remained cautious amid weak demand in longs segment, however, post-monsoon, sentiment is expected to improve as construction and infrastructure activity gain momentum.

Leave a Reply