- Drop in fuel, bunker prices support rates

- Baltic Capesize index falls to 1-month low

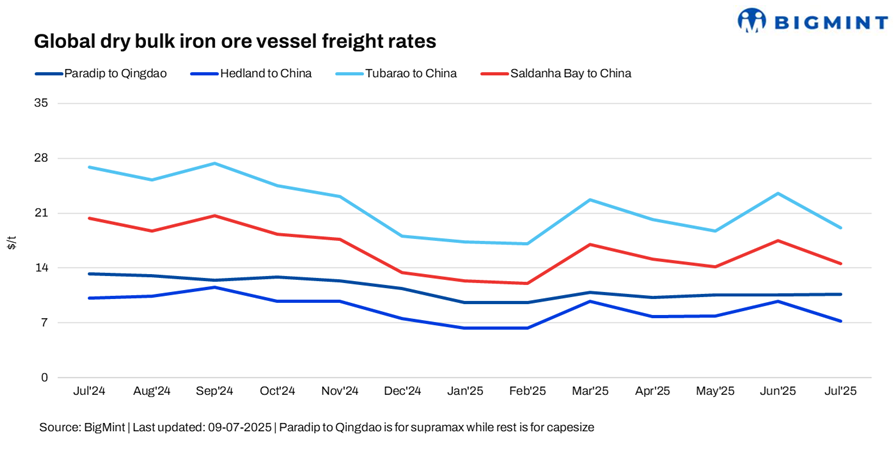

Dry bulk iron ore freight rates showed mixed trends this week. Rates on the India-China and Australia-China routes saw a slight recovery after a recent dip. In contrast, rates on the Brazil-China and South Africa-China routes declined on a w-o-w basis.

However, the overall sentiment in the Capesize segment remained tepid, with muted trading activity and some describing the market as “quiet,” despite reasonable vessel demand in the Pacific. Iron ore cargoes continued to surface from the region, though most were for forward loading, reflecting a lack of urgency among charterers to fix.

Meanwhile, bunker and fuel prices at key ports declined this week, offering some relief to overall voyage costs for dry bulk operators.

On the contrary, a w-o-w increase in Forward Freight Agreement (FFA) rates for Capesize and Supramax vessels has added to the cost risk for charterers, according to BigMint.

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freight rates for Supramax vessels from the Indian Ocean to China rose to $11/dry metric tonne (DMT), up by $0.7/DMT w-o-w. The increase was supported by hike in low-grade iron ore export offers from India, along with a rise in global iron ore prices and gains in DCE iron ore, SHFE rebar, and HRC futures over the week.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freight rates for iron ore shipments from Western Australia to China rose to $7.60/DMT, marking a w-o-w increase of $0.7/DMT. The uptick was attributed to active chartering by major Australian miners, including Rio Tinto and BHP, who fixed vessels to Qingdao at rates between $7.55-7.75/DMT for end-July 2025 laycans. This surge in activity led to a tightening of available tonnage, sources informed BigMint.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freight rates for Brazil to China shipments declined by $1.3/DMT w-o-w, settling at $18.50/DMT. Two fixtures were reported on the Tubarao-Qingdao route – one concluded at $19.50/DMT towards the end of last week, and the other at $18.40/DMT earlier this week, both for laycans spanning end-July to early-August 2025. Sources noted that the market saw firmer fixtures following initial softness. However, a persistently long ballast list (referring to the high number of vessels sailing empty toward Brazil) continues to pressure forward sentiment.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freight rates from Saldanha Bay to Qingdao declined by $2/DMT w-o-w, settling at $13.60/DMT. The drop was attributed to a lack of fresh fixtures and muted chartering activity, as limited cargo demand from the region kept the market subdued.

Market highlights:

- Baltic capesize index falls to 1-month low: The Baltic Exchange’s dry bulk sea freight index fell to a one-month low on 8 July 2025, dragged down by a sharp drop in Capesize vessel rates. The main index, which tracks freight rates for Capesize, Panamax, and Supramax vessels, declined by 5 points to 1,431 points, marking its lowest level since 3 June 2025. Meanwhile, the Capesize index saw a steeper fall, dropping 74 points to 1,751 points, registering its sixteenth consecutive decline.

- China’s iron ore spot prices remains firm w-o-w: Chinese spot prices for iron ore fines (Fe62%) were assessed at $95/tonne (t) CFR China on 9 July 2025, up by $2/t w-o-w. The rise was driven by active trading, particularly in medium-grade fines, and was supported by an overall uptrend in the ferrous complex, including gains in steel futures and related raw materials. Despite the price increase, Chinese mills remained cautious, opting to purchase only as needed rather than building bulk inventories.

Outlook

The near-term outlook remained mixed, with market participants divided over the direction of rates amid fluctuating demand and weather-related disruptions. The ongoing monsoon in India is impacting the iron ore market, with rising moisture levels in the material often breaching acceptable tolerance limits, a source noted.

Meanwhile, falling fuel prices and rough sea conditions during the monsoon season are expected to lend support to freight rates. However, due to these same factors, forward freight agreements have increased, which may result in fewer vessel bookings in the near term, another source commented.

Leave a Reply