- Iron ore, pellet prices decline

- BF-origin rebar down INR 1,000/t w-o-w

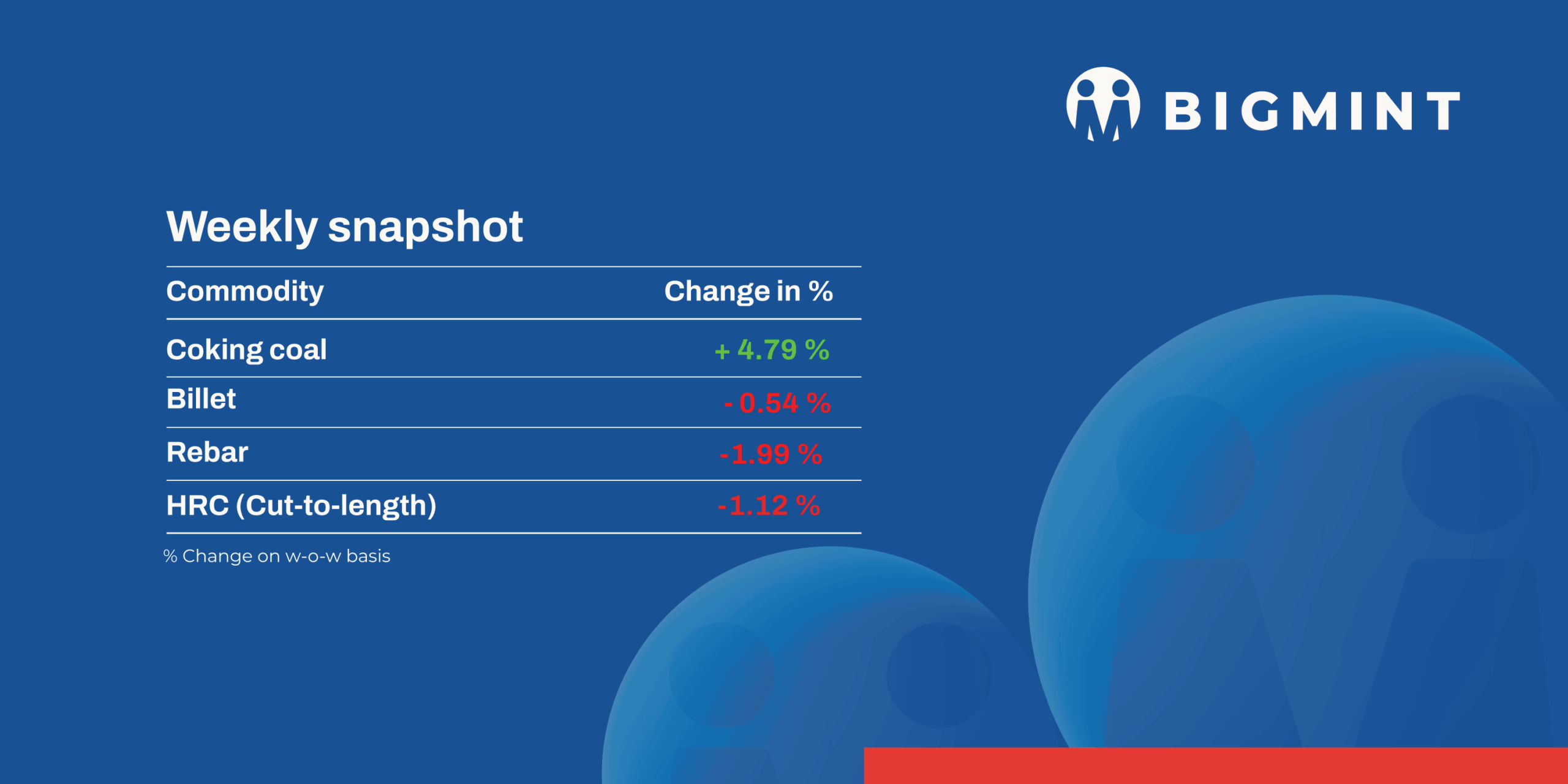

The domestic steel market saw mixed trends during week 27 (30 June – 5 July, 2025). Iron ore and pellet prices declined w-o-w, while semi-finished and long steel segments remained under pressure amid subdued demand and monsoon disruptions, flat steel prices were mostly unchanged.

Iron ore and pellet

India’s largest merchant iron ore mining company, NMDC, decreased list prices of iron ore CLO (calibrated lump ore) and fines for July. The miner has fixed prices of DR CLO (10-40 mm, Fe 67%) at INR 6,400/tonne (t) ($75/t) and of iron ore fines (-10 mm, Fe 64%) at INR 4,850/t ($57/t), a decrease of INR 650/t ($8/t) and 500/t ($6/t), respectively. Prices are on FOR basis from the miner’s Bacheli complex and include royalty, DMF and NMET.

PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, fell by INR 250/t ($3/t) w-o-w to INR 8,900/t ($104/t) DAP Raipur on 4 July. Raipur-based pellet producers cut offers for Fe 62/63% (+/_0.5%) material by INR 300/t ($3.5/t) to INR 8,700-8,800/t ($102-103/t) exw. Around 145,000 t of pellet deals were recorded in Raipur this week by local sellers at the same prices.

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index inched up by $3/t w-o-w to $62.5/tonne (t) FOB east coast on 3 July. Around 230,000 t Fe57% fines were sold at $72-73/t CFR China during the review period. Global fines prices found boost from fresh bookings, improved futures sentiment, and positive policy cues, with low port-side inventories expected to sustain near-term buying interest.

Coal

South African thermal coal prices at Indian ports moved up slightly this week. Exw-Gangavaram RB2 (5500 NAR) rose INR 50/t to INR 7,650/t, while RB3 (4800 NAR) touched INR 6,650/t. CNF offers stayed flat at $80–81/t for RB2 and $68–69/t for RB3, despite earlier index gains. Port stocks stayed steady around 15.86 mnt, keeping market sentiment cautious.

Domestic coal prices stayed flat this week, reflecting sluggish market sentiment. BigMint assessed 5000 GCV at INR 4,700/t and 4500 GCV at INR 4,250/t exw-Bilaspur, unchanged w-o-w. The market was notably quiet, with almost no fresh enquiries and scattered offers under selling pressure.

BigMint’s premium hard coking coal (PHCC) index climbed by $9/t w-o-w to $196/t CNF Paradip on 4 Jul’25, supported by an end-August deal from Australia at around $203 CFR for 40,000 t.

Metallurgical coke prices stayed firm this week, with BigMint’s 25–90 mm BF grade assessed at INR 28,000/t ex-Jajpur and INR 29,000/t exw Gandhidham. Market sentiment was cautiously positive as the government extended import quotas on LAM coke until Dec’25, aiming to support local producers.

Ferrous scrap

India’s imported scrap market remained subdued in the first week of July due to weak steel demand, monsoon disruptions, and the availability of cheaper domestic alternatives like sponge iron. Shredded scrap offers hovered at $360-365/t CFR Nhava Sheva, while bids stayed lower at $355-360/t, limiting trade.

HMS 80:20 offers ranged $330-345/t CFR from UK and West Africa, but Indian buyers bid lower at $325-330/t for UK cargoes. Traders reported minimal inquiries as mills held back from fresh purchases.

Last week, around 8,000-9,000 t of imported scrap were booked into India, including HMS 1, busheling scrap, and HMS 80:20, with prices ranging from $320-343/t for HMS grades and $370/t for busheling.

Ferro Alloys

Silico Manganese

Indian silico manganese prices (60-14) witnessed a slight increase of INR 550/t ($6/t) w-o-w to INR 72,000-72,900/t ($842-853/t) in the key regions of Durgapur, Raipur, and Vizag. Rising production cuts tightened domestic silico manganese supply in India, pushing prices higher w-o-w amid renewed export enquiries from Southeast Asia and the Middle East.

Additionally, MOIL, a state-owned mining company, has announced a price revision in manganese ore, effective 1 July. The company has implemented a modest 2% increase in prices of ferro grades — “both above and below 44% Mn content”, as per a company release.

Ferro Manganese

Indian ferro manganese (HC 70%) prices remaned flat w-o-w INR 71,900/t ($841/t) exw in Durgapur. Meanwhile, prices, exw-Raipur, edged up to INR 72,200/t ($845/t). Stability was supported by balanced market activity characterized by steady demand, consistent supply, and cautious trading sentiment among buyers and sellers this week.

Ferro Silicon

Indian ferro silicon prices dipped by INR 1,400/t ($16/t) w-o-w to INR 87,000/t ($1,018/t) exw-Guwahati. Meanwhile, Bhutanese prices also decreased by INR 500/t ($6/t) to INR 87,500/t ($1,023/t) exw. Reliable sources indicate that Bhutan has set prices at INR 88,000/t ($1,029/t), yet most sellers continue to quote prices below this level.

Ferro Chrome

Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices edged down by INR 500/tonne (t) ($6/t) w-o-w to INR 99,500/t ($1,164/t) exw-Jajpur. Prices edged down amid cautious buying, stemming from widening bid-offer disparities.

Semi-finished steel

Indian semi-finished steel prices showed a downtrend, as per BigMint’s assessment. Domestic billet prices in all key locations decreased by INR 50-1,000/t across regions and a major fall of INR 1,000/t was seen Mumbai and Jalna. Otherwise, sponge iron prices showed positive trends in almost all key locations, moving up by INR 50-550/t.

Indian DRI (Direct Reduced Iron) export offers stands still for CPT Raxaul, at $315/t while, CPT Benapole offers dropped by INR 4/t to $321/t.

NMDC’s steel plant in Nagarnar, Chhattisgarh, auctioned 10,000 t of steel-grade pig iron on 1 July, with 7,500 t booked at an average price of INR 31,100/t (by road). However, management approval is still pending. Notably, bids dropped by INR 400/t from the previous approved auction, held on 10 Jun’25 for 15,000 t, where 5,200 t were booked at an average price of INR 31,500/t (by road).

SAILs Rourkela Steel Plant (RSP) conducted an auction for 7,100 t of steel-grade pig iron on 1 July, in which the entire quantity was booked at an average price of INR 31,200/t exw. This shows a decrease of INR 800/t compared to the previous auction on 7 June, in which 3,000 t were sold at INR 32,000/t exw.

Finished long steel

IF-rebar: India’s induction furnace route finished long rebar prices remained under pressure this week amid subdued market sentiment. Buying activity was largely limited to immediate requirements, while manufacturers continued to lower prices to boost sales. Current inventory levels are estimated at around 12–15 days. In several regions, mills have under gone maintenance which has reduced the production by 20-30% . Market participants anticipate prices to remain weak in the near term, citing sluggish project demand and slow construction activity due to the ongoing monsoon season.

On a weekly basis, rebar steel prices declined in the range of INR 200-1,200/t across regions except Durgapur and Patna where prices rose by INR 200/t and INR 1,000/t respectively as per BigMint assessment shows. The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 39,200-39,600/t exw Raipur, INR 42,900-43,500/t exw Jalna. Trade reference price of heavy structural steel for base size 150mm channel stands at INR 41,600-42,000/t exw Raipur. Trade reference prices of wire rod hovering at INR 40,800-41,300/t ex Raipur.

BF-rebar: Indian primary mills have cut rebar prices by up to INR 1,000/t ($12/t) for early-July 2025 deliveries as against prices prevailing in end-June. Post-revision, list prices stand at INR 50,000-51,500/t ($585-603/t) on landed basis. It should be noted that mills had offered discounts/rebates to augment sales last month. Trade-level BF rebar prices declined by INR 800/t ($9/t) w-o-w to INR 49,900/t ($584/t) exy-Mumbai, as per BigMint’s assessment on 4 July 2025. In the projects segment, prices opened at INR 48,500-49,500/t ($567-579/t) FOR Mumbai basis. Weak buying activities continue to weigh on market sentiments & exerted pressure on prices.

Flat steel

Indian steel producers have maintained list prices for hot-rolled coils (HRCs) and cold-rolled coils (CRCs) for July 2025 sales. While most mills officially held prices steady, market participants suggest price support or reduction of INR 1,000-2,000/t

India’s bulk imports of HRCs touched 294,879 t as of 27 June, based on vessel line-up data from BigMint. Around 159,825 t of cargo are expected in July.

India’s HRC export offers to the EU fell by $26/t m-o-m to $565/t FOB in June, amid weak demand, high inventories, and summer slowdown. Despite lower offers, buyer interest remained muted. Indian mills focused on the domestic market due to better price realisations, limiting exports to Europe.

Leave a Reply