- Raw materials, steel prices fall in Jun’25

- Steel slump squeezes Mandi mills

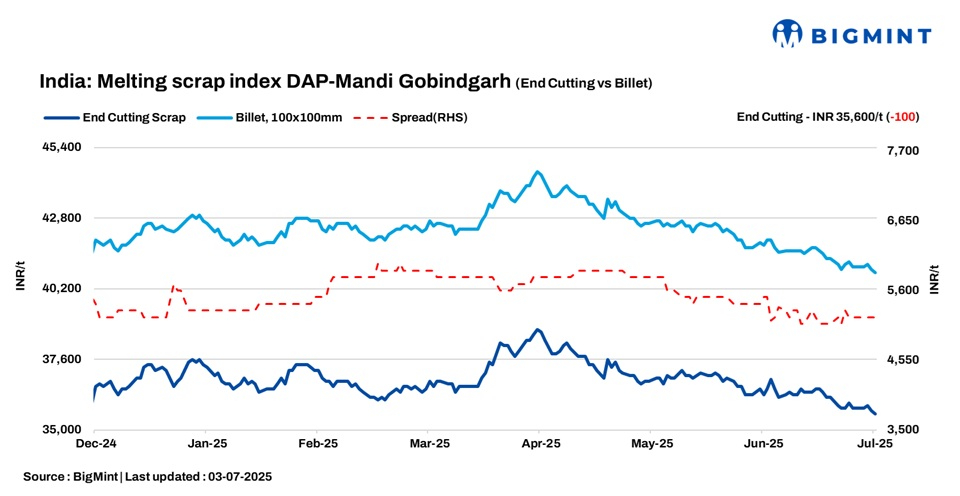

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, fell by INR 100/tonne (t) d-o-d to INR 35,600/t DAP on 3 July, 2025. Today in Mandi and Ludhiana, steel scrap prices declined by INR 100-200/t across various grades amid ongoing GST checks, which continue to hamper scrap buying activity.

Key raw material prices decline in June

In Mandi, sponge iron prices fell by INR 100/t day-on-day to INR 28,700/t today, while steel-grade pig iron prices in Ludhiana remained stable at INR 35,100/t DAP.

According to data, Mandi raw material prices continued to ease in June, reflecting muted demand and correction in scrap prices.

Sponge iron (CDRI) prices at Mandi dropped INR 29,180/t in June, down 4% from INR 30,388/t in May and 8.7% from April’s INR 31,954/t. This marks the lowest level in the last six months.

Pig iron (steel grade) at DAP Ludhiana averaged INR 35,856/t in June, a 1.1% drop from INR 36,263 in May and 6.8% down from INR 38,457/t in April, continuing a softening trend post-March.

HMS (80:20) Scrap prices at DAP Mandi stood at INR 33,224/t, slipping 2.2% from INR 33,969/t in May and 4.6% down from INR 34,815/t in April. This marks the third consecutive month of decline.

Steel market softens: June sees continued price slide

Today, steel ingot prices in Mandi Gobindgarh declined by INR 100/t d-o-d to INR 40,800/t (DAP). Semi-finished steel prices in other regions also declined by INR 50-200/t.

The Mandi steel market saw continued decline in prices in June, as per data. Both ingot and rebar prices dropped for the second straight month, reflecting sluggish demand and falling raw material costs.

Ingot prices averaged INR 41,464/t in June, down 2.2% from INR 42,380/t in May and down nearly 4.7% from the April peak of INR 43,505/t.

Rebar (Fe 500) fell to INR 46,504/t in June, marking a 2.2% drop from May and a total decline of 4.5% since April.

The downtrend indicates continued price correction in the secondary steel segment, with producers likely facing margin pressure amid reduced buying interest. The outlook remains cautious as the market awaits signs of demand revival.

Overview of Mumbai steel market

Rebar (Fe 500) prices on the Mumbai IF route remained stable at INR 43,500/t exw. Limited buying interest, driven by immediate requirements and exacerbated by ongoing rainfall, is contributing to the subdued sentiment. Scrap (HMS 80:20) is currently priced at INR 30,800/t DAP, while the conversion spread between scrap and billet stands at approximately INR 8,500/t.

Upcoming scrap auctions

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 5,100-5,400/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $333-335/t, which equates to approximately INR 30,824/t (including freight). Today, local HMS (80:20) prices in Mumbai remained stable at INR 30,800/t DAP. Indicative prices of shredded from Europe stood at $360/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 14,150/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply