- Monsoon slows down construction activity

- Billet, sponge iron prices decline m-o-m

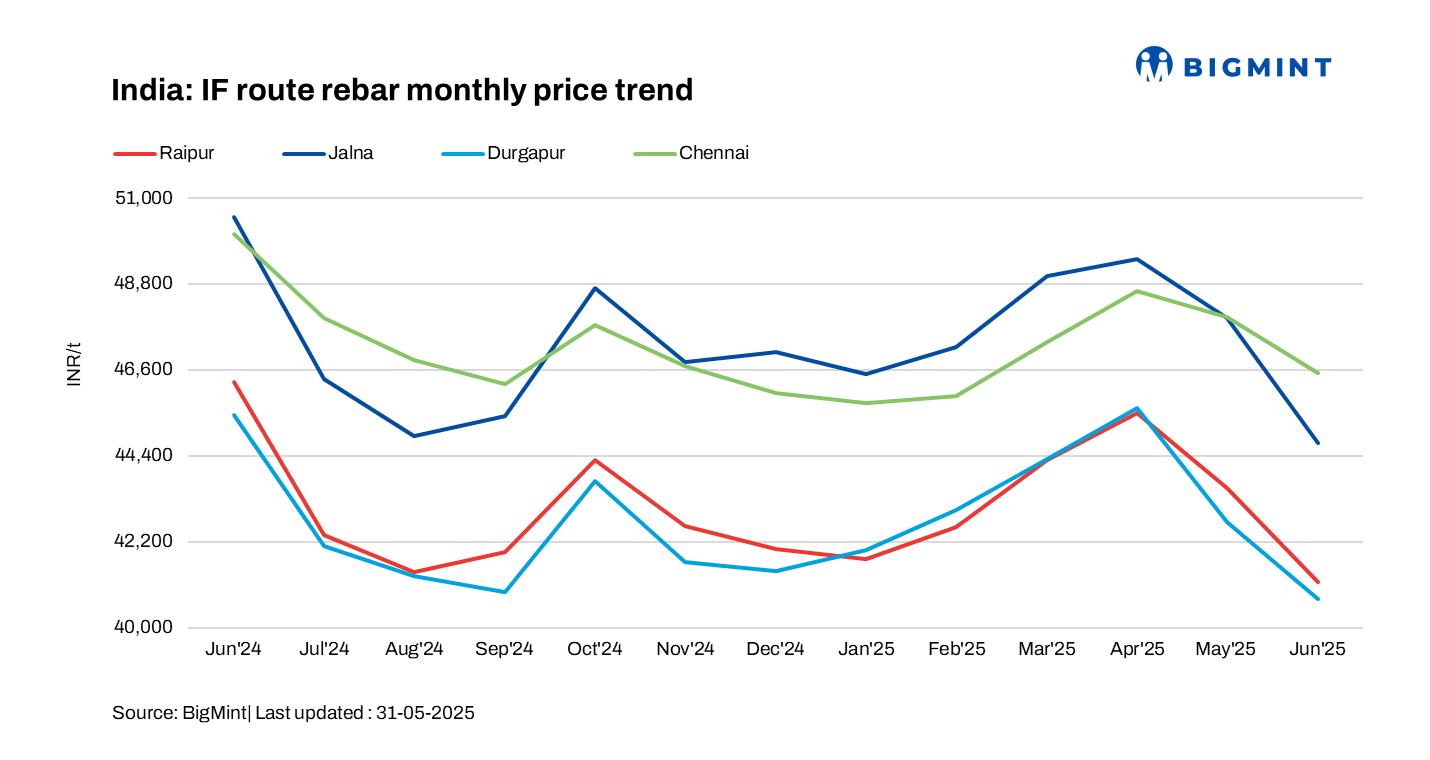

India’s induction furnace (IF) rebar prices registered a sharp decline of INR 1,000-2,800/tonne (t) m-o-m in June 2025 across major regions, as per BigMint’s assessment. The correction was primarily driven by weak demand, cautious buying behaviour, and declining raw material prices.

The most significant price drops were recorded in the western region, with Ahmedabad witnessing a fall of INR 2,800/t m-o-m and Mumbai trailing close with a reduction of INR 2,700/t.

In central India, Raipur, a key production hub, reported a decline of INR 2,600/t m-o-m. Northern markets also softened, with Mandi prices falling by INR 1,000/t and Delhi by INR 1,500/t.

The southern markets followed the same trend, as Bengaluru and Chennai saw declines of INR 1,400/t and INR 1,300/t m-o-m, respectively.

Overall, the market continued to reflect subdued sentiment, with buyers refraining from bulk bookings. Purchasing activity remained largely need-based, as demand from both the project and retail segments slowed considerably. Uncertainty over pricing trends, the impact of the ongoing monsoon, and falling raw material prices further dampened market confidence.

To stimulate sales and manage rising inventories, manufacturers were compelled to reduce offers and extend trade discounts. Despite these measures, inventories across mills increased, with holding periods stretching from 12 days in May to 12-15 days in June, indicating slower order intake.

As per JPC data, India’s total rebar production through the IF and BF routes stood at 49 million tonnes (mnt) in FY’25, marking a significant 10% rise from around 44.5 mnt in FY’24. Additionally, IF-route rebar production reached 6.8 mnt during April-May in FY’26, up from 5.9 mnt recorded during the same period last year, indicating continued growth momentum.

Factors impacting market

Raw material prices drop m-o-m: The decline in finished steel prices was largely driven by a drop in prices of key raw materials – steel billets and sponge iron – used in IF-route production. Weakened buying interest and limited trade activity across several markets prompted manufacturers to cut prices. Considering the Raipur market as a benchmark, billet prices fell by INR 2,150/t m-o-m to INR 37,000/t exw, while sponge iron (PDRI FeM 80% +/- 1) saw a sharper decline of INR 1,200/t m-o-m, settling at INR 22,400/t exw (prices taken from 31 May to 30 June 2025). Notably, billet prices were at a 10-month low in June, matching prices last seen in September of the previous year.

Market sees monsoon slowdown, buyer resistance: The early onset of the monsoon, traditionally a lean period for construction, dampened infrastructure activity, further weakening steel demand. Coupled with this, prevailing bid-offer gaps and expectations of additional price corrections made buyers hesitant, prompting many to delay purchases and adopt a wait-and-watch approach.

BF-route prices drop m-o-m: Trade-level blast furnace (BF)-rebar prices dropped by INR 3,700/t m-o-m to an average of INR 52,500/t exy-Mumbai amid sluggish domestic demand in June. Subdued domestic demand and slowing market activity due to the onset of the monsoon weighed on prices. The gap between IF and BF-route rebar prices was at 7,700/t.

Outlook

Market participants expect the finished steel market to remain under pressure in the near term amid weak demand and cautious buying. Any price recovery will depend on a post-monsoon demand revival and raw material cost movements.

Leave a Reply