- Guinea’s bauxite exports to India drop 88% y-o-y in Q1

- Gujarat bauxite output surges, offsets eastern India’s shortfall

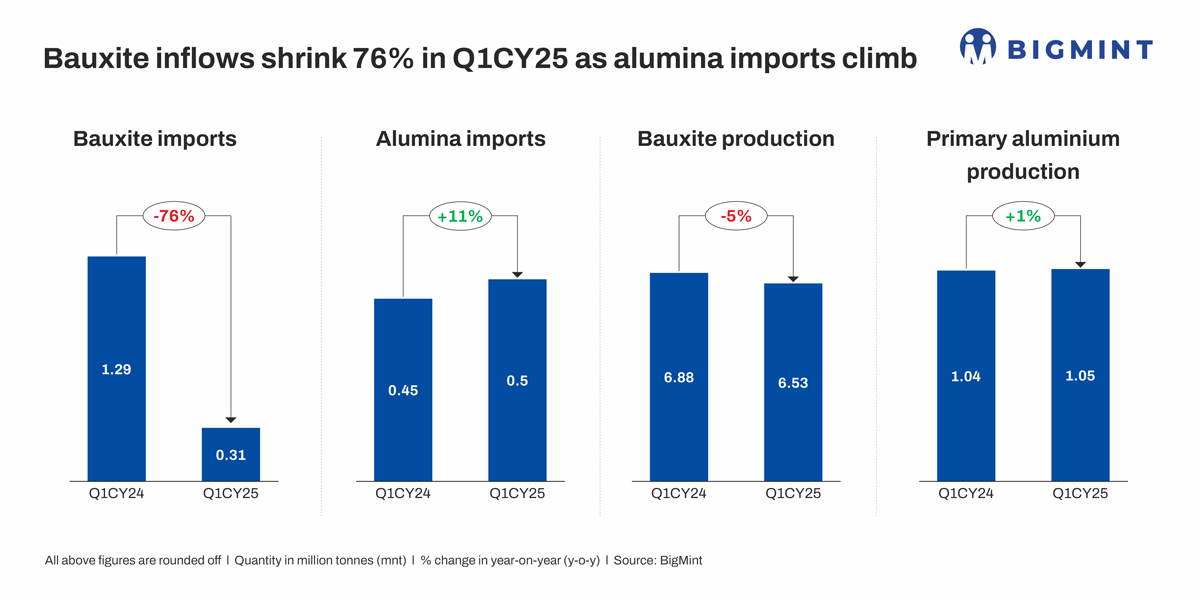

India’s bauxite import volumes fell sharply in the first quarter of calendar year 2025 (Q1CY25), down 76% y-o-y to 0.31 million tonnes (mnt) from 1.29 mnt in Q1CY24. What makes this fall even more notable is that it occurred despite a 5% dip in domestic production, which stood at 6.53 mnt versus 6.89 mnt a year earlier.

In contrast to bauxite, alumina imports rose 11% y-o-y to 0.5 mnt in Q1CY25. This uptick indicates a shift toward importing value-added material — likely to bridge quality gaps or compensate for raw bauxite shortages, particularly among producers without captive refining capabilities.

Despite India’s abundant bauxite reserves its bauxite imports continue to rise–even as domestic production grows—due to a mix of structural and regulatory challenges. Delays in mine auctions, such as the stalled Karlapat block in 2021, and disruptions like the abrupt halt of Vedanta’s public hearing on the Sijimali project, reflect broader hurdles in mine development.

At the same time, India’s rapidly expanding aluminium industry demands a stable and scalable raw material supply. Until domestic mining bottlenecks are resolved, imports will remain a key part of India’s bauxite supply chain.

Gujarat output cushions eastern region’s shortfall

The regional output story paints a mixed picture. Odisha, the country’s leading bauxite-producing state, saw output fall by 13%, while Jharkhand registered a 10% decline. In contrast, Gujarat nearly doubled its production (+98%), helping partially offset shortfalls elsewhere.

Country-wise imports

Guinea, traditionally India’s most important bauxite supplier, cut shipments by a staggering 88%, from 1.25 mnt in Q1CY24 to just 0.15 mnt in Q1CY25. The drop stems from weather-related disruptions during Guinea’s rainy season and potential operational constraints. Indonesia also shipped 18% less bauxite to India during the quarter.

In response, Indian importers diversified their supply base. Imports from Vietnam jumped 133%, and volumes from other smaller countries surged by 286%. This strategy suggests a tactical response to supply risk, aimed at reducing reliance on a few large exporters.

Domestic primary aluminium output steady

Despite raw material volatility, India’s primary aluminium production remained steady. Output in Q1CY25 rose marginally by 1% y-o-y to 1.05 mnt.

Major producers Vedanta (0.45 mnt), Hindalco (0.33 mnt), and Nalco (0.12 mnt) — maintained previous output levels. Only Balco recorded notable growth, with a 7.1% increase in production to 0.15 mnt.

Vision for raw material self-sufficiency

A key pillar of India’s Aluminium Vision is achieving self-reliance in raw materials–bauxite and alumina–by 2035. Despite producing 24 mnt of bauxite and 7.6 mnt of alumina in 2024, India still imported 3.8 mnt of bauxite and 2.5 mnt of alumina. Rising demand and supply gaps have driven imports, but the government plans to scale domestic output to meet 100% of needs, reducing dependence on imports and lowering the carbon footprint linked to transport and extraction.

Leave a Reply