- Excess pellets capacities boosted sponge output

- Cheaper coal prices dragged down sponge tags

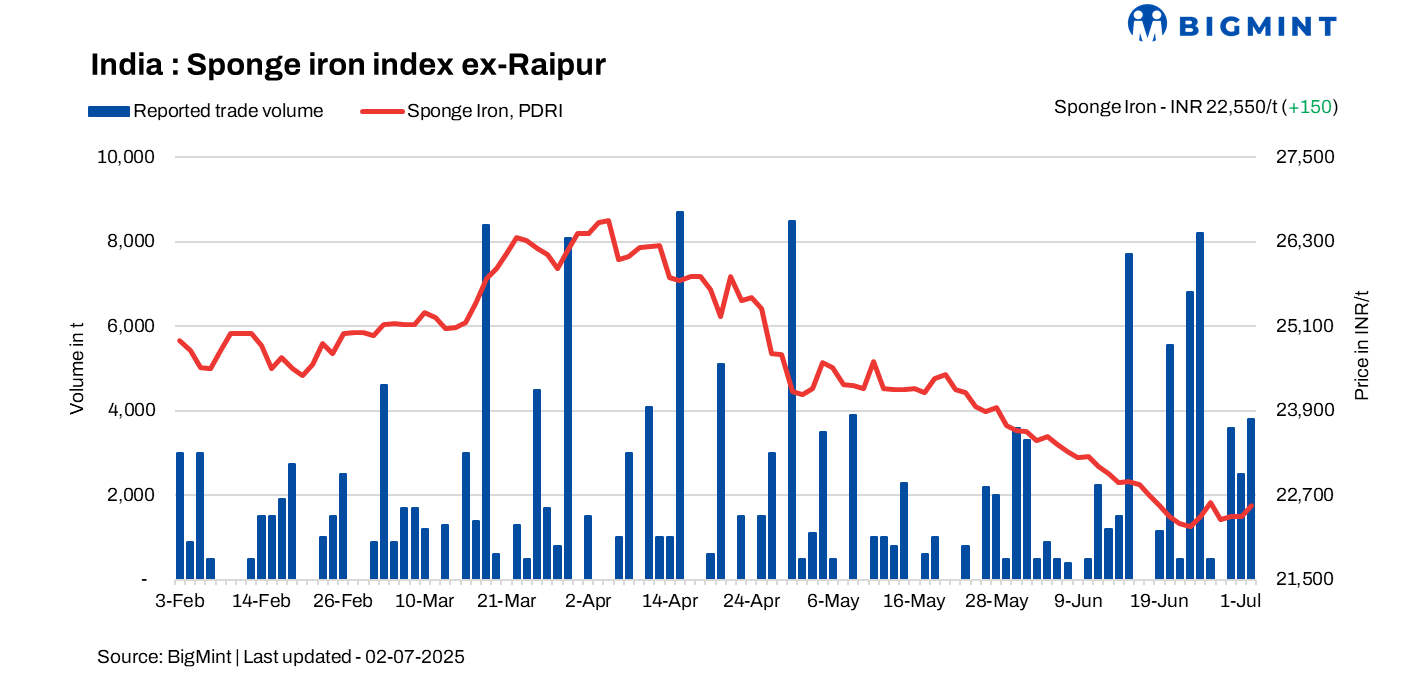

- DRI consumption seen rising post-monsoon

Sponge iron production has been steadily rising. From around 44 mnt in FY23, it increased to around 52 mnt in FY24 and further to around 55.6 mnt in FY25. January to May 2025 data also tells a similar story of a northward-headed graph. But the growth in India’s crude steel production, with which sponge iron’s fate is intrinsically linked, has slowed from 13% in FY24 to 5% in FY25.

Sponge iron prices, on the other hand, while spiking intermittently, have been showing a downward graph over the last few years. So, why is sponge production rising, when demand seems to be ebbing?

BigMint discussed some key issues at a recent webinar on,”How has the Indian sponge iron market fared in 2025? How will H2FY26 pan out”

Key take-ways from the webinar

Why is sponge production in excess?

- Growth in sponge iron production was around 8% last year with the growth from the smaller players at 14%, which was matched by expansion in crude steel production in the secondary sector. These players set up DRI capacities for captive consumption but also sold in the market. Hence, capacity addition will continue and be commensurate with the growth rate of the secondary steel producers, which will be at 8-10%. However, sponge capacities, which were planned 2-3 years ago, have already started but consumption failed to keep pace with the same.Akhilesh Kumar, Chief of Procurement – Bulk Commodities and Industrial Gases, at Tata Steel, indicated the government’s vision of 300 million tonnes by 2030 may not be met considering the current rate of crude steel production. “However, the preparedness of the producers was there – whether primary or secondary. Thus, all secondary producers in expansion mode have gone ahead with addition of DRI capacity as well. So crude steel capacity is coming up but pace is slow and getting aligned with the slowed demand,” he informed.

- Excess pellets production in India also boosted sponge iron production. Pellet production ramp-up led to its additional availability. The export duty (on pellet) slapped a few years back had a backlash when domestic sponge producers increasingly started converting these into PDRI as a feed for domestic induction furnaces. “Now, it is a matter of cost – PDRI versus calibrated DRI, pig iron versus scrap. And even if you need to buy pellets and convert into PDRI, it will still make sense in the hot metal at 60-70% share. Most IFs, especially in eastern India, are using PDRI because it is providing an edge in cost,” informed Vivek Adukia, Chairman of the Steel Re-Rolling Mills Association of India, Vice-President of the West Bengal Sponge Iron Manufacturers Association and Director of Adukia Group of Industries.

- Availability of iron ore becomes a big challenge in the monsoons and with the rains having arrived a tad early this year, iron ore availability remains tight. “Iron ore-based DRI is getting scarce because of the shortage and high prices of lumps. Thus, bulk of DRI production is pellet-based,” added Adukia.Kumar said: ”DRI capacity is in excess at this juncture. Using 100% CDRI is not viable at current prices. So CDRI is being used only by those players who have their own mines – Rungta, Tata Steel etc. That is why CDRI availability is poor in the market… while PDRI is in excess”

Why has consumption fallen?

Sponge iron consumption growth has fallen from 21% in FY24 to 7% in FY25. Several factors are responsible for this scenario. One is the increased power tariffs across states, which has impacted demand of DRI end-users – namely billet and TMT manufacturers. Secondly, geo political factors like the Indo-Pak tensions dented demand. Thirdly, government spending has also dropped from an envisaged INR 1 lakh crore per month.

Price plunge a function of cheaper raw materials

- The drop in sponge iron prices is mainly due to the availability of coal and 30% correction in imported South African RB1 prices from $125/t a year back to around $90/t at present. RB2 is at around INR 7,500/t at Dhamra from around INR 10,500/t 3-4 months back, observed Adukia.

- Domestic coal availability from CIL has also increased. Either some portions at the auctions are going abegging or being sold at the base price. The linkage auctions quantities have also been enhanced and sponge player are hopeful this will increase during crunch time in Q1, next fiscal.”Commercial mining has also increased production by additional 150 mnt. So thermal coal prices will remain on lower side while scrap will be scarce,” said Kumar.

- Thanks to excess pellet production of around 100 mnt, PDRI production will be used as the primary feed and help IF units to survive.

- But Adukia warned there is a question of viability of the sponge iron units. Fines availability is not favourable for the industry plus pellet prices in the last few days have increased by INR 400-500/t. However, prices have been fluctuating on and off and dipped slightly in Raipur but up in Durgapur at the time of publishing this article.

Coal usage pattern

- Most IF producers use at least 30-40% of sponge in their feed. In the north, this has gone up from 10-15% to around 50% today because of scarce scrap and an increasing tilt towards sponge. So higher DRI consumption from IFs will definitely push up steel prices.

- Smaller DRI units in WB are using 80-90% and some even 100% of domestic coal. But larger kilns of 350-900 tpd capacities, are using 70-80% imported coal. With fall in prices as well as availability of higher GCV domestic coals some units have switched to 70% imported and 40% domestic coals.

Outlook

Due to the CRR cut, INR 2.5 lakh crore of extra investible funds are available with the banks which will give a big boost to the infra and capital goods industry. Moreover, interest rates have also been corrected twice by 50 basis points twice. So, these factors will support investments.

“The investment cycle will start from the next two quarters and gain momentum in the next financial year. And the investments and production growth in sponge iron will be at 14-15% over the next 3-4 years. This will be further supported by the spurt in infra construction, rail expansion, housing demand pick-up in metros and tier 2-3 cities from private players. Housing schemes from governments will also trigger steel demand, added Adukia.

Adukia sees PDRI prices, which are at INR 22,000/t in Durgapur to rise to around INR 28,000-29,000/t after Q3, thanks to greater demand from infra which will trigger TMT sales.

Kumar warned, iron or prices may rise a bit which may push up sponge prices from Q3 but demand for steel may not be favourable which may again pressure down sponge prices. He added, “DRI prices will be stable in the short term being already at four-year lows but recover lost ground Q3 onwards.”

However, Adukia is upbeat that consumption will increase because of tight scrap availability in western and northern India, since most developed countries are decreasing export of the same. “Material has been moving from West Bengal, Odisha and Chhattisgarh towards the north and west. The low consumption trend will get phased out after monsoons. Plus, eased geopolitical factors will help. I foresee huge demand, based on our Budget and 3- and 5-Year plans,” Adukia said.

Leave a Reply