- Charterers opting for shorter-haul regional trades

- Chinese production curbs, port stocks hit freights

Dry bulk freight rates on key global routes continued to decline, driven by weak cargo demand, production curbs, and vessel oversupply. From India to China, freight rates dipped primarily due to reduced cargo volumes and limited spot enquiries. Indian exporters, particularly in the iron ore and coal segments, have curtailed shipments amid subdued Chinese demand, driven by steel output restrictions and high port inventories. This has resulted in excess vessel availability, intensifying competition and placing downward pressure on rates.

Additionally, the broader market sentiment has been sluggish, with muted activity from major exporting regions such as the US Gulf and South America. The lack of strong forward bookings and uncertainty around macro-economic factors, including China’s real estate concerns and slower-than-expected industrial output, have made charterers hesitant. This cautious stance, combined with vessel owners holding back from committing — in hopes of a market rebound has further contributed to the current softening of freight rates on the India-China dry bulk corridor.

Capesize freight rates are falling mainly because there’s not enough cargo coming out of the Atlantic region, especially Brazil and West Africa. Too many ships are available while fewer cargoes are being fixed, which is forcing owners to lower their offers to stay competitive.

In contrast, the Pacific market is somewhat active with regular fixtures from major miners like Rio Tinto and BHP. But even there, the rates are only slightly improving, and not enough to lift the whole market. Offers in the Pacific dipped slightly through the day, showing that momentum is still weak.

This combination of high vessel supply and soft demand is pushing Capesize freight levels down steadily.

Factors influencing freights

- Baltic indices decrease w-o-w, BSI goes contrarian: The Baltic indices, indicating trends in vessel demand, fell w-o-w. The Baltic Dry Index (BDI) was recorded at 1,521 on 30 June, decreasing by 168 points w-o-w. Additionally, the Baltic Capesize Index (BCI) stood at 2,220, sharply down by 659 points w-o-w. However, the Baltic Supramax Index (BSI) inched up by 36 points w-o-w to 1,009.

- China’s iron ore spot prices remains firm w-o-w: Chinese spot prices of iron ore fines (Fe62%) were assessed at $93.15/t CFR on 1 July, remaining stable w-o-w as fresh bookings provided a degree of support, even as overall market sentiment stayed subdued due to production curbs and weak downstream demand. While port-stock prices held steady, buyers showed increased interest in mid-grade fines for cost efficiency and growing acceptance of high-phosphorus cargoes amid limited high-grade availability. However, tightened environmental norms leading to lower sintering and pig iron output in major hubs, along with reduced seaborne activity, kept price movements in check.

Route-wise updates

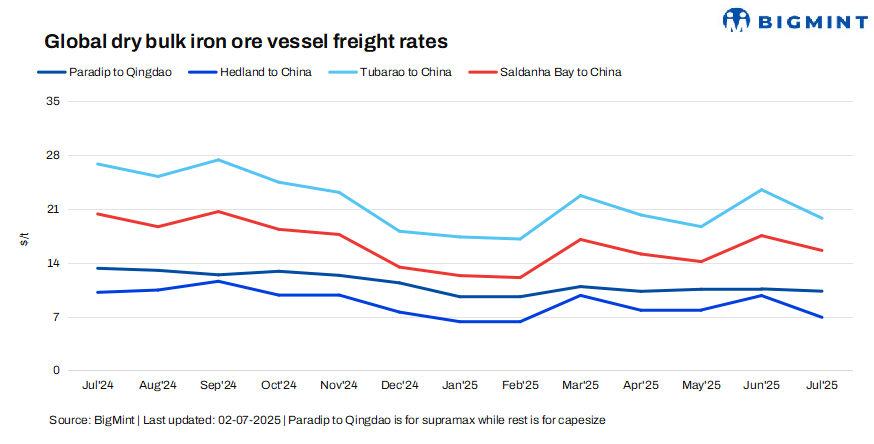

- India-China: Freights from the Indian Ocean to China were recorded at $10.3/t, inching down by $0.2/t w-o-w amid limited fresh cargo enquiries. An oversupply of tonnage and sluggish activity in the Asian market contributed to the decline. Some fixtures are still under negotiation.

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $6.9/t on 2 July, decreasing by $2.1/t w-o-w. According to sources, major Australian miners Rio Tinto and BHP booked Capesize vessels from a Western Australian port to Qingdao at around $6.95-7.35/t. Shipment is scheduled for 14-18 July.

- Brazil-China: Freights for Capesize vessels from Brazil to China fell this week. Rates from Tubarao to Qingdao Port were assessed at $19.8/t on 2 July, down by $3/t w-o-w. As per sources, two Capesize vessel got booked from Tubarao to Qingdao at $20.35-22.25/t for the shipment period of 16-27 July.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao dropped by $1.70/t w-o-w to $15.6/t on 2 July due to a lack of fresh fixtures and subdued chartering activity during Asian trading hours. Weak demand for cargoes from the region limited market movement. Additionally, an oversupply of tonnage continued to weigh on sentiment.

Leave a Reply