- HRC export offers to the EU drop w-o-w

- Chinese offers to the Middle East remain stable

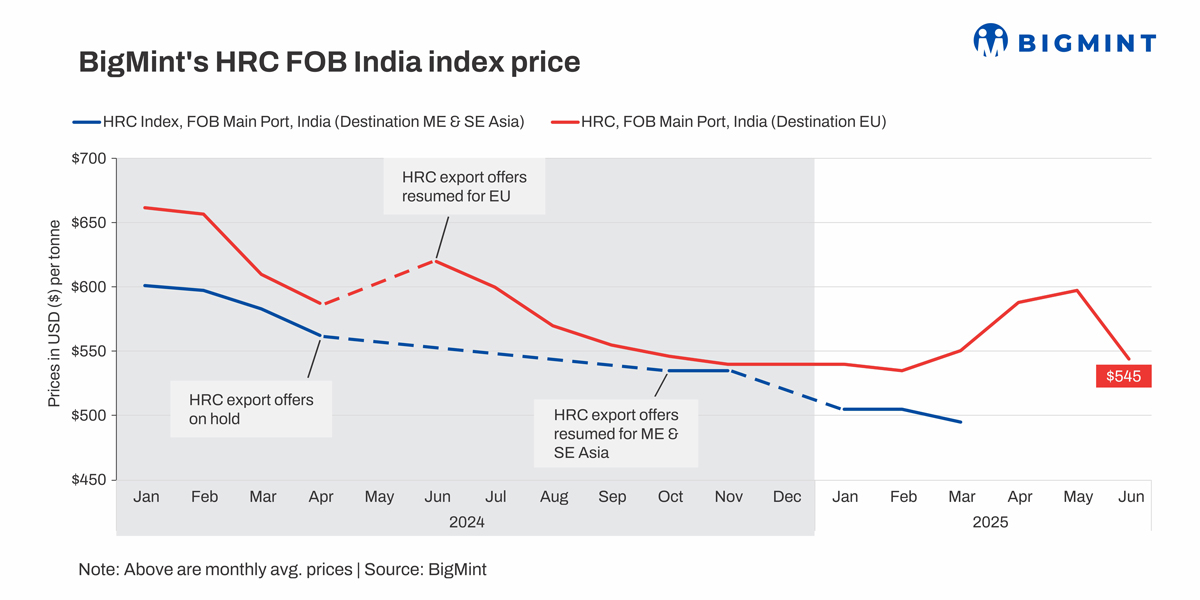

BigMint’s India HRC (S275) exports index declined by $5/tonne (t) w-o-w to $545/t FOB main port, reflecting the impact of sluggish domestic demand and a cautious buying approach driven by summer slowdown. Meanwhile, the Middle East market remained challenging for Indian mills, amid ongoing geopolitical tensions and competitive pressures from other regions.

1.Chinese HRC offers to ME steady w-o-w: Chinese HRC (S235 and S275) export offers to the ME remained range-bound w-o-w at $475-480/t CFR UAE. Furthermore, the market sentiment remains slow amid ongoing geopolitical tensions and seasonal summer slowdown.

Notably, a Middle Eastern re-roller has booked 25,000t of Japanese HRCs for August-September shipment at similar price levels, sources informed BigMint.

Meanwhile, Indian mills have kept their HRC offers to the Middle East on hold due to competitive prices and stronger domestic realisations.

2.Chinese HRC offers to Vietnam stable w-o-w: Chinese HRC (SAE1006) export offers to Vietnam remained stable at $475/t CFR Ho Chi Minh City (HCMC), with the Vietnamese HRC import market continuing to see muted activity.

Moreover, Vietnam imported 1.29 mnt of steel in May, reflecting a 5.8% m-o-m drop from 1.37 mnt in April, with China, Japan and Indonesia being the major exporters.

Meanwhile, HRC futures on the Shanghai Futures Exchange (SHFE) increased by RMB 15/t ($2/t) w-o-w to RMB 3,121/t ($436/t) as compared to RMB 3,106/t ($434/t) a week ago. However, on a d-o-d basis, the same edged down by RMB 13/t ($2/t) from RMB 3,134/t ($438/t) a day ago.

3. Indian HRC export offers drop w-o-w: Indian HRC export offers to the EU declined by $5/t w-o-w to $595/t CFR Antwerp ($545/t FOB main port India) as compared to $600/t CFR last week. European HRC prices are under pressure, with producers indicating that further declines may be limited due to rising input costs and tightening margins. Demand remains sluggish, impacted by weak activity in construction and automotive sectors, competitive import offers from Asia, and the seasonal summer slowdown. Buyers remain hesitant, adopting a wait-and-watch approach amid uncertainty over near-term price movements.

Notably, the European Union’s steel import quota utilization remains modest in several product categories. India being one of the largest exporters to the EU has only modestly consumed its HRC quarterly quota volume by merely 51,213 t out of 773,831 t.

Outlook

The Indian export market is expected to remain subdued. While there might be some short-term volatility, the prevailing sentiment points towards a challenging period for HRC exports due to a combination of weak demand, oversupply, and geopolitical factors. Moreover, market participants are awaiting Indian mills’ price announcement for July.

Leave a Reply