- Construction slowdown continues to weigh on rebars

- Domestic, imported coal hold firm but trades sluggish

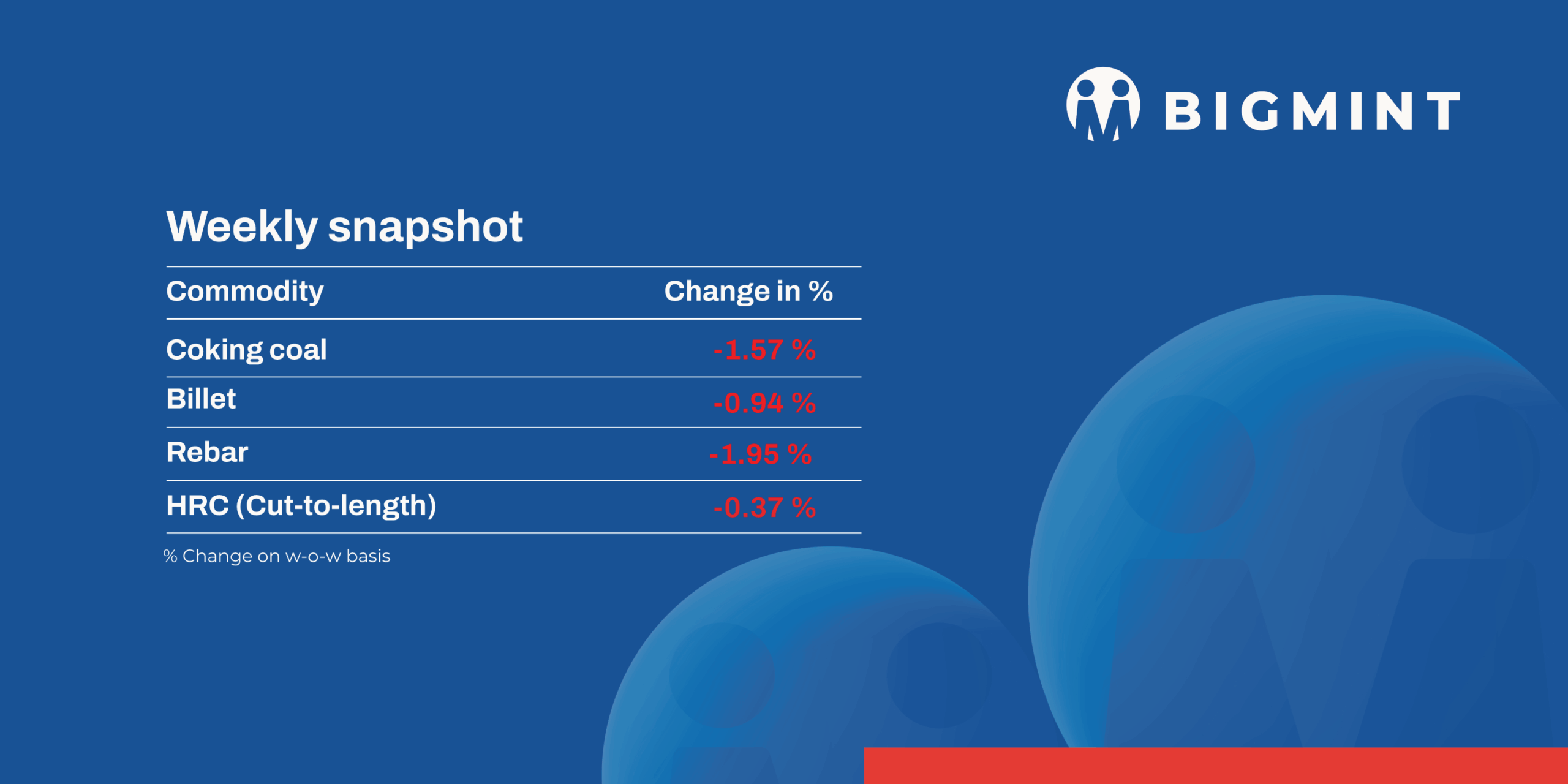

Indian steel and raw material prices continued to trend down this week across most markets, as demand remained weak, resulting in sluggish activity. Coal prices, however, remained stable, while some ferro alloy commodities witnessed gains.

Additionally, domestic induction furnace (IF) finished long steel offers declined by INR 100-1,200/t, and trade-level blast furnace (BF) rebar prices dropped due to muted demand. To stimulate buying interest, primary mills extended rebates and discounts on their listed prices.

Iron ore, pellets

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, inched down by INR 50/tonne (t) ($0.5/t) w-o-w to INR 9,150/t ($107/t) DAP Raipur on 27 June compared to last week. Raipur-based pellet producers kept their offers for Fe 62/63% (+/_0.5%) material stable at INR 9,000-9,100/t ($105-106/t) exw. Deals for around 46,000 t were recorded in Raipur this week by local sellers at these levels.

- NMDC conducted an auction for 193,200 t of iron ore from its Bacheli mines, Chhattisgarh, on 26 June. The entire 17,200-t DRCLO (10-40 mm, Fe 67%) lot was booked at a base price of INR 7,110/t. Meanwhile, around 172,000 t of Baila fines (Fe 64%) and 4,000 t of Baila lumps (10-20 mm, Fe 65.5%) remained unsold. Prices were on FOR basis, inclusive of royalty, DMF, and NMET.

- Lloyds Metals and Energy has received an environmental clearance (EC) to expand its iron ore mining capacity to 55 MTPA (26 MTPA haematite initially, later ramping up to 55 MTPA, including 45 MTPA BHQ), positioning its mine in Gadchiroli as India’s largest iron ore operation.

Coal

- South African portside coal prices held steady this week despite an uncertain market. RB2 (5500 NAR) was assessed at INR 7,600/t and RB3 (4800 NAR) at INR 6,600/t exw-Gangavaram. CNF deals were heard at $76/t for RB2, with FOB deals at $66-68/t. Portside stocks dipped, while sponge iron prices showed marginal gains, but overall market sentiment stayed cautious.

- Domestic coal prices remained unchanged this week, with 5000 GCV and 4500 GCV grades assessed at INR 4,700/t and INR 4,250/t exw-Bilaspur, respectively, as per BigMint. Market activity stayed subdued due to poor industrial demand. SECL’s recent auctions witnessed limited buyer participation, reflecting ongoing caution and uncertainty in the market amid the monsoon season and sluggish offtake.

- Met coke prices in India dropped further amid weak steel sector demand and ongoing policy uncertainty. As per BigMint’s assessment on 25 June, the 25-90 mm BF grade slipped by INR 1,000/t w-o-w to INR 28,000/t ex-Jajpur, while prices in Gandhidham edged down by INR 150/t w-o-w to INR 29,000/t. Limited buying and a lack of clarity regarding the quantitative restrictions (QR) policy kept market sentiment subdued, despite signs of stability in China’s coke market.

Ferrous scrap

- India’s imported scrap market stayed sluggish all week, with UK-origin shredded at $360/t CFR, down 1% from last week’s $362/t, pressured by weak finished steel demand, monsoon disruptions, and ample domestic supply of sponge iron and scrap. Buyers remained cautious, as falling rebar prices and freight uncertainties from geopolitical tensions added further hesitation to import decisions.

- Shredded offers from the UK/EU hovered at $355-360/t CFR, but tradable levels dipped to $350-355/t amid low buying interest. HMS 80:20 from West Africa was steady at $335-340/t CFR, while UK HMS slipped slightly to $330-335/t CFR as sellers mostly held back fresh offers.

- Total imported scrap volumes into India last week were captured at around 2,000-2,500 t.

Ferro alloys

- Silico manganese: Indian silico manganese prices (60-14) witnessed a slight increase of INR 200/t ($2/t) w-o-w to INR 71,500-72,300/t ($836-846/t) in the key regions of Durgapur, Raipur, and Vizag. Leading smelters strategically cut production levels, resulting in a slight price recovery in certain areas. This deliberate output control helped stabilise the market and curb further price drops.

- Ferro manganese: Indian ferro manganese (HC 70%) prices went up by INR 300/t ($4/t) w-o-w to INR 71,900/t ($841/t) exw in Durgapur. Meanwhile, prices, exw-Raipur, also increased to INR 72,100/t ($843/t). The upward movement was largely attributed to material shortages, which tightened supply and supported the modest price gains.

- Ferro silicon: Indian ferro silicon prices dipped by INR 400/t ($5/t) w-o-w to INR 88,400/t ($1,034/t) exw-Guwahati. Concurrently, Bhutanese prices also decreased by INR 400/t ($5/t) to INR 88,000/t ($1,029/t) exw. The price dip was driven by limited inquiries, prompting sellers to reduce offers to stimulate trade.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices edged down by INR 400/t ($5/t) w-o-w to INR 100,000/t ($1,170/t) exw-Jajpur. Prices fell following a drop in bids at major auctions last week by the Odisha Mining Corporation (OMC) for chrome ore and Vedanta-FACOR for ferro chrome.

- At Vedanta-FACOR’s ferro chrome auction on 23 June, the larger lot of 10-150 mm secured an H1 price of INR 99,200/t ($1,143/t) exw, marginally above the base price of INR 99,000/t ($1,141/t). Additionally, OMC’s ferro chrome auction on 25 June saw limited interest, with just 300 t sold of the 6,900 t offered.

Semi finished

- Indian semi-finished steel prices declined, as per BigMint’s assessment. Domestic billet prices in all key locations decreased by INR 100-600/t across regions, with the steepest fall of INR 600/t in Goa. However, sponge iron prices showed a fluctuating trend. Most locations saw prices moving up by INR 100-700/t, with the highest increase of INR 700/t seen in Chennai. However, in other regions, there was a fall of INR 50-250/t.

- Indian direct reduced iron (DRI) export offers stood firm at $315/t for CPT Raxaul, while CPT Benapole offers were stable at $325/t.

- SAIL-Bokaro Steel Plant (BSL) held an auction for 3,000 t of steel-grade pig iron on 26 June. The total quantity was booked at an average price of INR 31,450/t exw (by road transportation). In the previous auction, conducted for 17,500 t on 29 May, the entire quantity was sold at an average price of INR 30,780/t exw (by rake).

Finished long steel

- IF rebar: India’s IF-route rebar prices remained under pressure this week, despite a slight pick-up in trading activity. A modest quantity was booked, with buyers expecting prices to decline further. Moreover, manufacturers further reduced prices to encourage sales. Inventory levels were indicated to be at around 12-15 days. Market participants expect the market to remain subdued in the near term, primarily due to weak project demand and sluggish construction activity amid the ongoing monsoon season.

-

On a w-o-w basis, rebar steel prices declined in the range of INR 100-1,200/t across regions, except in Jalna, where prices rose by INR 800/t, as per BigMint’s assessment.

-

Trade reference prices of Fe 500 grade rebars manufactured via the IF route for the 10-25 mm size were assessed at INR 40,000-40,400/t exw-Raipur and INR 44,000-44,600/t exw-Jalna.

-

Trade reference prices of heavy structural steel for the base size 150-mm channel stood at INR 42,000-42,500/t exw-Raipur.

-

Trade reference prices of wire rod hovered at INR 41,300-41,800/t ex-Raipur.

- BF-rebar: India’s trade-level BF rebar prices declined w-o-w, weighed down by subdued domestic demand and slowing market activity due to the onset of the monsoon. Market sentiment remained cautious, with buyers refraining from bulk purchases amid persistent bid-offer gaps, while distributors aimed to offload previously procured high-cost inventories.

- Trade-level BF rebar prices declined by INR 1,200/t w-o-w to INR 50,700/t exy-Mumbai, as per BigMint’s assessment on 27 June. Prices are exclusive of GST at 18%.

- Buying activities in the project segment remained subdued, with limited orders being placed amid ongoing concerns over further downward price corrections. Prices hovered at around INR 49,500-50,000/t on a landed basis. Mills continued to face challenges in securing bookings due to stiff market competition.

Flat steel

- Trade-level prices of hot-rolled coils (HRCs) in India declined marginally by up to INR 500/t w-o-w to INR 50,600-52,500/t ($596-616/t) across markets. Meanwhile, cold-rolled coil (CRC) prices declined marginally by up to INR 300/t w-o-w to INR 56,200-60,700/t ($659-718/t).

- The market waited for clarity on whether mills will provide price support. Meanwhile, demand continued to be weak, with fewer inquiries and an even slower rate of them converting into actual sales.

- India’s bulk imports of HRCs and plates touched 214,961 t as of 23 June, based on vessel line-up data from BigMint. Around 48,946 t of additional cargo are expected by end-July and another 69,748 t in July 2025.

- BigMint’s India HRC (S275) export index fell by $5/t w-o-w to $550/t FOB main port, following a 5,000-t deal to the EU. Buyers remained cautious amid expectations of a summer slowdown, keeping pressure on prices. In the Middle East, weak sentiment due to geopolitical tensions continued to impact demand. Indian mills held back HRC offers to the region amid strong competition from other suppliers.

Leave a Reply