- India buyers prefer sponge iron amid falling rebar prices

- Turkiye market steady as buyers await clearer rebar cues

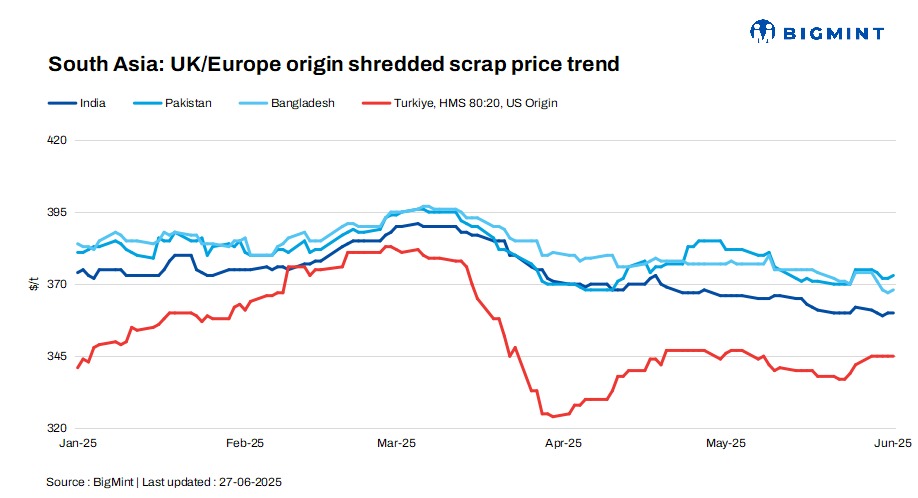

Imported scrap markets across South Asia remained largely subdued, with range-bound prices d-o-d, as seasonal factors, weak steel demand, and geopolitical uncertainties continued to weigh on buying activity.

Indian buyers steered clear of large bookings amid falling rebar prices and competitive domestic alternatives, while Pakistani mills stayed cautious due to Middle East tensions and expected tax changes. In Bangladesh, post-Eid demand remained sluggish, with minimal trade despite stable bulk pricing.

Meanwhile, Turkiye’s market held steady, with buyers and sellers adopting a wait-and-watch stance in the face of weak downstream demand and firm seller positions.

Market overview

India: India’s imported scrap market remained subdued, as weak steel demand, monsoon disruptions, and cheaper domestic alternatives curbed buying interest. Shredded offers from the UK/EU stood at $355-360/t CFR Nhava Sheva, though tradable levels were lower at $350-355/t. HMS 80:20 from West Africa was offered at $335-340/t, with UK HMS 80:20 at $330-335/t CFR.

Mills largely preferred domestic sponge iron due to cost benefits. Falling rebar prices and freight uncertainties added to the cautious mood. Sellers held back on fresh offers, opting for a wait-and-watch stance amid unclear price direction and limited trade.

Pakistan: Pakistan’s imported scrap market remained sluggish, as mills avoided fresh bookings amid geopolitical tensions and freight-related uncertainties. UK/EU-origin shredded scrap offers were steady at $370-375/t CFR Qasim, while UAE-origin material was quoted higher at $385/t. HMS 80:20 offers from the UAE ranged within $360-365/t, with HMS 1 heard at $365-368/t.

Despite firm offers, buying interest was limited, pressured by concerns over vessel delays and rising war risk surcharges linked to Middle East unrest. Market sentiment was further dampened by a proposed 5% duty on re-rollable scrap. Domestic scrap and rebar prices held flat, with traders expecting more clarity post-fiscal announcements.

Bangladesh: Bangladesh’s imported scrap market remained subdued post-Eid, weighed down by monsoon-related slowdowns and weak construction demand. Mills continued operating below capacity, with limited interest in near-term cargoes.

Two US West Coast bulk deals were confirmed at $346-350/t CFR for HMS, with shredded and bonus grades priced at up to $360/t CFR, signalling stable pricing but muted appetite. Containerised offers for shredded hovered at $370-375/t, though buyers capped bids at $360-365/t CFR Chattogram.

Traders cited minimal booking activity and cautious sentiment amid stagnant rebar sales. “Demand is there, but it is slow-moving,” one trader said, adding that prices may soften if project activity does not improve.

Turkiye: Turkish imported scrap prices held steady amid muted trade, as both buyers and sellers stayed cautious in a subdued market. US-origin bulk HMS (80:20) offers were at $345/t CFR, unchanged from the prior day, with US- and Baltic-origin cargoes offered in the $345-350/t range.

Sellers remained firm, pointing to a balanced market supported by stable rebar prices and a strengthening euro. Buyers, however, stayed on the sidelines, citing weak downstream demand and uncertain rebar market dynamics.

‘The current price seems to reflect an equilibrium,” one recycler noted, adding future moves hinge on rebar tags and currency shifts. Euro strength continued, assessed at $1.172.

Price assessments

India: UK-origin shredded indicatives were assessed stable d-o-d at $360/t CFR Nhava Sheva.

Pakistan: UK-origin shredded indicatives stood at $372/t CFR Qasim, unchanged d-o-d.

Bangladesh: UK-origin shredded prices were assessed unchanged d-o-d at $367/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $345/t CFR Turkiye, unchanged d-o-d.

Leave a Reply