- OMC auction response may not affect offers

- Sellers stock up to avoid monsoon-related shortage

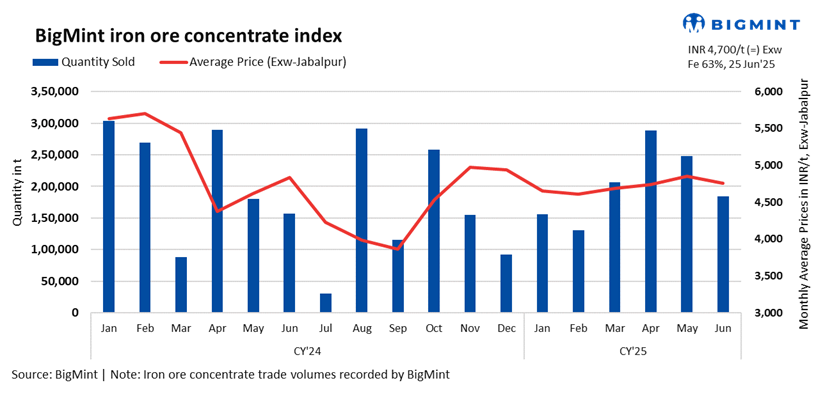

Iron ore concentrate (Fe 63%) prices in Jabalpur, India, remained stable in recently concluded deals compared to the previous assessment on 21 June 2025, with BigMint’s bi-weekly index for the same assessed at INR 4,700/tonne (t) ($55/t) exw-Jabalpur.

However, weakening sponge iron and semi-finished steel tags, along with fall in bids on monthly basis in Odisha Mining Corporation’s (OMC) recent iron ore fines auction, signal subdued market sentiment and are likely to exert downward pressure on concentrate offers.

Market players’ insights

Contrary to expectations, sellers remained hesitant towards a reduction in offers. A Jabalpur-based seller noted, ” No revision in offers. OMC activity hasn’t affected our market, but enquiries have declined.”

To avoid the usual seasonal shortage, like every time, one of the source mentioned, “We’ve already stocked sufficient raw material in preparation for the monsoons. With rains having begun here, iron ore mining is currently not possible.”

On the contrary, one of the buyer told BigMint, “Prices remain unchanged for now, but there’s a possibility of a decline.”

Rationale

- One (1) trade of 10,000 t were recorded in the publishing window. It was accorded 50% weightage.

- Ten (10) offers and indicative prices were reported, out of which eight (8) were taken into consideration as T2 trades, receiving the balance 50% weightage.

Why concentrate prices are likely to come under pressure?

- Bids fall by INR 250/t ($3/t) in OMC’s iron ore fines auction: In OMC’s iron ore fines auction (Fe 51-65%) held on 19 June, 1.025 million tonnes (mnt) (95%) out of the total 1.073 mnt on offer was booked across various lots at base prices ranging from INR 3,600-5,600/t ($42-65/t) (ex-mines). Some lots fetched premiums of INR 50-950/t ($1-11/t). The weighted average bid fell by INR 250/t ($3/t) compared to the previous month. This followed a base price cut of INR 500-700/t ($6-8/t) m-o-m by OMC. The decline in pellet and steel prices contributed to the lower bids.

- Sponge iron prices drop INR 300/t w-o-w: Sponge PDRI prices in Raipur declined by INR 300/t ($3/t) w-o-w on 25 June 2025, driven by subdued market sentiment. Buyers remained cautious and adopted a wait-and-watch approach amid market instability. Limited dispatches from moderate bookings at lower offers pressured sponge iron prices downward. Transaction volumes stayed relatively low, with buyers refraining from major commitments at prevailing rates.

- Billet index hits 4-year low amid limited buying: Despite price cuts, market activity and buying interest remained subdued, as weak sentiment and low bids continued to dampen spot trading throughout the day. Sellers in the semi-finished segment were forced to reduce spot offers to draw buyers, but the response was limited. Participants observed that the prolonged downturn in the finished steel segment has intensified market pessimism, prompting many buyers to stay on the sidelines amid prevailing uncertainty. BigMint’s billet index dropped w-o-w by around INR 550/t ($6/t) exw-Raipur on 25 June 2025.

Outlook

Market participants remain watchful for clearer pricing signals or signs of recovery in steel, iron ore, and pellet markets. While pre-monsoon restocking may continue to provide some support in the short term, persistently weak downstream sentiment poses a challenge to any meaningful price rebound.

Leave a Reply