- China, DRC account for 56% of global refined output

- India drives Asian production growth

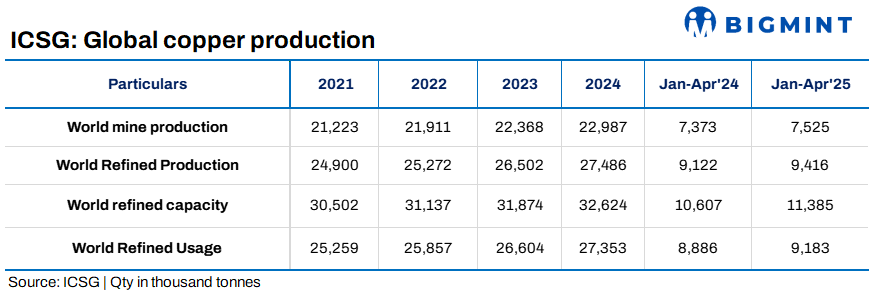

The International Copper Study Group (ICSG) has released preliminary data for January-April 2025, indicating that global refined copper production rose by approximately 3.2% y-o-y. This included a 3.3% increase in primary production (from ores via electrolytic and electrowinning processes) and a 3.1% rise in secondary production (from scrap).

The growth was largely driven by China and the Democratic Republic of Congo (DRC), which together contributed about 56% of global refined copper output and saw a combined increase of 4.8%. Asia (excluding China) recorded a 3.5% rise, led by stronger output in India.

In Indonesia, Amman refinery began cathode production in late March, while the Manyar refinery start-up was delayed to H2 2025. Japan’s production fell by 8% due to maintenance-related shutdowns. Chile’s output declined by 9.5%, with electrolytic production down 17% and electrowinning (SX-EW) output falling 5%. Overall, global secondary refined copper production increased by 3.3%, primarily supported by higher output in China.

Regional trends in refined copper production

Chile’s refined copper output fell by 9.5%, with electrolytic production down 17% due to smelter maintenance and SX-EW output declining 5%. Asia ex-China saw a 3.5% increase, driven by higher production in India. Japan’s output dropped by 8% following a smelter shutdown.

Indonesia’s Amman refinery began cathode production in late March, while the Manyar refinery’s launch was delayed to the second half of 2025.

Copper mine output rises

Global copper mine production rose by 2% y-o-y in the first four months of 2025, with concentrate output up 2.2% and SX-EW up 1.7%, supported by new projects ramping up and better performance at existing mines.

Peru’s output increased 5%, led by higher production at Las Bambas, Quellaveco, and Toromocho. DRC saw an 8% rise, driven by the Kamoa mine expansion. Mongolia’s output surged 25% due to the ramp-up at the Oyu Tolgoi underground project.

Chile’s mine production rose 3.5%, with a 6.2% gain in concentrate output offsetting a 5% decline in SX-EW. Increased output from Escondida, Centinela, Mantos Copper, and Codelco outweighed losses at Collahuasi and Los Pelambres.

Indonesia’s mine production dropped sharply by 42%, mainly due to scheduled maintenance at Grasberg and lower output at Batu Hijau due to mine sequencing. Canada and other regions also saw declines.

Refined copper usage and market balance

Global apparent refined copper usage rose by 3.3% in January-April 2025.

China’s demand grew by 6%, though net imports fell 11%. World ex-China usage was flat, as gains in Asia and MENA were offset by weak demand in the EU, Japan, and the US.

Market surplus and stocks

The global refined copper market recorded a surplus of 233,000 t in Jan-Apr 2025, rising to 298,000 t after adjusting for Chinese bonded stock changes, which increased by around 64,500 t. Combined copper stocks at LME, COMEX, and SHFE stood at 419,917 t at the end of May, down 2.4% from December.

Copper prices

The average LME cash price for May was $9,530/t, up 3.7% from April. The highest price so far in 2025 was $9,982/t on 25 March, while the lowest was $8,539/t on 9 April. The year-to-date average stands at $9,402/t, which is 2.8% higher than the 2024 annual average.

Leave a Reply