- Imports from Russia jump 212% m-o-m

- ZCE futures prices hold steady w-o-w

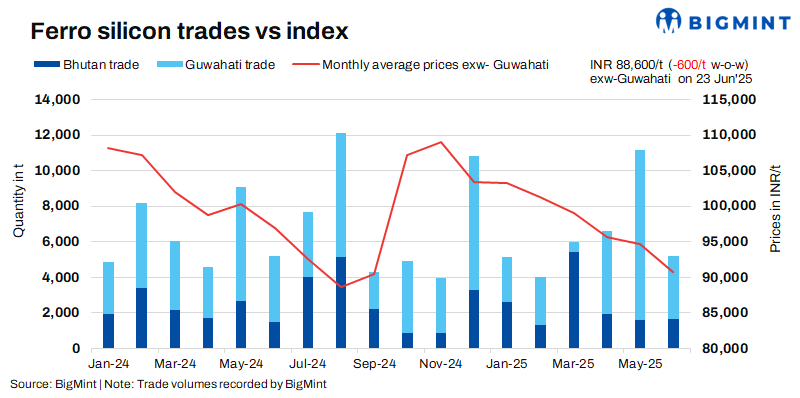

Indian ferro silicon (70%) prices kept trending lower over last week, sliding by INR 600/t ($7/t) w-o-w. Prices fell as inquiries remained limited prompting sellers to lower their offers.

As per BigMint’s assessment on 23 June 2025, ferro silicon prices in India were INR 88,600/t ($1,029/t) exw-Guwahati. In Bhutan, prices fell by INR 2,200/t ($26/t) w-o-w to INR 88,200/t ($1,025/t) exw. No deal was concluded last week as the majority of sellers were either sold out or were catering to previously booked orders.

Market summary (17-23 June)

India’s ferro silicon imports touch 2-year high: Ferro silicon imports to India reached 24,942 t in May 2025, highest ever figures since 26,900 t in July 2023. Bhutan, which usually supplies majority of the material to India, was overtaken by Russia in May. It exported 10,782 t, a rise of 212% m-o-m. With increased competition from overseas suppliers, buyers inclined towards them rather than sourcing material domestically.

Regarding silicon metal imports, a seller informed BigMint, “Ferro silicon prices are impacted by it but major Indian bulk buyers have not adapted to it yet. Only small end users are going for it.”

Update on SIMS: Recently some modifications were applied to the SIMS registration by Ministry of Steel. Under it, importers must apply for registration between 60 days and 7 days before their goods are expected to arrive in India. Once they apply, they get an Automatic Registration Number, which stays valid for 75 days.

Sources from Bhutan highlighted that applying in advance might be an issue. Earlier it was like, loading is scheduled for today. SIMS will be generated, and the consignment will exit Bhutan either today or by the next day.

Chinese market scenario: Ferro silicon (Si:75%) prices in China inched up slightly by RMB 150/t ($21/t) w-o-w to RMB 5,640/t ($786/t) exw-Inner Mongolia. Although some producers in Qinghai and Inner Mongolia planned to cut output through furnace shutdowns, but overall production levels remained high. Delivery warehouse stocks stayed elevated, indicating that supply continued to outpace demand.

On the demand side, buying interest from steel mills was weak amid a seasonal lull in downstream steel consumption. High inventories and the absence of speculative buying led to muted market activity, with transactions mostly limited to immediate needs. Spot prices showed some variations, reflecting uneven market sentiment.

On the Zhengzhou Commodity Exchange (ZCE), prices edged up by RMB 24/t ($3/t) w-o-w to RMB 5,316/t ($740/t) on 23 June for September deliveries.

Outlook

Demand continues to remain subdued so in the coming days, we might witness further correction in prices. Reports also suggest that Bhutanese players have sufficient inventories with them. So, next month offers may drop.

Leave a Reply