- BigMint’s PHCC index falls $3/t w-o-w

- HRC trade prices drop up to INR 500/t w-o-w

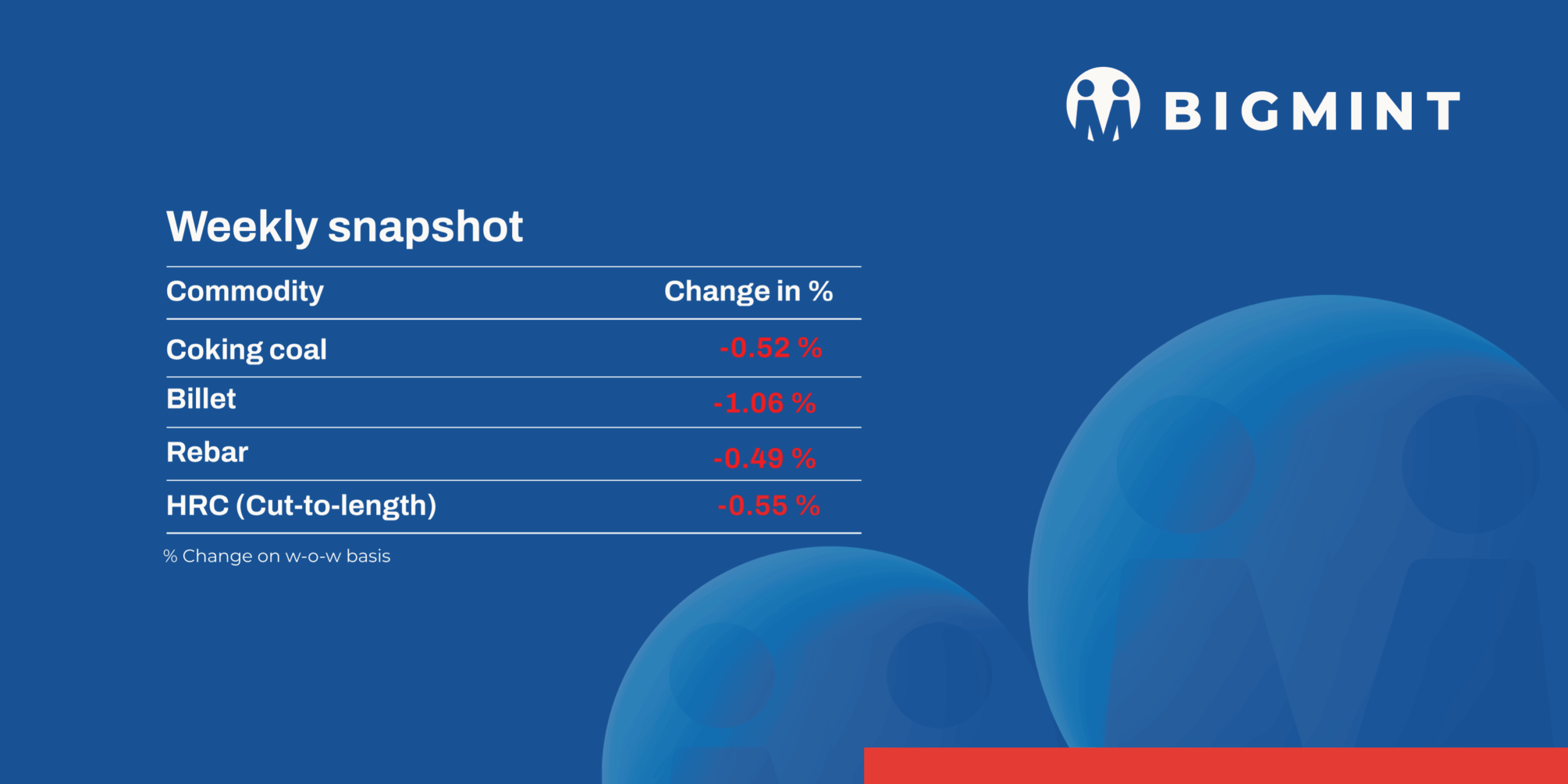

Domestic induction furnace long steel prices decrease by INR 200-1,200/tonne (t) this week even as semis continued to decline due to ongoing market weakness and decreased industry demand.

Iron ore and pellets

- OMC conducted an auction for 2.05 mnt of iron ore (0.98 mnt of lumps and 1.07 mnt of fines) on 19 June 2025. Around 1.025 mnt fines (95%) and 0.976/t lumps (almost 100%) received bids of INR 3,600-5,600/t and INR 5,150-7,500/t respectively. Bids fell by INR 250/t for fines and INR 350/t for lumps compared to the May auction. The miner reduced base prices by INR 500-700/t ($6-8/t) and INR 500/t ($6/t) m-o-m for fines and lumps, respectively. The sharp decline in pellet and sponge prices in central eastern Indian led to a drop in OMC’s base prices.

- An Indian pellet-maker concluded a deal for 50,000 t (Fe63%, 2.5% alumina) via an export tender this week. According to sources, the deal was closed at around $96/t FOB India.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index remained stable w-o-w at $60/t FOB east coast on 19 June. Deals of around 165,000 t of Fe 56-57% fines were concluded at $70-71/t CFR China in this publishing window, while a deal for 80,000 t of below Fe 55% fines was concluded on the eastern coast but is yet to be confirmed from the concerned parties.

Coal

- South African thermal coal prices dropped again at Indian ports this week due to sluggish demand and increased stock levels. RB2 (5500 NAR) fell by INR 100/t to INR 7,600/t exw-Gangavaram, while RB3 dropped by INR 200/t to INR 6,600/t. At Vizag, both RB2 and RB3 declined by INR 200/t to INR 7,450/t and INR 6,450/t, respectively.

- Sellers faced pressure to clear inventories, and some traders reportedly made low offers to influence index levels. Export prices also fell, with RB2 down to $67.50/t FOB. Sentiment remains weak ahead of Transnet’s 12-day rail maintenance in South Africa next month.

- BigMint’s PHCC index dropped by $3/t to $187/t CNF Paradip amid weak demand and lower met coke prices. Bids remained low, with a mill source suggesting the index should reflect $184/t CFR levels. Sellers are finding it tough to close deals even at $170/t FOB. Indian met coke prices dropped INR 500/t to INR 29,000/t ex-Jajpur, while Australian PHCC prices slipped to $176/t FOB. Market sentiment stayed subdued.

- Met coke prices in India fell further this week due to weak steel demand and uncertainty over the continuation of quantitative restrictions (QRs) on imports. Blast furnace-grade coke dropped INR 500/t to INR 29,000/t ex-Jajpur, while Gandhidham saw a decline of INR 350/t to INR 29,150/t. Clarity on QRs is awaited following recent discussions, as current restrictions are set to end in June.

- Globally, China’s met coke market remains under pressure due to the steel off-season and expectations of another round of price cuts. Meanwhile, Australian PHCC prices slipped $6/t to $175/t FOB.

Ferrous scrap

- India’s imported ferrous scrap market remained largely stable over the week, with UK-origin shredded scrap assessed at $362/t CFR Nhava Sheva, slightly up from $361/t last week. Overall sentiment stayed cautious amid weak end-user steel demand, seasonal slowdown, and a persistent bid-offer mismatch.

- Indicative offers for HMS 80:20 were heard in the $338-345/t CFR range, while buyers quoted lower, around $335-340/t. Shredded scrap from the UK and Europe hovered at $360-362/t CFR, with limited firm offers from the US, reflecting market hesitancy.

- Total imported scrap volumes into India last week were at around 4,000-5,000 t, including HMS 1, HMS 80:20, busheling, bundle scrap, and PNS.

- Mills are expected to remain cautious unless either scrap prices soften or finished steel demand shows clear signs of improvement.

Ferro alloys

- Silico manganese: Indian silico manganese prices (60-14) rose by INR 600/t ($7/t) w-o-w to INR 71,300-72,100/t ($823-833/t) in the key regions of Durgapur, Raipur and Vizag. Smelters started tackling the supply surplus by strategically cutting production, leading to a price recovery in select regions.

- Ferro manganese: Indian ferro manganese (HC 70%) prices witnessed a downward trend, dropping by INR 700/t ($8/t) w-o-w to INR 71,600/t ($827/t) exw in Durgapur. Meanwhile, prices, exw-Raipur, also decreased to INR 71,900/t ($830/t). Prices declined due to weakening export demand, as overseas buyers reduced inquiries amid sluggish global steel market activity.

- Ferro silicon: Indian ferro silicon prices dropped by INR 1,600/t ($18/t) w-o-w, settling at INR 88,800/t ($1,026/t) ex-works Guwahati. Bhutanese prices also decreased by INR 2,500/t ($29/t) to INR 88,400/t ($1,021/t) ex-works. Prices dropped to their lowest levels since September 2024, weighed down by weak demand, as end-users increasingly opted for imported silicon metal over ferro silicon, curbing domestic buying interest.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices were largely stable, inching down by INR 400/t ($5/t) w-o-w, reaching INR 100,400/t ($1,160/t) ex-works Jajpur. The stability may result from regular trading activity combined with the moderate response observed in the Odisha Mining Corporation (OMC) auction. OMC’s chrome ore auction saw subdued interest, with 50,500 t sold out of 76,000 t, bids for Cr2O3 >48% grades dropped by 21–32% m-o-m.

- Additionally, OMC will conduct another e-auction on 25 Jun’25 for 6,900 t of ferro chrome across various grades and sizes (Cr: 50-64%, 0-100 mm).

Semi-finished steel

- Indian semi-finished steel prices trended lower this week. Domestic billet prices in all key locations decreased by INR 200-1,100/t. Sponge iron prices also showed fluctuating trends, moving down by INR 50-300/t. A decrease of INR 300/t was seen in Raipur.

- Indian DRI (Direct Reduced Iron) export offers decreased by $5 for CPT Raxaul to $315/t while, CPT Benapole offers decreased by $5 and stands at $325/t.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, conducted a steel-grade pig iron auction for 16,000 t on 16 June of which 12,000 t was booked at an average price of INR 30,200/t (by rake). However, management approval is still pending. In the previous approved auction, held on 10 June for 15,000 t, only 5,200 t was booked at an average price of INR 31,500/t (by road).

Finished longs

If-route: India s induction furnace-route rebar prices remained under pressure this week, with further declines observed across key markets. Purchasing activity was largely limited to immediate requirements, as a significant bid-offer gap compelled manufacturers to reduce trade prices. Retailers refrained from bulk bookings due to prevailing market uncertainty and heavy rainfall in several regions, which dampened demand further.

- As a result, mills are facing increased sales pressure and rising inventories, currently estimated at 12–14 days. While prices have approached their lower threshold in most regions, they are expected to stay subdued in the absence of any clear signs of demand recovery.

- On a weekly basis, rebar prices declined in the range of INR 200-1,200/t across regions, as per BigMint assessment.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 40,800-41,200/t exw Raipur and INR 43,200-43,800/t exw Jalna.

- Trade reference prices of heavy structural steel for base size 150mm channel stood at INR 42,400-42,800/t exw Raipur.

- Trade reference prices of wire rods were assessed at INR 41,400-41,800/t ex Raipur.

Bf-route: Trade-level BF rebar prices declined across major Indian markets this week, driven by weak demand and cautious market sentiment. Buyers adopted a wait-and-watch approach due to the prevailing disparity between bids and offers, while distributors focused on liquidating high-cost inventories.

- Trade-level BF rebar prices declined by INR 1,300/t w-o-w to INR 51,900/t exy-Mumbai, as per BigMint’s assessment on 20 June. Prices are exclusive of GST at 18%.

- In the projects segment, prices declined further to INR 51,000-51,500/t FOR Mumbai, weighed down by continued bid-offer disparity and subdued construction activity due to the ongoing monsoon season.

Finished flats

- Trade-level prices of hot-rolled coils (HRCs) declined by up to INR 500/t w-o-w to INR 50,900-52,900/t ($596-616/t) across markets. Cold-rolled coil (CRC) prices remained rangebound w-o-w, assessed at INR 57,000-60,900/t ($659-718/t).

- Distributors experienced weaker demand, with a decline in enquiries and even slower conversion to actual sales. Purchases were limited and need-based, often in smaller quantities. As the quarter-end approaches, there is increased pressure to clear inventory and manage capital rotation efficiently.

- India’s bulk imports of HRCs and plates touched 1.11 mnt as of 16 June, based on vessel line-up data. Around 106,060 t of additional cargo areexpected by month end.

- BigMint’s India HRC (S275) export index fell by $15/t to $555/t FOB East India, as EU demand remained weak due to sluggish automotive and construction activity. Trade slowed further ahead of the Corpus Christi holidays. Indian mills also held back HRC offers to the Middle East amid stiff competition from China.

Leave a Reply