- Exporters cautious amid geo-political tensions

- Chinese demand weak amid ongoing rainy season

The seaborne iron ore export market remained largely range-bound this week, reflecting a slowdown in trading activity and subdued buyer sentiment. Exporters adopted a cautious approach due to ongoing geo-political tensions and unfavourable price trends, which have dented the momentum in overseas sales.

Meanwhile, a few exporters concluded their cargo deals in this publishing window amid expectation of prices dropping in the near term due to the geo-political tensions.

Prices, deals

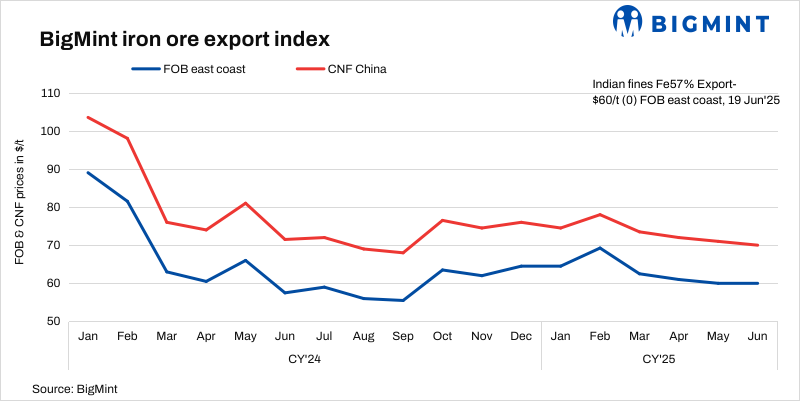

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index remained stable w-o-w at $60/t FOB east coast on 19 June.

Deals of around 165,000 t of Fe 56-57% fines were concluded at $70-71/t CFR China in this publishing window, while a deal for 80,000 t of below Fe 55% fines was concluded on the eastern coast but is yet to be confirmed from the transected parties.

Market commentary

Market participants said that the overall traded volume remained lower this week, with most exporters preferring to observe the situation before striking new deals. An exporter commented: “Export prices are currently not viable. With domestic procurement costs staying high, selling in the export market offers little to no margin.”

Chinese steel mills, typically the primary buyers, were seen actively booking medium-grade iron ore fines. However, overall demand from China remained limited due to the ongoing rainy season in certain regions, which is impacting construction activity and logistics.

The discount on 57% Fe iron ore fines remained stable at 18-19% this week, mirroring last week’s levels. Some deals of lower-grade ore were heard in the market, although prices were not disclosed.

Another seller informed, “With the market expecting a price drop, most buyers are in wait-and-watch mode. Geo-political uncertainties further dampened the market mood.”

Exporters are currently focused on completing shipments of previously concluded contracts, with few fresh bookings happening. The market awaits a clearer direction as both buyers and sellers remain on the sidelines, gauging short-term price cues.

Chinese spot prices fall w-o-w: Benchmark iron ore fines in China dropped by $3/t w-o-w to $93/t CFR on 18 June. The prices were influenced by oversupply concerns resurfacing amid tepid buying interest. The physical iron ore market has weakened recently due to lower demand and the rainy season in China. As per reports, weak steel margins and declining port-stock prices signalled poor fundamentals, prompting traders to offload cargoes even at a loss.

DCE iron ore futures down w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the September 2025 contract inched down by RMB 6/t ($1/t) w-o-w to RMB 698/t ($97/t) on 19 June. Meanwhile, prices remained stable on a d-o-d basis.

Rationale

- Three (3) deals for Fe 57% were recorded during this publishing window, and all were considered for price calculation. Therefore, T1 trade was given 50% weightage in the index calculation. For the detailed methodology, click here.

- BigMint received seventeen (17) indicative prices in the current publishing window, and twelve (12) were considered for price calculation as T2 inputs and given 50% weightage.

Iron ore inventory at Chinese ports increased by 1.2 mnt (million tonnes) w-o-w to 134.6 mnt on 19 June, as per data published by SteelHome.

Outlook

As per BigMint’s analysis, iron ore export prices are expected to remain uncertain in the coming days amid the weak market sentiments and rainy season in both India and China. Some deals which are under negotiation may conclude next week.

Leave a Reply