- Production expands 70% from FY’21, outpaces demand

- Exports plunge 52% in 4 years to 0.5 mnt in FY’25

- Weakness in finished steel tags percolates upstream

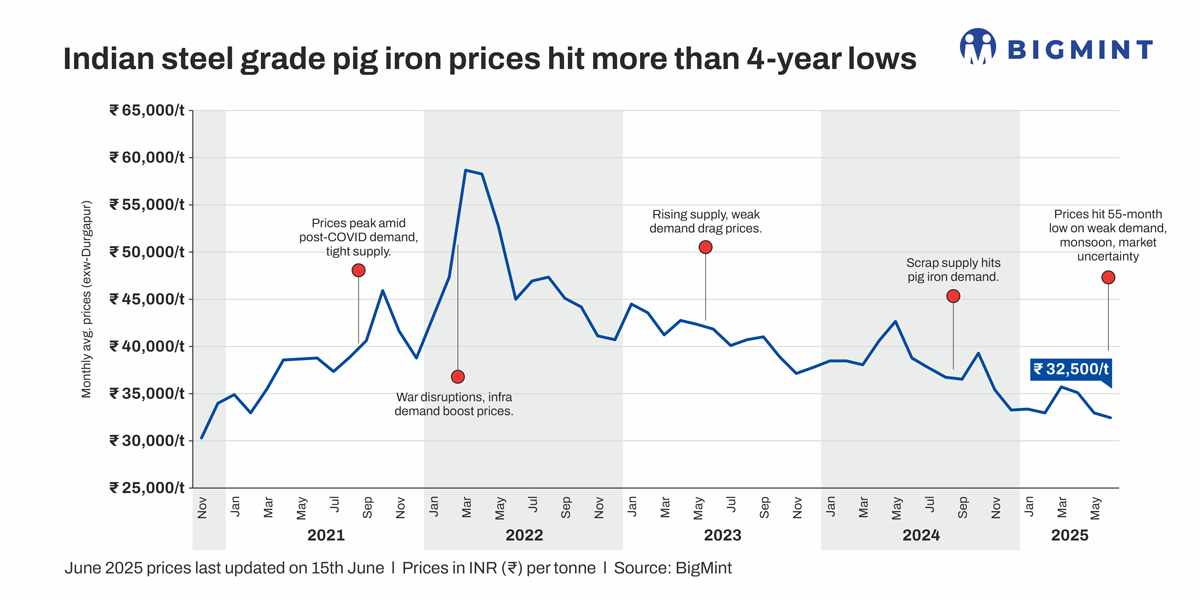

Morning Brief: India’s steel-grade pig iron prices sank to a four-year low in Durgapur in May 2025. Price tags plunged INR 2,200/t m-o-m to a monthly average of INR 32,900/tonne (t) exw-Durgapur, with similar values last recorded in February 2021 (INR 33,000/t) – just as the market was recovering from the COVID-19-led downturn.

In recent times, pig iron tags have faced mounting pressure from a number of quarters, foremost of which is the steady downtrend in the finished market. Due to this, while capacity expansions have accelerated, demand growth has been slack.

The resultant supply glut has also intensified competition among producers in major hubs such as Chhattisgarh, Jharkhand, Odisha, and West Bengal, significantly eroding their profit margins. Additionally, falling raw material prices have also left the market without cost support.

BigMint traces the reasons why Indian pig iron prices have experienced such a steep collapse.

Why have pig iron prices retreated to 4-year lows?

Supply swells amid surging production: India’s pig iron production expanded by 71% to 8.33 million tonnes (mnt) in FY’25 from 4.88 mnt in FY’21. While established players such as SAIL and JSPL continued to ramp up output, new entrants such as Rungta, Shyam Sel, NMDC Nagarnar, and Evonith have also injected significant volumes into the market. This has led to a supply glut, as demand growth has been relatively weaker.

Downstream price weakness adds pressure: Falling finished steel prices impacted pig iron tags.

To illustrate, BigMint’s India Rebar Index, a barometer of prevailing price trends, settled at 128.7 points on 13 June, quite close to February 2021’s monthly average of 122.5. This suggests that the finished steel segment has also faced sustained price pressure. Previously, the rebar index hit these levels in December 2024-February 2025, July-September 2024, and then back in December 2020-March 2021.

Export prospects dry up, imports rise: Pig iron exports, which used to offer relief during times of weak domestic demand, fell by a sharp 52% to 0.5 mnt in FY’25 from 1.06 mnt in FY’21. The plunge in international pig iron shipments mirrors the contraction in India’s steel exports, which has stemmed from China’s aggressive export push.

Meanwhile, imports climbed up in these four years, to 0.30 mnt in FY’25 from just 0.01 mnt in FY’21. Russia was the leading supplier in FY’25.

This mismatch limited external price support and channelled more material into an already saturated domestic market.

Price competitiveness of scrap rises: Domestic and imported scrap prices have also dropped steadily, and with increased collection volumes, many induction furnace (IF) and foundry operators have shifted away from pig iron. The more flexible scrap route, combined with easier availability, further challenges pig iron’s market share.

The monthly price spread between HMS (80:20), DAP Durgapur, and pig iron, exw-Durgapur, reveals a sharp narrowing in recent times. In Q4FY’21, the spread hovered at around INR 3,700/t, but as the years progressed, this differential shrank drastically, averaging below INR 800/t in Q4FY’25 and even contracting to 0 in May.

The shrinking spread reflects the climbing price competitiveness of scrap. This has prompted IF units to increasingly substitute pig iron with scrap, as part of a structural shift in raw material preferences within the secondary steel sector.

Also pointing to the steady substitution of pig iron with scrap is the shift in India’s metallic mix over FY’21-25. While crude steel production climbed up by 46%, hot metal consumption increased at a slower 32%. DRI usage rose 65%, while that of scrap moved up by 60%.

Input costs decline, fail to offer support: Raw material prices have also corrected over the last four years, failing to shore up pig iron tags. For example, met coke (25-90 mm BF-grade), ex-Jajpur, hit a five-year low in early June. In May, monthly average prices were at INR 32,300/t, down precipitously from the high INR 45,000/t average recorded over September 2021-March 2023.

Likewise, Odisha iron ore lump prices stood at INR 6,760/t in May against elevated levels of INR 10,400/t (average) in FY’22.

Auctions signal demand softness: Pig iron auctions, which shape prices and demand trends, have increasingly witnessed low turnout and offtake in its recent times. For example, in 2024, across NMDC’s 22 auctions, the offered volumes were an average 28,000 t, while offtake was at around 19,000 t (68% sold). In 15 auctions in January-May 2025, offered quantities were lower at 12,000 t on average, of which around 5,000 t (42%) were booked.

Prices have also trended down, with NMDC’s latest three auctions in May closing at INR 32,700/t compared to approximately INR 36,000/t in 10 auctions in August-December 2023. These subdued market dynamics are also evident from SAIL’s various auctions.

This downtrend pressured other private producers to align their offers accordingly to stay competitive.

Outlook

A near-term price recovery in pig iron seems a remote possibility at this juncture. Pig iron prices have dropped INR 500/t from May’s average to INR 32,400/t in June, indicating that the downtrend is likely to continue.

The onset of the monsoon has slowed down construction activity, and given that no major boost is expected in steel demand, pig iron prices are likely to remain under pressure. Met coke prices are also hurtling down.

Until exports revive or infrastructure-led steel demand returns meaningfully, pig iron producers may continue facing squeezed margins. Cost-efficient operations and diversified customer base will remain key survival strategies amid this prolonged downcycle.

Leave a Reply