- Declining pig iron prices curtail met coke demand

- 4th coke price cut buzz pressures Chinese market

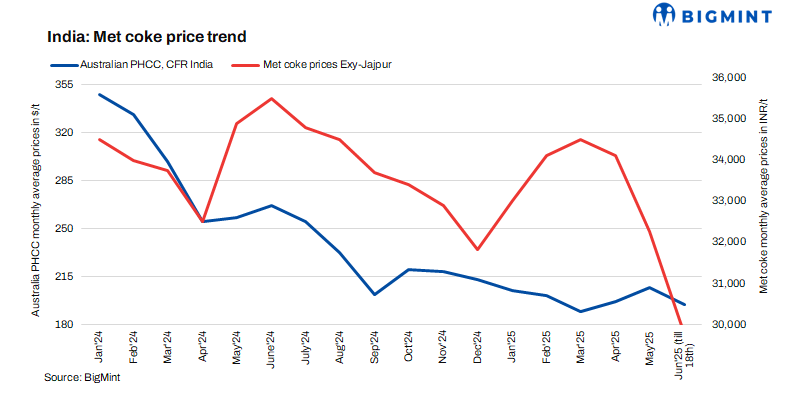

Indian metallurgical (met) coke prices fell further this week, with the 25-90 mm blast furnace (BF) grade down by INR 500/tonne (t) to INR 29,000/t ex-Jajpur, according to BigMint’s assessments on 18 June. Prices hit a five-year low last week, as per BigMint’s records.

Likewise, in Gandhidham, western India, prices decreased by INR 350/t w-o-w to INR 29,150/t exw. These declines are attributed to weak demand in the steel sector and ongoing uncertainties regarding quantitative restrictions (QR).

“There was a meeting regarding the future course of action for QRs in met coke imports yesterday. The market is waiting for a final word on the QR. Notably, in December 2024, when the Indian government announced the QRs, they were announced for two quarters of 2025, i.e. January-March and April-June, with the total volume pegged at 713,583 t in each quarter,” stated a domestic coke producer in India.

Factors weighing on Indian met coke prices

Declining pig iron prices in India lead to reduced coke procurement: NMDC’s steel plant in Nagarnar, Chhattisgarh, conducted a steel-grade pig iron auction for 16,000 t on 16 June 2025, of which 12,000 t were booked at an average price of INR 30,200/t (by rake). However, management approval is still pending. In the previous approved auction, held on 10 June 2025 for 15,000 t, only 5,200 t were booked at an average price of INR 31,500/t (by road).

China’s coke market slows as steel demand slumps due to summer: With the summer steel off-season underway, China’s metallurgical coke market faced subdued demand, weighed down by persistent inventory pressures and weak cost support. Speculation around a potential fourth round of Chinese met coke price cuts added further pressure on prices.

Steelmakers, battling thin margins and poor market confidence, limited coke intake and production. Despite recent coking coal price stabilisation, expectations of further coke price cuts persisted amid weak steel demand and oversupply.

Australian premium hard coking coal (PHCC) prices fell $6/t w-o-w to $175/t FOB. Market sentiment remained mixed, with wider price expectations for premium low- and mid-vol coals.

Outlook

Met coke prices are expected to remain under pressure amid a falling steel market and the seasonal slowdown because of the monsoon. The lack of clarity on QRs may exert additional pressure on prices.

Leave a Reply