- South Asia seasonal slowdowns impacts cargo volumes

- Baltic Capesize Index (BCI) surges by sharp 880 points

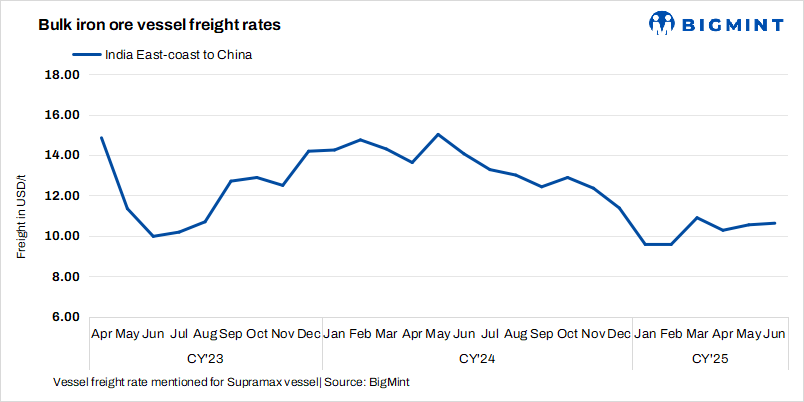

Dry bulk iron ore freight rates from the Indian Ocean to China fell w-o-w amid muted demand and limited fresh cargo activity while the other routes perked up somewhat. As evident from recent reports, despite some firmness in the Atlantic and US Gulf regions, the Indian Ocean route has not seen much new business. Monsoon disruptions and seasonal slowdowns in South Asia, especially India, have led to a decline in cargo volumes such as coal and iron ore being shipped out. With fewer cargoes available, vessel owners are facing increased competition for limited fixtures, which is putting downward pressure on freight rates.

Additionally, there is a growing tonnage oversupply in the region, as vessels continue to open without corresponding cargo demand. Charterers are therefore able to negotiate lower rates due to the surplus of available ships. The situation is exacerbated by slow economic activity and cautious sentiment from buyers in China, which affects demand for inbound raw materials. As a result, despite some isolated fixtures being reported, the overall market remains soft with freight rates declining on Indian Ocean-China routes.

“We observed a slight firming up in bunker prices last Friday due to the ongoing Iran-Israel conflict. The full market reaction should become clearer this week. I feel there is a chance of rates for the Indo-WCI route to firm up, with some owners likely to seek a premium for moving into the WCI-PG range, at least until there’s better clarity on the intensity and expected duration of the conflict,” a source from a shipping company said.

In contrast, Capesize freight rates have risen, largely driven by firm offer levels for late June cargoes from Western Australia to China. Offer levels for late June cargoes are staying firm, especially on the key Western Australia to China route. Mining giants like FMG and Rio Tinto were active in seeking tonnage, which kept interest alive in the Pacific market. Even though overall trade activity was limited during Asian hours, the few available cargoes attracted higher indicative rates for early July shipments. This suggests that shipowners are holding out for better prices, expecting stronger demand as June ends.

Another contributor to rising freight levels is the recent increase in bunker fuel prices, influenced by geopolitical tensions in the Middle East. This is inflating vessel operating costs, prompting some charterers with urgent needs to pay premiums for quicker bookings.

Factors influencing freights

- Baltic indices increase w-o-w: The Baltic indices, indicating trends in vessel demand, rose w-o-w. The Baltic Dry Index (BDI) was recorded at 1,968 on 16 June, increasing by 335 points w-o-w. Additionally, the Baltic Capesize Index (BCI) stood at 3,722, sharply up by 880 points w-o-w. Meanwhile, the BSI inched up by 3 points w-o-w to 936.

- China’s iron ore spot prices fall w-o-w: Chinese spot prices of iron ore fines (Fe62%) were assessed at $93/t CFR on 17 June, down by $2/t w-o-w. Prices have fallen to their lowest level due to weak fundamentals and increased trading in medium-grade fines. Sluggish conditions in the Chinese real estate sector, disappointing crude steel data, and high iron ore supply put downward pressure on prices. The off-peak season and the ongoing Israel-Iran conflict have further weakened market sentiment.

Route-wise updates

- India-China: Freights from the Indian Ocean to China were recorded at $10.3/t, edging down by $0.3/t w-o-w. According to market sources, a Supramax vessel was recently fixed at approximately $10.30/t from New Mangalore to China for the shipment period of mid-July, while several other fixtures were heard at levels of $8.98/t from Gopalpur to China for the mid-July shipments.

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $10.9/t on 18 June, increasing by $1/t w-o-w. According to sources, major Australian miners Rio Tinto, BHP and FMG booked Capesize vessels from a Western Australian port to Qingdao at around $9.45-11/t. Shipment is scheduled for 26 June-1 July.

- Brazil-China: Freights for Capesize vessels from Brazil to China rose this week. Rates from Tubarao to Qingdao Port were assessed at $25.8/t on 18 June, jumping by $2.4/t w-o-w. As per sources, two Capesize vessel got booked from Tubarao to Qingdao at $24-26/t for the shipment period of 30 June-11 July.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao increased by $2.1/t w-o-w to $19.5/t on 18. It is heard that one Capesize vessel got booked from South Africa to China at $19.45/t for the shipment period of late June.

Leave a Reply