- Buyers eye silicon metal for higher Si content

- Stainless steel demand also remains subdued

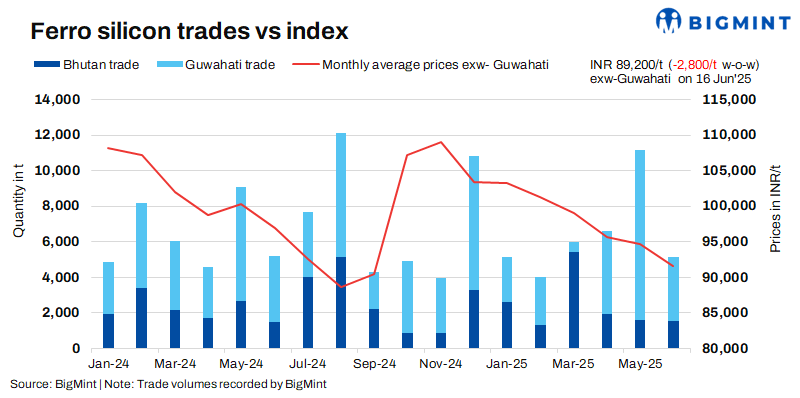

Indian ferro silicon (70%) prices dropped by INR 2,800/tonne (t) ($33/t) as compared to the previous assessment on 9 June. Prices reached their lowest point since September 2024, dragged down by subdued demand. End-users preferred imported silicon metal in place of ferro silicon, limiting domestic inquiries.

Ferro silicon prices in India were at INR 89,200/t ($1,036/t) exw-Guwahati, as per BigMint’s assessment on 16 June. In Bhutan as well, prices dropped by INR 1,600/t ($19/t) w-o-w to INR 90,400/t ($1,050/t) exw. Deals for approximately 3,400 t were concluded last week in both regions within the price bracket of INR 88,000-91,000/t ($1,022-1,057/t) exw.

Market highlights (10-16 June 2025)

Silicon metal imports curb ferro silicon demand: In recent weeks, there has been a surge in silicon metal imports to India, primarily from China. Commenting on this, an Indian stainless steel manufacturer stated, “We are currently using silicon metal as a substitute for ferro silicon. Its prices are currently at around INR 114,000-115,000/t ($1,324-1,336/t).” Zero import duty and higher silicon content (Si: 98-99%) also lifted demand for silicon metal.

South India’s price trends: Due to a drop in prices in Bhutan and northeast India, sellers in the south also adjusted their offers to INR 92,000-94,000/t ($1,068-1,092/t) exw.

Stainless steel demand remains soft: Meanwhile, some sources were of the opinion that silicon metal could not completely replace ferro silicon and cited weak demand for stainless steel as the key reason for drop in prices. They said that it was for this reason that Bhutan’s official prices for the month, which were at INR 92,000/t ($1,068/t), could not be sustained for a longer duration.

Chinese prices edge down: Ferro silicon (Si:75%) prices in China dipped by RMB 100/t ($14/t) w-o-w to RMB 5,490/t ($765/t) exw-Inner Mongolia. Production cuts in Inner Mongolia and Qinghai led to lower weekly output, but warehouse inventories remained high, creating a situation of reduced supply without destocking. Demand was weak due to the off-season, and downstream buying interest was low.

Looking ahead, prices may stay low and range-bound, pressured by weak steel demand and supported by production costs. A price rebound could occur if electricity costs rise or steel mills unexpectedly restock. Overall, price movements will depend on cost factors and broader market trends.

On the Zhengzhou Commodity Exchange (ZCE), prices edged up by RMB 118/t ($16/t) w-o-w to RMB 5,292/t ($737/t) on 16 June for September deliveries.

Outlook

Considering the current market scenario, a further correction in prices is likely in the days ahead.

Leave a Reply