- Indian buyers cautious, prefer cheaper alternatives

- Pakistan removes 2% ACD to revive scrap trade

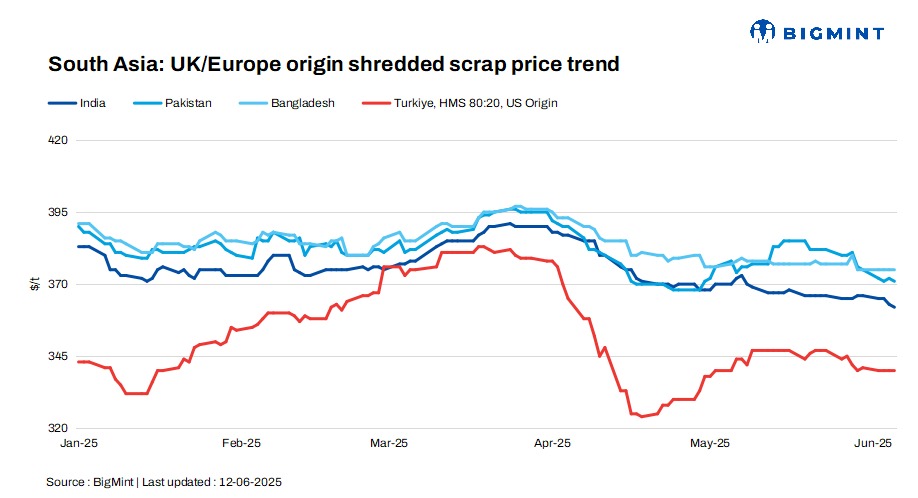

South Asia’s imported scrap market witnessed a quiet week, with activity slowing across India, Pakistan, and Bangladesh due to a mix of holidays, weak steel demand, and seasonal factors. Indian buyers remained sidelined amid monsoon disruptions and a shift toward cheaper sponge iron. In Pakistan and Bangladesh, Eid holidays, financial constraints, and LC issues kept mills inactive, with only limited spot bookings heard. Even as some regions saw offers holding steady, a clear buyer-seller mismatch prevented meaningful trade. The region now looks ahead to post-Eid resumption and potential policy cues to revive buying momentum.

Market overview

India: India’s imported scrap market remained muted amid weak steel demand and the early onset of the monsoon, which dampened buying interest. Containerised shredded scrap was heard at $360–365/t CFR Nhava Sheva, while HMS 80:20 was offered at $340-345/t CFR, with bids trailing lower at $335-340/t. West African HMS, depending on loading configurations, was quoted at $345–350/t CFR. However, limited trades were reported due to a persistent gap between buyer and seller expectations.

Mills continued to favour cheaper alternatives like sponge iron. With demand from infrastructure and auto sectors slowing, buyers remained cautious and awaited clearer cues before resuming active restocking.

Pakistan: Pakistan’s imported scrap market remained quiet amid Eid holidays, with most mills holding back on fresh purchases.

Containerised shredded offers were heard at $370-375/t CFR Port Qasim, though only a few deals materialised near $370/t levels.

On the domestic front, scrap traded at PKR 136,000-140,000/t ($482-496/t) and rebar at around PKR 235,000/t ($833/t), indicating weak demand and cautious buyer sentiment.

Market attention is now on the upcoming budget, which has scrapped the 2% Additional Customs Duty on scrap and shipbreaking. Activity is expected to pick up gradually once Eid-related slowdowns subside and policy clarity emerges.

Bangladesh: Bangladesh’s imported scrap market remained largely inactive due to Eid holidays and weak buying interest from mills facing financial stress and LC issues. Shredded offers were last heard at $375-378/t CFR Chattogram, while HMS 80:20 ranged between $355-360/t CFR. While a major mill booked Japanese Kanto cargo at $345-350/t CFR, most buyers stayed cautious amid limited liquidity.

No significant containerised deals were reported. The ship recycling sector also slowed, with only 9 HKC-compliant yards operational. Despite the quiet market, sentiment remains cautiously optimistic, with expectations of increased restocking activity once Eid holidays end and monsoon conditions begin to ease.

Turkiye: The Turkish imported scrap market remained stable with US bulk HMS 80:20 offers assessed at $340/t CFR. Despite sellers’ belief that mills still need July-shipment cargoes, buyers stayed cautious due to weak domestic rebar demand, with rebar prices flat at $545/t FOB. US recyclers avoided making firm offers, unwilling to lower July-August shipment prices amid shipping shortages.

EU sellers were similarly firm, supported by a strengthening euro and high scrap collection costs. With buyers unwilling to pay more than current levels, and sellers holding their ground, the market stayed in a standoff, awaiting clarity on near-term steel demand and shipping dynamics.

Price assessments

India: UK-origin shredded indicatives were assessed at $362/t CFR Nhava Sheva, down by $2/t d-o-d.

Pakistan: UK-origin shredded indicatives stood at $371/t CFR Qasim, down by $1/t d-o-d.

Bangladesh: UK-origin shredded prices were assessed stable d-o-d at $375/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $340/t CFR Turkiye, unchanged d-o-d.

Leave a Reply