- Rebar output exceeds sales, inventories pile up

- Rains, tight liquidity impact finished demand

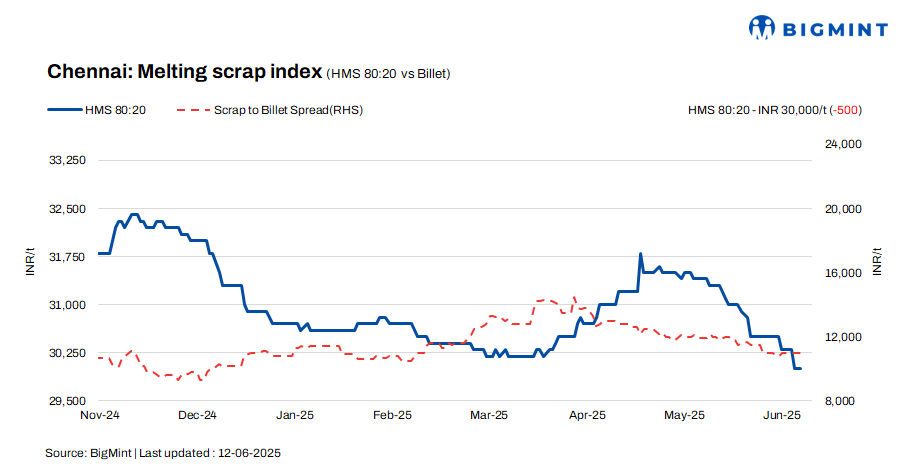

Prices of HMS (80:20) in Chennai, India, fell by INR 500/tonne (t) w-o-w to INR 30,000/t, although, d-o-d, prices remained stable, as per BigMint’s latest assessment. Billet prices also saw a decline of INR 300/t w-o-w to INR 41,000/t, while no significant changes were observed on a d-o-d basis.

Additionally, rebar prices remained unchanged d-o-d at INR 46,500/t but saw a w-o-w drop of INR 500/t. Overall, the market shows a lack of significant momentum, with selective price corrections across key semi-finished and long products.

Imported, domestic price trends

A scrap trader stated that offers for shredded from Australia stood at $365-370/t CFR Chennai, though buyers aimed to secure material at a maximum price of $360/t. Meanwhile, offers for HMS 80:20 were slightly lower, at $350-355/t. In recent months, around 4-5 vessels, containing approximately 75,000-80,000 t of scrap, have been beached in Chennai.

In Chennai, domestic HMS (80:20) prices were in the range of INR 29,500-30,000/t for spot transactions with immediate payment. For deals involving extended credit terms, prices were slightly higher, at INR 30,000-30,500/t. This reflects the prevailing liquidity preferences and the price differential between spot and credit-based transactions.

Additionally, most offers and concluded trades in the domestic market were within the INR 29,500-30,500/t range.

Buyer-supplier sentiments

Rebar manufacturers in Chennai operated at approximately 70-80% capacity, but daily sales accounted for only around 50% of their production, resulting in a steady accumulation of inventory. There are also reports that the Tamil Nadu government is considering issuing a government order (GO) to standardise rebar grades, which is expected to enhance consistency across manufacturers, improve quality control, and possibly affect both production processes and costs.

Meanwhile, demand for finished steel was weak over the past few weeks, primarily due to seasonal rains. Additionally, poor payment flows from government agencies hampered contractor liquidity, affecting their ability to place new orders.

According to a scrap supplier, HMS 80:20 was traded between INR 29,500-30,500/t, with pricing influenced by payment terms. The market for both semi-finished and finished steel witnessed a decline in demand, putting mills under pressure to reduce scrap purchase prices. Notably, manufacturers were utilising an 80:20 scrap-to-sponge iron ratio, indicating a heavy reliance on scrap as their primary raw material input.

Regional comparison

In the Jalna market of Western India, billet prices remained stable on a day-on-day (d-o-d) basis, with current prices assessed at INR 40,200/t. While rebar and HMS 80:20 prices fell by INR 100/t to INR 45,200/t and INR 31,600/t, respectively. The market continued to experience weak demand for finished steel, as seen in recent months. According to sources, mills currently hold inventory levels of around 12-15 days. To control conversion costs, mills are incorporating 30-50% sponge in their charge mix.

Outlook

Given the weak demand, rising inventories, and limited market liquidity, rebar prices are expected to stay bearish in the near term. Meanwhile, HMS prices are expected to remain within a narrow range, with fluctuations likely to be limited to INR +/- 500/t. The short-term price direction will largely hinge on evolving market conditions, including demand trends, mill procurement behaviour, and the availability of incoming scrap supply.

Leave a Reply