- Chrome ore costs support prices despite weak demand

- Vedanta FACOR schedules auction for 13 Jun’25

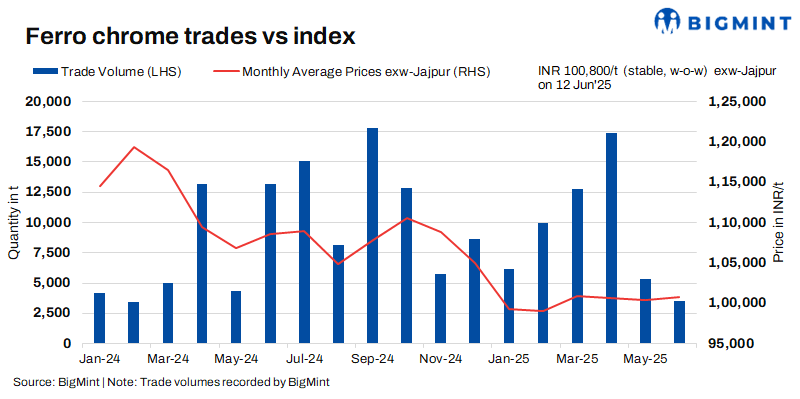

Indian high-carbon ferro chrome (HC60%, Si:4%) prices remained stable w-o-w compared to the previous assessment on 4 June 2025, as muted stainless steel demand continued to weigh on market activity.

High-carbon ferro chrome (HC60%, Si:4%) prices in India were INR 100,800/t ($1,178/t) exw-Jajpur, as per BigMint’s assessment on 11 June. Around 1,200 t of trades were reported last week within the range INR 100,000-102,000/t ($1,168-1,192/t) exw.

For low-silicon high-carbon ferro chrome, prices inched down by INR 800/t ($9/t) w-o-w to INR 105,000/t ($1,227/t) exw-Jajpur. However, tags remained stable w-o-w for low-carbon (C:0.1%) ferro chrome at INR 202,000/t ($2,360/t) exw-Durgapur.

Market recap (5 – 11 June)

Cautions buying amid weak demand: Prices held firm, with the market remaining stagnant as buyer resistance and sluggish demand from the stainless steel sector restricted upward price movement. Meanwhile, elevated chrome ore prices provided cost support, preventing any significant decline and helping maintain overall price stability.

However, further clarity on market direction is expected after the Vedanta FACOR auction scheduled for tomorrow. In the previous auction on 21 May, the 10–150 mm lot recorded an H1 price of INR 100,300/t exw.

A seller informed BigMint, “The 300 series stainless steel market is very poor and may drag ferro chrome prices down.”

China market scenario: Ferro chrome (HC60%) prices in China remained steady w-o-w at RMB 7,950/t ($1,105/t) exw-Inner Mongolia.

On the supply side, production has resumed in the northern regions after maintenance breaks, enhancing market circulation. However, downstream stainless steel mills stayed cautious, extended their raw material inventory cycles, and tightened cost controls, which limited their acceptance of higher prices.

Environmental inspections continued to curb outdated production capacity, while the lack of new regulations left the market without a clear direction. Chrome ore prices held steady, although some traders offered discounts on South African material. Falling coke prices slightly reduced smelting costs.

According to market sources, Merafe/Glencore has shut down one of its furnace due to expansion of ferro chrome capacity in China. Continued operations may have strained margins, making the smelter unviable. An official notice from the company is still awaited.

Sluggish demand from stainless steel sector: Stainless steel prices for 304 grade HRC were unchanged w-o-w at INR 182,000/t ($2,126/t) exw-Mumbai.

Domestic demand for finished stainless steel longs remains subdued, with major mills operating at 60-70% capacity. Continued weakness may lead to further production cuts, while underperforming export markets offer little support.

The slowdown in infrastructure and government projects is adding to the challenge. With activity expected to remain slow through the monsoon season, the stainless steel market is likely to stay muted in the near term.

Outlook

Prices are likely to fluctuate in the near term amid weak demand from the stainless steel sector, with further clarity likely to emerge after FACOR’s auction tomorrow.

Leave a Reply