- Prices in western India hit five-month low

- Lack of clarity on QRs adds to bearishness

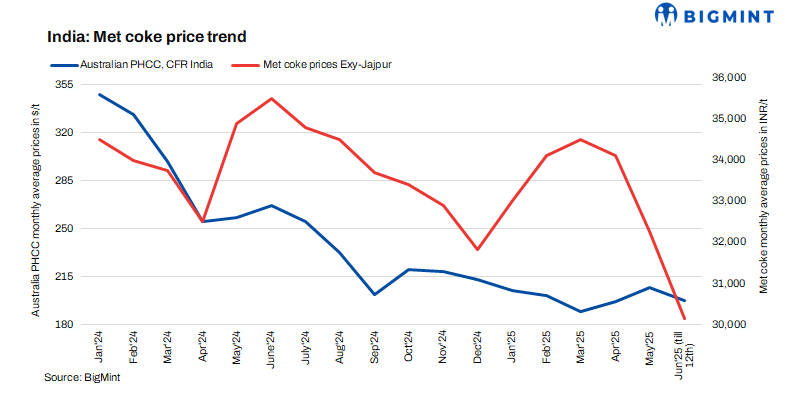

Indian metallurgical (met) coke prices plunged this week, with the 25-90 mm blast furnace (BF) grade down by INR 1,300/tonne (t) to INR 29,500/t ex-Jajpur, according to BigMint’s assessments on 12 June. This marks a five-year low in eastern India, last seen in August 2021.

Likewise, in Gandhidham, western India, prices decreased by INR 1,100/t w-o-w to INR 29,500/t exw, the lowest since January 2025. These declines are attributed to weak demand in the steel sector and ongoing uncertainties regarding quota restrictions.

Declining steel prices lead to reduced coke procurement

Falling steel prices led steelmakers to reduce coke procurement, with inquiries and transactions dropping. Buyers were hesitant due to uncertainty over future steel production and sales, opting to hold off on restocking until clearer demand signals emerge.

The uncertainty in the steel sector is reflected in NMDC’s recent pig iron auction in Nagarnar, where only 5,200 t out of the 15,000 t offered were booked at INR 31,500/t, down INR 1,100/t from the bids of INR 32,600/t recorded in the previous auction on 22 May.

This decline in demand signals caution in both the steel and pig iron markets, with buyers waiting for further price adjustments. Durgapur and Raipur pig iron prices have dropped by around INR 2,700-2,800/t since April.

Regulatory concerns add to market pressure

Regulatory uncertainties also fuelled the bearish sentiment in the met coke market. The potential extension of the quantitative restrictions (QRs) on imports, along with an ongoing anti-dumping investigation, has created caution among importers. Without confirmation on the QR’s full-year extension, concerns over supply disruptions and price instability added to market hesitancy.

China sees 3rd straight round of met coke price cuts

China’s met coke market is facing similar challenges, with prices cut by RMB 150-185/t since mid-May due to weak steel demand and high inventories. Steel mills in Hebei and Tianjin reduced purchase values by RMB 50-75/t, the third consecutive round of met coke price cuts, driven by high inventories with mills and an expected fall in steel demand. While there was a brief uptick in coke and steel futures on 4 June, the overall market remains weak, and these gains may not sustain due to poor fundamentals.

Outlook

Met coke prices are expected to remain under pressure amid a falling steel market and the seasonal slowdown because of the monsoon. The lack of clarity on quota restrictions may exert additional pressure on prices.

Leave a Reply