- Primary mills cut rebar prices for June sales

- HRC prices stable, mills keep tags unchanged for June

- Possible US-India interim trade deal to boost steel market

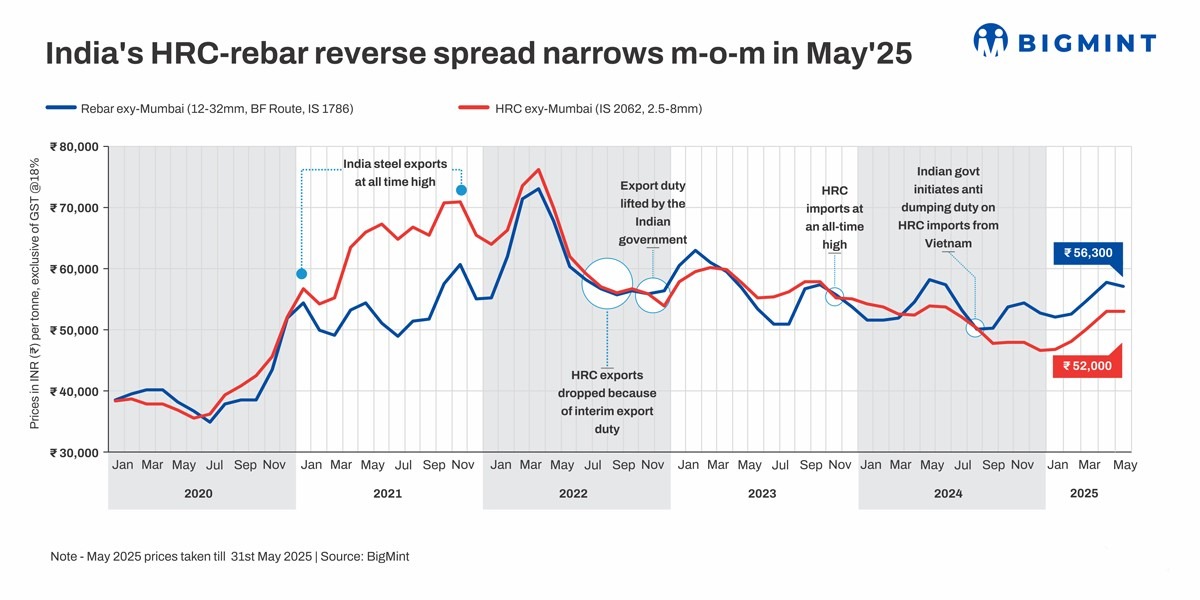

Morning Brief: In the domestic steel market, the hot-rolled coil (HRC) and blast furnace reinforcement steel bar, or rebar, reverse spread narrowed somewhat in May 2025. As per BigMint data, the reverse spread narrowed by INR 800/tonne (t) in May compared with April.

Usually, HRC is sold at a premium of INR 4,000-5,000/t ($47-59/t) over blast furnace (BF) route rebar. However, the reverse trend continued for the ninth consecutive month in May and, barring a brief month’s pause in August 2024, has been continuing for around 14 months.

This indicates that domestic flat steel prices have been under pressure for well over a year now.

Steel price movements in May

Primary mills cut rebar list prices: Indian Tier-1 mills reduced their list prices of rebar by up to INR 1,500/t ($17/t) for early-June deliveries as against prices prevailing in end-May. Post-revision, list prices were at INR 54,500-55,500/t ($635-646/t) on landed basis. Mills had offered discounts/rebates to augment sales in May.

Rebar inventories at Tier-1 mills increased by approximately 10% m-o-m in early-June, sources informed, due to sluggish sales in May, as declining prices and soft demand posed challenges for mills in securing new orders.

Weakness in the IF steel market also affected BF-origin rebar prices. Induction furnace (IF)-route rebar prices fell 3% m-o-m in May, as buyers engaged in trades only for their urgent needs. Inquiries were limited, and manufacturers either kept list prices stable or offered discounts.

Inventory holding periods increased to above 12 days by the end of the month, with heavy rains and labour shortages hindering construction activity.

HRC prices stable amid soft demand: HRC prices remained stagnant m-o-m amid liquidity troubles and subdued demand affecting trade. The monthly average price of HRC (IS 2062, 2.5-8 mm) was assessed at INR 52,000/t in May.

Buyers delayed purchases, hoping for further price corrections. Labour shortages and the onset of monsoon weighed on prices, though supply shortages in early May and a decline in import arrivals due to the safeguard duty lent some support.

Mills did not provide any price support for May. “Distributors are trying to keep prices firm as mills have not offered any price breaks for May. But buyers are holding back, only purchasing what is essential to capitalise on falling prices and to avoid monsoon blues,” a market source told BigMint.

Imports of HRC and steel plates remained below 0.3 mnt in May, down from over 0.4 mnt in March, which provided some support to the domestic mills, especially in view of the high duty threshold level on HRC under the 12% provisional safeguard duty which came into force in mid-April.

However, HRC export prices have been under pressure due to global downtrend and competition from other countries. So, this has not offered any support to domestic prices, and export prospects keep deteriorating.

Outlook

The domestic steel market, largely dependent on the construction, infrastructure, housing, real estate sectors, is expected to remain under pressure in the short term as monsoon settles in in large parts of the country. This is a period of seasonal cyclical downturn that the steel market has to pass through.

But globally, steel market sentiments may recover significantly in the event of a US-China and US-India interim trade deal to lessen the harsh impact of tariffs on the market and trade relations. Going by press coverage of latest developments, such a deal looks increasingly likely.

If tariffs are cut sufficiently as part of any new deal, it will surely boost global steel prices and, of course, domestic HRC prices and steel prices in general. But there is a big ‘if’.

Leave a Reply