- Dhaka mills may face closures due to financial stress

- Ship recycling slows; only 9 HKC yards operational

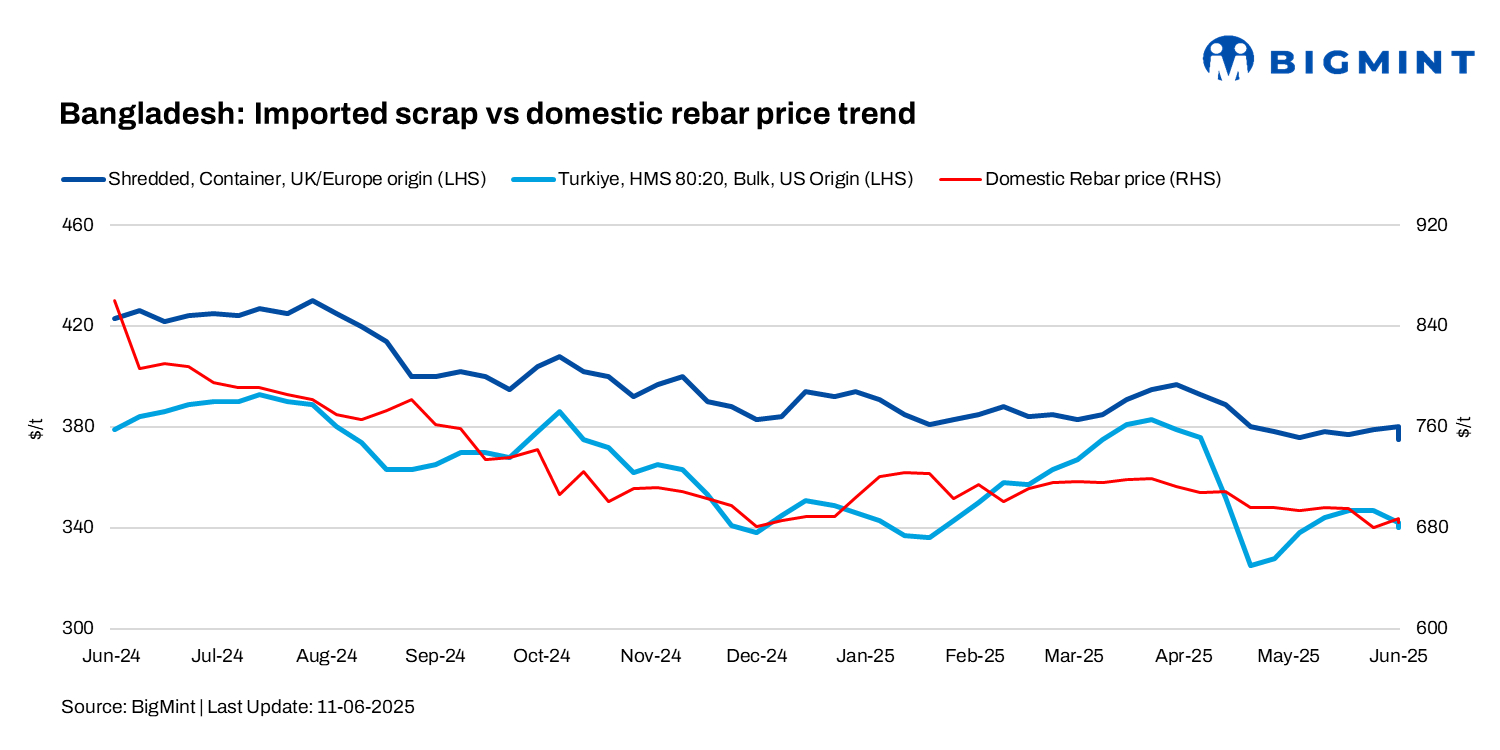

Bangladesh’s imported ferrous scrap market witnessed sluggish trading activity due to the Eid holidays, which are expected to dampen deal momentum until at least next week. Consequently, imported scrap prices dropped by up to $5/tonne (t) w-o-w, as mill-side sentiment remained subdued.

BigMint’s weekly assessments

- European-origin HMS (80:20) prices inched down by $1/t to $362/t.

- European-origin containerised shredded was down $5/t w-o-w to $375/t.

- Japanese-origin H2 bulk prices stood at $359/t CFR Chattogram, down by $5/t w-o-w.

- US-sourced HMS (80:20) bulk prices stood at $370/t, down by $5/t w-o-w.

Singapore-origin bulk offers for July shipments remained firm, with HMS 80:20 quoted at $355-360/t, PNS at $380-385/t, HMS 80:20 at $370/t, and HMS 70:30 within $350-353/t.

In the containerised segment, offers remained steady, with Australia HMS 80:20 at $355/t, GI bundles from the Philippines at $330/t, and Malaysian busheling at $380/t.

Market commentary

A major Chattogram-based mill secured the recent Kanto cargo – its first bulk booking since the Eid holidays – at around $345-350/t CFR, considered competitive in the current market.

Another key bulk scrap buyer returned to the market last month after an eight-month gap, marking its first booking since the formation of the new government.

Another Chattogram-based mill indicated that while rebar sales remained steady, the company continues to face letter of credit (LC) related hurdles in securing raw materials.

Domestic market

According to market participants, some mill closures are expected in Dhaka soon, driven by ongoing financial and operational stress. On the steel expansion project front, Meghna is expected to enter the market by 2026, while Bashundhara’s long-delayed operations now seem likely only by 2030-2032.

In the ship recycling market, Bangladesh witnessed notable activity, with several large vessels – including LNG carriers and a very large ore carrier (VLOC) – sold to recyclers, some destined for yards newly compliant with the Hong Kong Convention (HKC). However, demand in Chattogram declined sharply this week, with only 9 of the 35 HKC-approved yards currently operational. Most are now near capacity due to recent vessel arrivals, including a smaller unit that caught many by surprise.

The highlight was the sale of BERGE FUJI (37,379 LDT) at $440/LT LDT – the largest dry bulk recycling deal of 2025 so far. Despite the slowdown during the Eid holidays and a $7/t drop in plate prices to $548/t (down $30/t m-o-m), recyclers remained largely profitable.

Chattogram Port received 11,842 LDT this week, down from 24,634 LDT last week.

Outlook

Market sentiment remains positive for the rest of June, with mills expected to restock for July-August shipments as monsoon conditions ease. Rebar interest across the region may support pricing, and trading activity is likely to pick up from next week.

Leave a Reply