- 316-grade tags witness INR 4,000/t increase

- Exports sluggish, no relief for Indian producers

India’s 316-grade stainless steel (SS) finished flats prices saw a w-o-w uptick after major coil producers announced a price hike of INR 4,000/t, effective 6 June 2025. This increase was largely driven by a sharp rise in ferro molybdenum (FeMo) prices, prompting higher offers for both 316 grade hot-rolled coils (HRCs) and cold-rolled coils (CRCs).

In contrast, prices of stainless steel longs declined during the same period, as persistent weak demand continued to weigh on the segment.

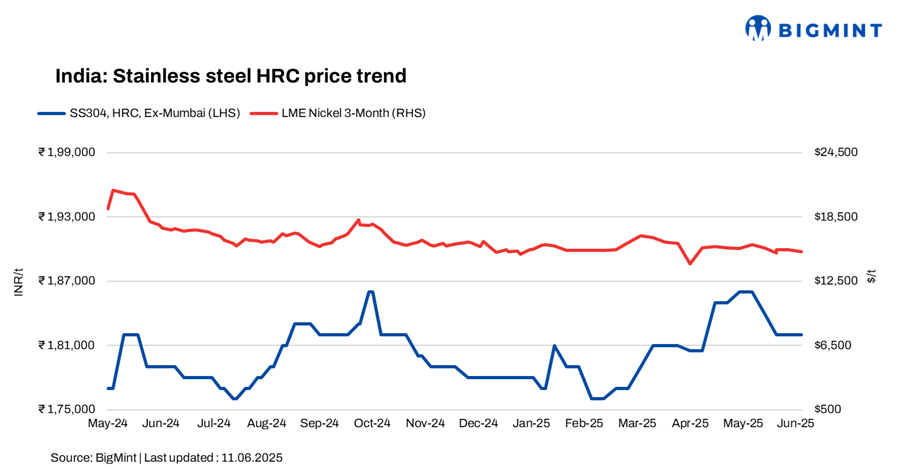

As per BigMint’s assessment, SS 316 HRCs stood at INR 325,000/t and 316 cold-rolled coils (CRCs) at INR 333,000/t ex-Mumbai, both up by INR 4,000/t w-o-w.

LME nickel tags dip, Asian NPI stable w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,240/t, down 1% against last week’s $15,425/t. Nickel stocks in LME-registered warehouses stood at 198,126 t, a 1.6% drop compared to 201,462 t in the previous week.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) stood at RMB 960/t ($133/t). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $115/t.

Market insights

A trade source said, “Demand for SS flats remains weak. While 304 prices are stable, 316 tags increased after a major coil maker raised prices. However, the rise in 316 is expected to come down due to the prevailing weak demand.”

BigMint’s benchmark assessment for stainless steel 304 series HRCs remained stable w-o-w at INR 182,000/t, while 304L (25-100 mm) black round bars stood at INR 157,000/t, both ex-Mumbai.

Demand for finished SS longs remains very weak in the domestic market, As per market participants, “Major mills are currently operating at 60-70% of their capacity. If this sluggish trend continues, production levels may be reduced even further. Export markets are also under-performing, offering little relief to Indian producers.”

Adding to the challenges, the pace of infrastructure and government projects has slowed considerably. With these projects moving at a sluggish rate, demand is expected to stay low through the monsoon season.

Chinese stainless steel prices steady

In China, prices of domestic stainless steel 304-grade cold-rolled coils (CRCs) stood at RMB 13,850/t ($1,924/t) exw, stable w-o-w, while FOB tags of 304-grade CRCs were at $1,910/t.

Raw material scenario

Ferro molybdenum: Indian ferro molybdenum prices held steady w-o-w from the last assessment on 4 June 2025, backed by consistent demand in the stainless steel sector and stable conditions in the global market.

As per BigMint’s assessment on 11 June, ferro molybdenum prices in India were at INR 2,655,000/t ($31,053/t) exw-India. Around 60 t of trades were concluded last week in the price range of INR 2,600,000-2,660,000/t ($30,410-31,111/t) exw.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 100,800/t ($1,179/t) exw-Jajpur, remaining range-bound w-o-w.

Additionally, Vedanta-Ferro Alloys Corporation (FACOR) has scheduled an auction for high-carbon ferro chrome (0-150 mm) on 13 June. The minimum allowed bid quantity for all lots is 25-300 t. In the previous auction on 21 May, the larger lot of 10-150 mm fetched an H1 price of INR 100,300/t exw. BigMint assessed ferro chrome (HC 60%, Si: 4%) prices at INR 100,800/t exw-Jajpur on 11 June.

Ferro silicon: Indian ferro silicon (70%) prices experienced a decline of INR 2,300/t ($27/t) as compared to the previous assessment on 2 June. Prices dropped as Bhutanese sellers announced their June offers at INR 92,000/t ($1,075/t) exw and subsequently, sellers in north-eastern India followed with similar offers.

As per BigMint’s assessment on 9 June, ferro silicon prices were at INR 92,000/t ($1,075/t) exw in both Guwahati and Bhutan. Approximately 1,800 t of deals were concluded last week at same price levels.

Ferrous scrap: India’s imported ferrous scrap market remained largely rangebound this week. Buyers continued to stay cautious due to weak domestic steel prices, seasonal disruptions from the monsoon, and the availability of more affordable local scrap.

Containerised shredded scrap offers slipped to $360-365/t CFR Nhava Sheva, though tradable levels were reported closer to $355-360/t. Confirmed bookings were limited, with most traders adopting a wait-and-watch approach, anticipating further price corrections or more clarity post-monsoon.

Outlook

In the near term, the stainless steel market is expected to remain subdued due to weak demand during the monsoon season. Currently, infrastructure and government projects are progressing slowly, which is likely to keep demand low throughout the monsoon period.

![]()

Leave a Reply