- Indian buyers hold off amid monsoon, weak demand

- Turkish buyers cautious, inactive post Eid holidays

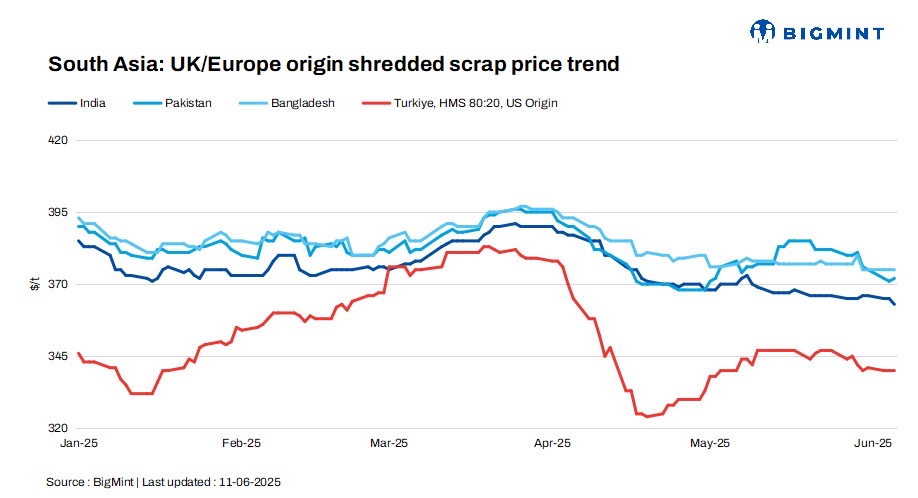

The South Asian imported scrap market remained largely inactive this week, with trade across India, Pakistan, and Bangladesh slowing due to a combination of Eid holidays, weak steel demand, and seasonal disruptions. Buyers across the region showed limited interest in fresh bookings, weighed down by falling rebar prices, high inventories, and liquidity concerns.

While India faced added pressure from the onset of the monsoon and cheaper domestic alternatives, Pakistan and Bangladesh remained quiet, with most mills yet to resume operations post-holidays. Meanwhile, Turkiye saw stable prices but subdued activity, as mills adopted a cautious stance amid higher offers and limited buying appetite.

Market overview

India: India’s market remained quiet, weighed down by falling steel prices, monsoon disruptions, and more affordable domestic scrap and sponge options. Containerised shredded was offered at $360-365/t CFR Nhava Sheva, but buyers resisted beyond $355-360/t. HMS 80:20 saw limited interest, with offers at $340-345/t CFR and bids at around $335-340/t. West African HMS, depending on loading weight, was quoted at $345-350/t CFR, though buying remained subdued.

Mills preferred domestic scrap due to better availability and pricing, while some distressed offers surfaced. With rebar sales standing moderate and weak market cues, buyers stayed cautious, expecting further softening in prices during the monsoon season.

Pakistan: Pakistan’s imported scrap market remained sluggish amid Eid holidays, with containerised shredded heard at $370-375/t CFR Port Qasim. Trading activity was thin, as most mills stayed inactive or operated at minimal capacity, holding off purchases due to high inventories and weak steel demand.

Most market participants are awaiting policy clarity post-Eid and the upcoming budget, with meaningful recovery expected to begin next week.

Bangladesh: Bangladesh’s imported scrap market remained quiet amid Eid holidays, with buyers staying on the sidelines and showing limited interest in new bookings.

Shredded offers were last heard at $375-378/t CFR Chattogram, while HMS 80:20 ranged between $355-360/t CFR. No fresh container deals were reported, and Dhaka-based mills continued to hold back, weighed down by past letter of credit (LC) issues.

In the bulk segment, a major steel mill secured the Japanese Kanto tender at $345-350/t CFR, while another significant market player re-entered the market after a long pause.

Despite current inactivity, sentiment remains positive, with expectations of restocking for July-August once Eid and monsoon disruptions ease in the coming weeks.

Turkiye: The Turkish imported scrap market remained stable, with premium HMS 80:20 assessed at $340/t CFR. Mills returned from Eid holidays but stayed largely inactive, collecting offers without making bids. Sources noted Turkish buyers were not in a hurry to book cargoes, reflecting a cautious sentiment.

An unconfirmed EU-origin deal at $332/t CFR was heard, but overall market activity remained low. Recyclers in the Baltic and Eurozone cited high collection costs and forex challenges, making it unviable to sell at current prices without incurring losses.

With no clear direction, participants described the market as stuck in a wait-and-see mode, with uncertain pricing and subdued trade interest.

Price assessments

India: UK-origin shredded indicatives were assessed at $363/t CFR Nhava Sheva, down by $2/t d-o-d.

Pakistan: UK-origin shredded indicatives stood at $372/t CFR Qasim, up by $1/t d-o-d.

Bangladesh: UK-origin shredded prices were assessed stable d-o-d at $375/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $340/t CFR Turkiye, unchanged d-o-d.

Leave a Reply