- Indian Ocean rates dip on limited cargo, ample vessels

- FMG, BHP, Rio Tinto bookings boost Capesize freights

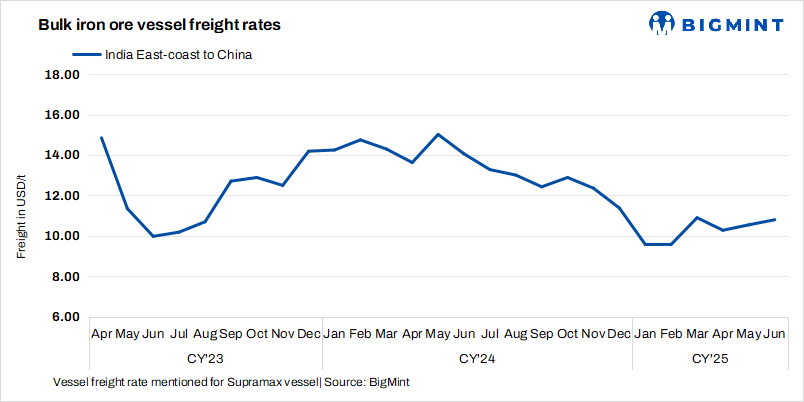

Dry bulk iron ore freight rates from the Indian Ocean to China inched down w-o-w following the overall lack of fresh demand and subdued trading activity on the heels of a long weekend. With many market participants just returning to their desks, fixture activity remained low and sentiment was generally weak. This led to reduced urgency among charterers, limiting upward movement in freight rates and contributing to a marginal softening in the market.

Additionally, the Indian Ocean continued to face a build-up of prompt tonnage with limited fresh cargo enquiries, creating an oversupply of vessels relative to available shipments. This imbalance put downward pressure on freight rates. In the broader Asian market, sentiment remained muted as trading volumes were thin and no significant new drivers emerged, reinforcing the slow pace of recovery and resulting in a slight dip in rates on the India-China dry bulk route.

The increase in Capesize freight rates for iron ore shipments was primarily driven by a rebound in demand from key charterers such as FMG and Rio Tinto, who returned to the market seeking vessels for late July laycans. Despite the overall subdued sentiment and limited fresh cargoes, these charterers’ requirements injected renewed activity into the Pacific market. Their vessel bookings created upward pressure on rates, especially amid a gradual build-up in tonnage that had not yet fully translated into excess availability.

Bad weather in North China and Changjiangkou, with strong winds and thick fog, forced some ports to close for a while. This caused delays in ship schedules and slowed down the movement of vessels. At the same time, there weren’t enough ships available right away, and ongoing transport issues added to the pressure. As a result, freight rates went up for a short time before starting to drop again.

Factors influencing freights

- Baltic indices rise w-o-w, BSI goes contrarian: The Baltic indices, indicating trends in vessel demand, remained positive w-o-w except Baltic Supramax Index (BSI). The Baltic Dry Index (BDI) was recorded at 1,633 on 9 June, increasing by 215 points w-o-w. Additionally, the Baltic Capesize Index (BCI) stood at 2,842, up sharply by 565 points w-o-w. However, the BSI inched down by 18 points w-o-w to 933.

- China’s iron ore spot prices firm w-o-w: Chinese spot prices of iron ore fines (Fe62%) were assessed at $94.95/t CFR on 10 June, remained steady w-o-w amid improved market liquidity and declining inventories. Production curbs are not anticipated in the near term, amid ample supply. Port procurement is being prioritised by mills, as healthy profit margins allow cost-effective sourcing strategies to be maintained.

Route-wise updates

- India-China: Freights from the Indian Ocean to China were recorded at $10.6/t, inching down by $0.4/t w-o-w. According to market sources, a Supramax vessel was recently fixed at approximately $8.75/t for a prompt shipment, while several other fixtures were heard at levels of $9.9/t for the mid-June shipments.

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $9.9/t on 11 June, rising by $0.8/t w-o-w. According to sources, major Australian miners Rio Tinto, BHP and FMG booked Capesize vessels from a Western Australian port to Qingdao at around $9.50-10.40/t. Shipment is scheduled for 19-29 June.

- Brazil-China: Freights for Capesize vessels from Brazil to China fell this week. Rates from Tubarao to Qingdao Port were assessed at $23.4/t on 11 June, climbed by $1.4/t w-o-w. As per sources, Vale booked two Capesize vessel from Tubarao to Qingdao at $23.50-24/t for the shipment period of 18-28 June.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao increased by $1.5/t w-o-w to $17.4/t on 11 June despite the absence of reported fixtures on this route.

Leave a Reply