- Scrap shortage continues to support firm pricing

- Major automaker’s settlements expected to rise for Jul’25

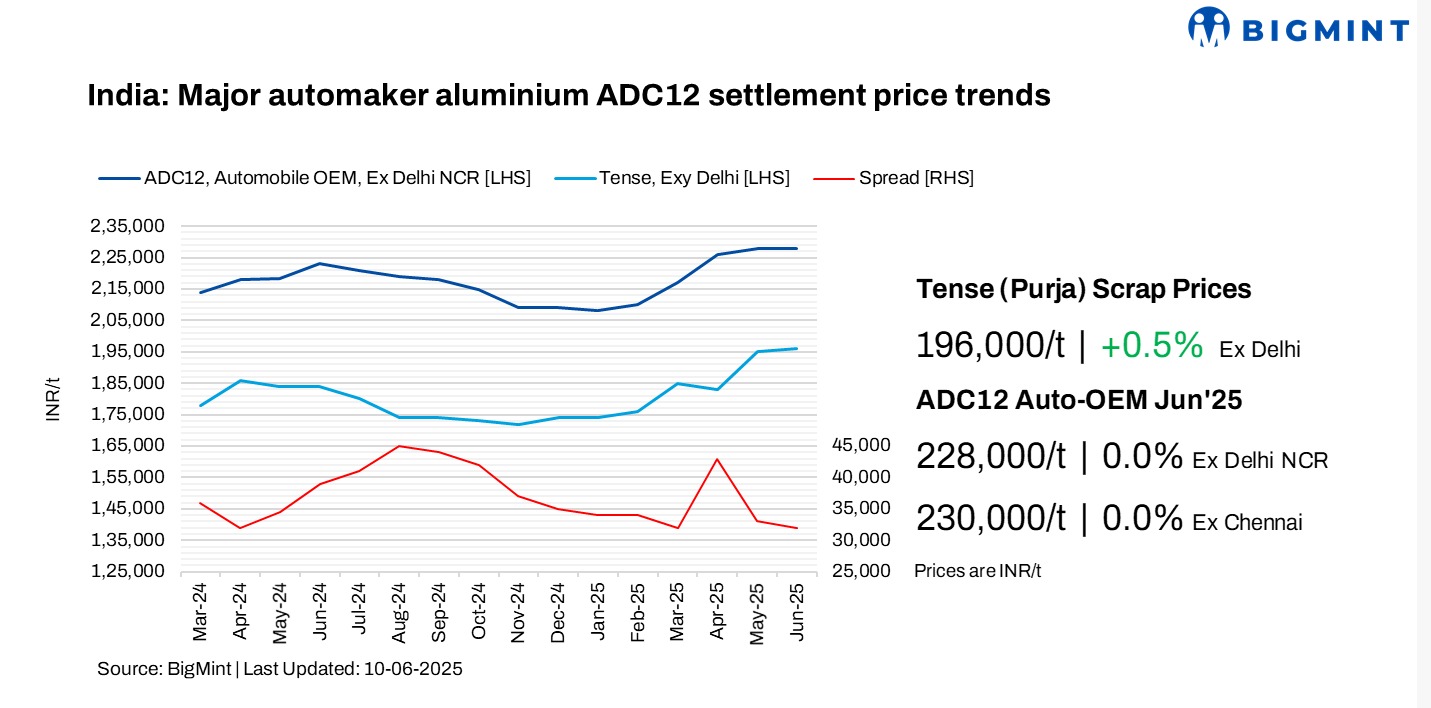

Aluminium ADC12 alloyed ingot prices remained stable m-o-m in June 2025 across both northern and southern India, according to BigMint‘s benchmark assessments. Steady pricing was supported by ongoing shortages of raw materials used in alloy ingot production.

BigMint’s monthly assessment for the OEM grade of ADC12 stood at INR 228,000/tonne (t) in Delhi, and INR 230,000/t in Chennai.

The spread between scrap and semi-finished products narrowed to INR 32,000-33,000/t due to increased Tense scrap costs.

Meanwhile, three-month London Metal Exchange (LME) aluminium average prices hovered at around $2,460/t in June, largely stable m-o-m from the previous month’s $2,450/t. At the time of reporting, LME aluminium prices had increased to $2,517/t. The inventory levels at LME warehouses in June had decreased to 365,375 t, down by 7.5% m-o-m from 394,876 t in May 2025.

Market insights

The offer levels for ADC12 continue to remain on the higher side in both north and the south market hovering between INR 232,000-233,000/t in Delhi and INR 233,000-235,000/t in the Chennai market.

The bid levels in the north region are heard at INR 226,000-227,000/t levels and in the south region the bid levels are at INR 228,000-229,000/t.

A scrap trader noted that scrap availability in the northern region is relatively better than in the south, leading to higher alloy and scrap prices in southern markets compared to the north.

A domestic market participant remarked, “Despite the recent dip in LME prices, scrap rates remain elevated due to tight availability. The shortage caught many by surprise, leaving most participants with low inventory levels. Imports of ADC12 from Malaysia are also facing BIS-related challenges, with landed costs around INR 230,000/t. As a result, alloy ingot manufacturers are finding it difficult to maintain production and meet demand, keeping prices firmly supported.”

According to market sources, a major automaker is reportedly being quoted INR 230,000–232,000/t for July 2025 settlements. While official confirmation is still awaited, the market anticipates an upward revision in settlement levels for July.

In the Southern market, the ADC12 market in Chennai remains relatively firm, with most producers yet to settle and instead opting for rollover strategies, largely due to steady scrap prices. Tense scrap continues to trade in a stable range, quoted around INR 197,000-198,000/t in Chennai and INR 198,000–199,000/t in nearby Coimbatore.

Capacity utilisation among major ADC12 producers in Chennai is currently heard at 55-60%, reflecting cautious production amidst tight raw material availability.

On the import front, Malaysian ADC12 suppliers are reportedly in the process of applying for BIS certification, which could influence future supply dynamics if approvals come through. For now, raw material shortages continue to be a key concern, keeping sentiment firm in the regional market.

Alloy exim trends

Imports: According to BigMint‘s latest data, total alloy ingot imports in April 2025 stood at 19,425 t, with no recorded imports of ADC12 during the month. Among the imported volumes, A356 accounted for 11,185 t holding the major share.

Export: India’s exports have currently been at nil levels due to weak export market sentiments as well as strong domestic demand in India amid prevailing raw material shortages.

Raw material price trends

In June 2025, prices of the basic raw material for aluminium alloys, that is scrap, saw a rise m-o-m. US-origin Tense scrap inched up by $30/t to $1,990-1995/t, while UK-origin Wheels rose by $35/t to $2,520/t. Zorba 95/5 from the UK stood at $2,160/t CFR west coast, India, up by $15/t w-o-w.

In the domestic market, Tense scrap prices remained range-bound m-o-m in both Delhi and Chennai. According to BigMint’s assessment, prices stood at INR 196,000/t ex-Delhi and INR 197,000/t ex-Chennai.

Silicon price trends

According to BigMint’s assessment, prices of China’s 553-grade silicon dropped by $75/t m-o-m to $1,230/t CFR Mundra.

The price decline was mainly driven by weak demand, as most alloy ingot manufacturers have already stocked up on material and are currently holding off on new purchases.

Outlook

Prices are expected to remain firm amid ongoing raw material shortages. Additionally, the market is closely watching the upcoming settlement levels from major automakers for July, with expectations of a possible increase.

Leave a Reply