- Chinese pre-monsoon restocking boosts volumes in May

- Domestic trades offer better realisations to suppliers

- Flagging China demand darkens iron ore export prospects

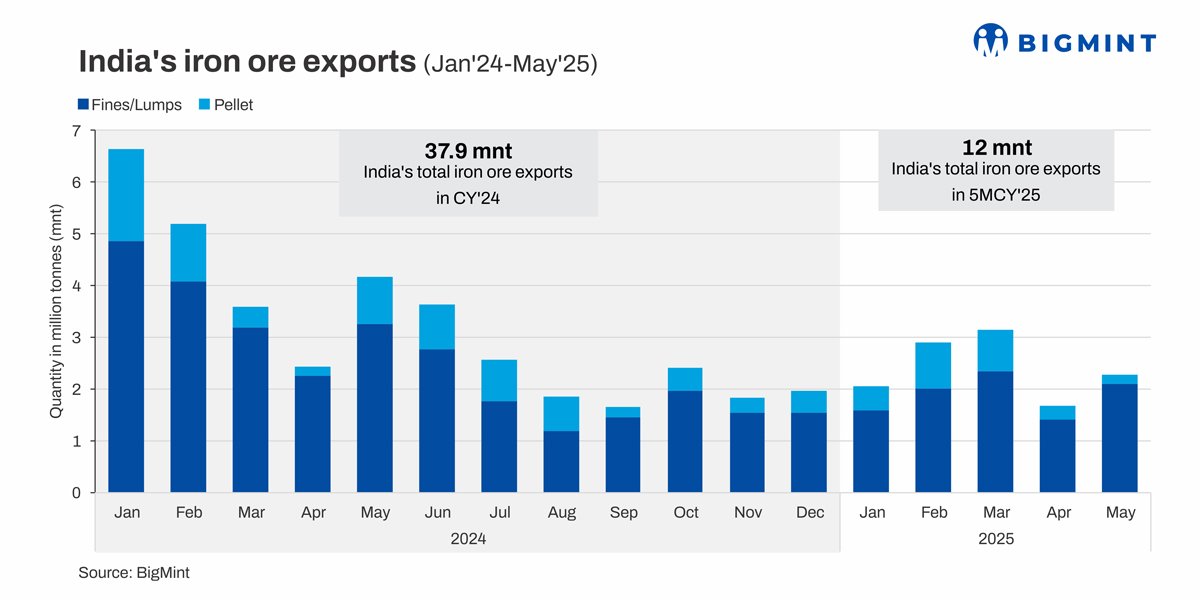

Morning Brief: India’s iron ore and pellet exports remained lacklustre in May 2025, though they shot up by 35% to 2.26 million tonnes (mnt) from a four-month low of 1.68 mnt in April. However, there was a sharp 46% decrease compared to the 4.17 mnt recorded in May last year.

Meanwhile, exports totalled 12.01 mnt in January-May, again recording a steep 45% drop from 22.01 mnt in the corresponding period last year (CPLY).

BigMint goes behind the scenes.

Commodity-wise break-up

Exports of iron ore fines surged by 50% m-o-m to 2.1 mnt in May, while those of pellets plunged 41% to 0.16 mnt.

Iron fines exports were lower by 46% y-o-y in January-May at 9.43 mnt. Moreover, pellet exports were down by an equally steep 41% y-o-y at 2.57 mnt.

What led to rebound in iron ore, pellet exports in May?

Exports to China recover on restocking demand: Volumes to China experienced a mild recovery in May, buoyed by pre-monsoon restocking demand and the 90-day truce in the reciprocal tariff war with the US. Exports rose by 13% m-o-m to 1.68 mnt in May from a seven-month low of 1.49 mnt in April.

Following easing trade tensions, iron ore prices climbed up, and optimism prevailed in the market. Higher prices and a pick-up in buying interest encouraged Indian exporters to strike deals. However, prices moderated eventually, fuelled by softening demand and cautious sentiment.

Another factor that contributed to higher exports to China was mills’ strategic sourcing of mid-to-low-grade material. To preserve profit margins amid deteriorating steel prices, mills held off from procuring higher grade fines, especially those above Fe 62%, as they were less economically viable. Indian exports, which are mainly of Fe 57% fines, suited Chinese mills’ requirements.

Why did iron ore, pellet exports sink in Jan-May?

Declining margins put off exporters: Indian (Fe 57%) export prices fell $30/t to $60/t FOB east coast in May from $90/t in January 2024. Such a steep decline put off exporters, as it significantly reduced margins and made overseas shipments unfeasible.

Only leading players such as Rungta Mines and Vedanta were active in the iron ore export landscape, due to prices falling below the psychological $75/t CFR mark.

Meanwhile, realisations from domestic trades were better. To illustrate, benchmark Odisha iron ore fines (Fe 62%) stood at INR 5,180/t ($61/t) in May compared to INR 5,660/t ($66/t) in January 2024, a modest decline in comparison.

For pellets, domestic prices exceeded export offers by nearly INR 1,800/t ($21/t) in March-May of this year, climbing up substantially from the average INR 800-1,000/t ($9-12/t) in January-February.

China’s iron ore imports contract: China’s iron ore and concentrates imports fell 5% y-o-y to 486.41 mnt in January-May. Market uncertainty regarding potential production cuts, the tariff war with the US, and flagging domestic steel demand led mills to cut down on purchases.

Additionally, iron ore stockpiles at major ports were higher y-o-y – averaging at 140 mnt in January-May against 136 mnt in the year-ago period. Chinese mills opted to make use of these inventories rather than placing new import orders.

Outlook

India’s iron ore exports may continue to trend down, as Chinese prices are likely to fall further. The country’s crude steel production is expected to edge down in this calendar year. Additionally, given that Indian production momentum is set to remain robust, iron ore suppliers may keep their focus on domestic trades because of better realisations. However, pre-monsoon restocking and the current preference for lower grades may prop up volumes, though these factors are unlikely to offer steady or substantial support.

Notably, India slipped to the seventh rank among global exporters in Q1CY’25 compared to fourth earlier. The slide is likely to continue.

Leave a Reply