- Australian PHCC prices edge up on supply disruptions

- Easing US-China trade tensions support iron ore fines

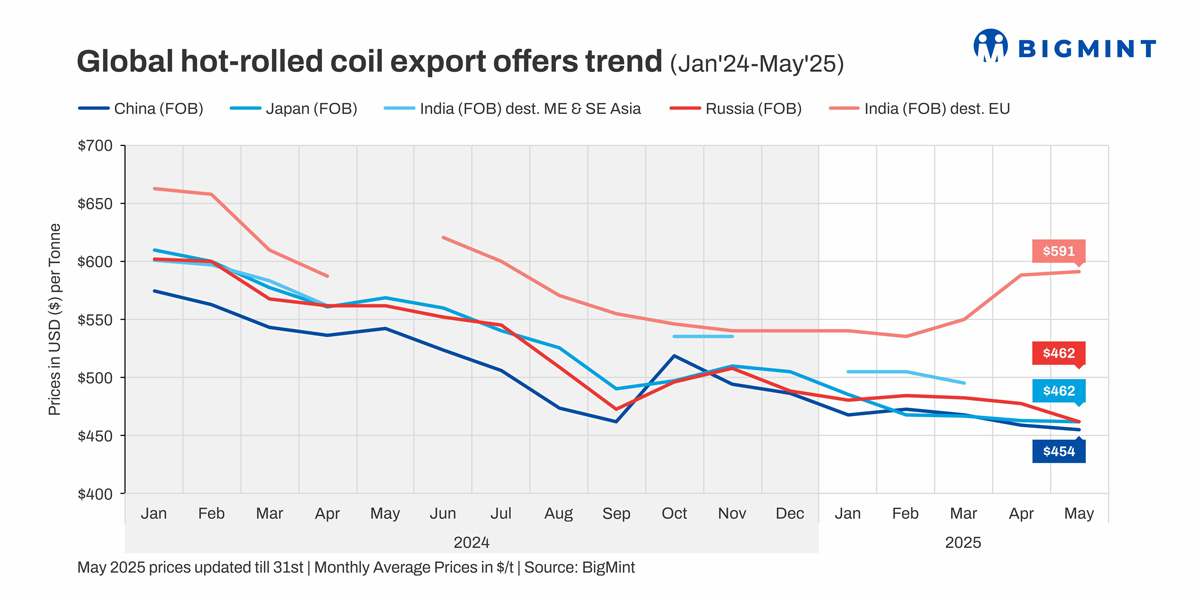

- China’s HRC export tags fall as supply outstrips demand

Morning Brief: Global steel and raw material prices largely declined in May 2025, as mounting Chinese steel exports (up 10% y-o-y and 1% m-o-m to a seven-month high of 10.6 mnt) led to a demand contraction across various commodities and regions. May marked the third consecutive month in which China’s exports exceeded 10 million tonnes (mnt).

Moreover, the trade war ignited by Trump kept the market uncertain and cautious.

Only coking coal prices registered a notable uptick m-o-m, and while India’s hot-rolled coil (HRC) offers to the EU inched up, trade activity was limited. Prices of all other commodities eroded m-o-m.

Factors influencing global steel, raw material prices in May’25

Iron ore prices in China dip in cautious market: Australian iron ore fines, CFR China, declined marginally by $1/tonne (t) m-o-m to $99/t in May, amid cautious sentiment.

To start with, the Labour Day holidays led to a market freeze at the beginning of the month. However, as trading resumed, price tags gained, riding a wave of optimism, with the People’s Bank of China announcing measures to boost liquidity. Subsequently, a significant boost came from the 90-day pause on the tariff war between the US and China.

Nonetheless, after the initial euphoria faded, sentiment weakened, with some quarters deeming the easing of monetary policies as insufficient and questioning whether the tariff truce would lead to a substantial economic improvement.

Later on, with the onset of summer and heavy rains in some regions, there was a slowdown in construction activity, which reduced steel demand and, consequently, iron ore.

Australian PHCC surges on supply constraints: Following an $8/t m-o-m spike in April, Australian premium hard coking coal (PHCC), CFR India, climbed up by $9/t to $206/t in May. The price rise stemmed from supply constraints, driven by weather-related logistics challenges, and active restocking before the arrival of monsoon in the country.

Turkish scrap tags tumble amid bid-offer disparities: Prices of HMS (80:20), CFR Turkiye, dived by $11/t m-o-m to $342/t in May, as buying interest was lean, with mills pushing back on prevailing offers. Additionally, domestic construction demand was tepid, while scrap supply was plentiful, which also motivated mills to ask for prices.

Ultimately, recyclers had to give in to lower bids, given that their yards neared maximum capacity, and they had to recover costs to sustain further collections. Moreover, the availability of competitively priced imported billets dampened scrap demand.

HRC export prices edge down as oversupply persists: Chinese HRC export prices were at an intra-year low of $454/t FOB in May, down $5/t m-o-m.

China continued to struggle with a surplus, and demand was soft, with Vietnamese buyers staying away due to the ongoing anti-dumping investigation and concerns about the possible inclusion of wider-width coils under its purview. Market uncertainty regarding the tariffs also prompted a rush to offload material.

As a result, exporters pruned offers to draw in buyers. Although favourable macroeconomic sentiment following the US-China trade talks propelled offers higher, eventually, prices slumped as importers remained indifferent to these values.

On the other hand, Indian mills continued to be largely inactive in the Middle East and Southeast Asia, amid competitive offers from China and higher domestic realisations. Conversely, offers to the EU strengthened by $3/t m-o-m to $591/t, though exports were sluggish due to lacklustre demand.

Meanwhile, Japan’s HRC offers inched down by $1/t m-o-m to $462/t FOB.

Russian billet tags plunge amid competitive Chinese offers: Russian billet prices eroded by $14/t m-o-m to $428/t FOB Black Sea, tracking subdued demand in the Turkish and North African markets. A decline in Chinese billet tags, by RMB 40/t ($6/t) to RMB 2,940/t ($409/t), and in Turkish scrap also weighed on Russian offers, while a strengthening rouble squeezed export margins.

Waning demand continues to pressure Turkish rebar: Mirroring the decline in scrap tags, Turkish rebar prices fell by $11/t to $553/t FOB. Although this period marks the peak construction season, demand was subdued, and falling scrap prices failed to offer cost support to mills.

While sales improved later in the month, mills did not drive up prices due to resistance from buyers. Additionally, as Eid approached, bearish signals emerged, and prices softened again.

Furthermore, Turkish rebars faced pressure from corresponding Chinese tags, which approached eight-year lows near the month-end.

Outlook

As long as the steel overcapacity and macroeconomic slowdown in China remain unresolved, the downtrend in global steel and raw material prices is expected to continue. However, fluctuations in market fundamentals may occasionally lead to a spike in prices.

Notably, the Chinese summer season has arrived, which may suppress domestic demand and foster further export urgency. Although contracting mill margins may lead to lower crude steel production this year, the drop is unlikely to have a major positive impact. This is because many markets, domestic and global, remain oversupplied due to months of surplus production.

Additionally, domestic steel demand is likely to shrink further this year, while Trump’s tariff blitz may keep the market on its toes. These could also unleash additional rounds of an export offensive and aggressive price undercutting.

Moreover, global crude steel production is on the decline, with volumes down by 0.4% y-o-y in January-April. This will naturally curb raw material demand.

As a result, prices may remain in the red in the near future.

Leave a Reply