- Year-on-year growth driven by downstream recovery

- Duty waiver, cable sector expansion to support Q2 demand

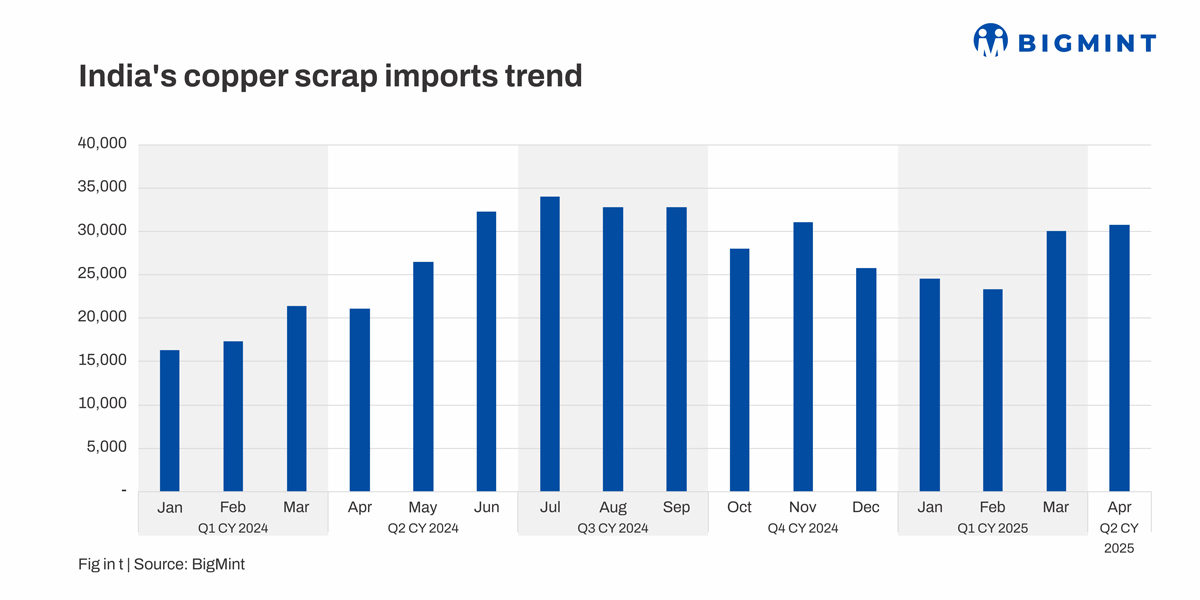

- Imports edge up as refiners restock post-Q1 slowdown

India’s copper scrap imports rose to nearly 30,800 tonnes (t) in April 2025, marking the highest monthly inflow since November 2024, when volumes stood at around 31,100 t. While the April figure was relatively flat on a month-on-month basis, it reflects a shift in market sentiment as downstream refiners and recyclers moved to replenish inventories after a subdued first quarter.

The recovery in April follows a pronounced dip in domestic scrap availability during Q1 2025, which typically sees a lull in post-festive disposal. Industry participants cited improved demand visibility and expectations of stronger summer consumption as key drivers behind the renewed import momentum.

Why did imports surge y-o-y?

Compared to roughly 21,100 t in April 2024, this year’s imports registered a sharp 46% increase. This surge reflects stronger appetite from processors and traders, many of whom were restocking ahead of the seasonal rise in demand from construction and power transmission sectors. With January-April 2025 cumulative imports reaching about 108,800 t, India is tracking ahead of last year’s pace and is on course to surpass 2024’s full-year total of around 319,400 tonnes if current trends continue.

India imported around 78,000 t of copper scrap in Q1 2025 – up as against 55,055 t during the same period in 2024. The uptrend signals improving demand from secondary manufacturers despite seasonal dips in domestic scrap collection post-festive season.

What constrained domestic scrap supply earlier in the year?

India’s scrap supply chain is heavily reliant on the informal sector, which accounts for over 85-90% of recyclable copper collection. This includes street-level kabadiwalas, small aggregators, and unlicensed dismantlers, whose operations are highly seasonal and cash-dependent. In Q1 2025, scrap generation was hit by the typical post-Diwali decline in volumes, as per sources.

This seasonal bottleneck, combined with cautious downstream sentiment, led to tight scrap availability, prompting refiners to shift towards imports as a more reliable source.

How is the scrap mix evolving?

In April, Brass Honey emerged as the largest grade by volume, accounting for 39% of imports, up from 35% in March. Druid held the next largest share at 22%, followed by Birch at 13%, Berry at 9%, and Barley at 5%. Berry’s share fell from 11% in March, reflecting grade rotation and selective buying. Clove remained flat in percentage terms at 3%, although actual tonnage edged up. The ‘Others’ category expanded to 9%, indicating a broader diversification in sourcing amid tightening premium-grade supply.

While Druid and Birch saw mild declines, the composition suggests refiners are adjusting grade preferences based on price-performance and feedstock compatibility, particularly for ISI-grade copper wire applications.

Who are the top suppliers?

Germany led the pack in April with 4,100 t, followed by the United States, which shipped nearly 4,000 t-marginally lower than in March. The US remains a steady source of Berry and Candy scrap, preferred by Indian manufacturers of ISI-grade and low-resistance wires. Supply consistency and predictable specifications make these grades ideal for wire and cable producers seeking ≥99.9% purity inputs.

What’s driving downstream copper demand?

The post-fiscal year-end period has seen a revival in orders from the wire and cable segment, especially from power utilities and the electric vehicle ecosystem. Manufacturers are actively sourcing Berry and Candy scrap to meet stringent conductivity standards. Simultaneously, Birch/Cliff and ICW (insulated copper wire) grades are being restocked by secondary smelters in Delhi, Bhiwadi, Daman, and Ludhiana-key hubs supplying regional construction and informal electrification projects. This divergence in grade-specific demand is shaping Q2 procurement strategies.

Policy tailwinds and sector expansion to boost Q2 imports

A key development supporting imports is the removal of basic customs duty on non-ferrous scrap, including copper, as announced in the Union Budget 2025–26. According to sources, this move significantly improves the landed cost economics for high-grade scrap imports, particularly from Europe and the US.

At the same time, leading cable manufacturers—Polycab, RR Kabel, and KEI Industries-have announced capacity expansions exceeding 200,000 km/year for FY 2025-26. These additions are expected to lift demand for clean copper scrap, further reinforcing the import pipeline over the coming quarters.

Domestic Copper Prices:

BigMint’s May 2025 assessment showed mixed trends across domestic copper products. Prices for Delhi secondary CC wire rods edged up by 0.6% to ₹845,000/t, while primary CC rods gained 2.2% to ₹877,000/t, tracking firmer refined copper values. However, copper armature prices remained flat at ₹788,000/t ex Delhi.

Imported Scrap Prices:

Imported scrap prices posted broad-based gains in May. Brass Honey scrap (Middle East origin) rose 7.0% m-o-m to $6,245/t, driven by tighter regional availability. US Motor Mix increased modestly by 1.7% to $1,167/t. Copper Birch Cliff scrap (CFR Mundra) also strengthened by 4.7% to $8,885/t.

Outlook

The 0% basic customs duty on copper scrap imports, effective from the Union Budget 2025–26, is expected to support higher import volumes in the coming months. With improving domestic demand, favourable landed costs, and steady grade-specific buying by wire and cable manufacturers, copper scrap inflows are likely to remain robust through Q2 and beyond.

With scrap supply in the domestic market still normalising and policy changes lowering barriers for high-grade imports, India’s copper scrap demand is poised for continued strength in Q2. The wire and cable sector remains the key consumption driver, with procurement increasingly focused on consistent, low-impurity grades to meet expanding downstream specifications.

If April’s momentum holds, 2025 could emerge as a record year for India’s copper scrap imports, underpinned by structural demand growth and improving sourcing flexibility.

Leave a Reply