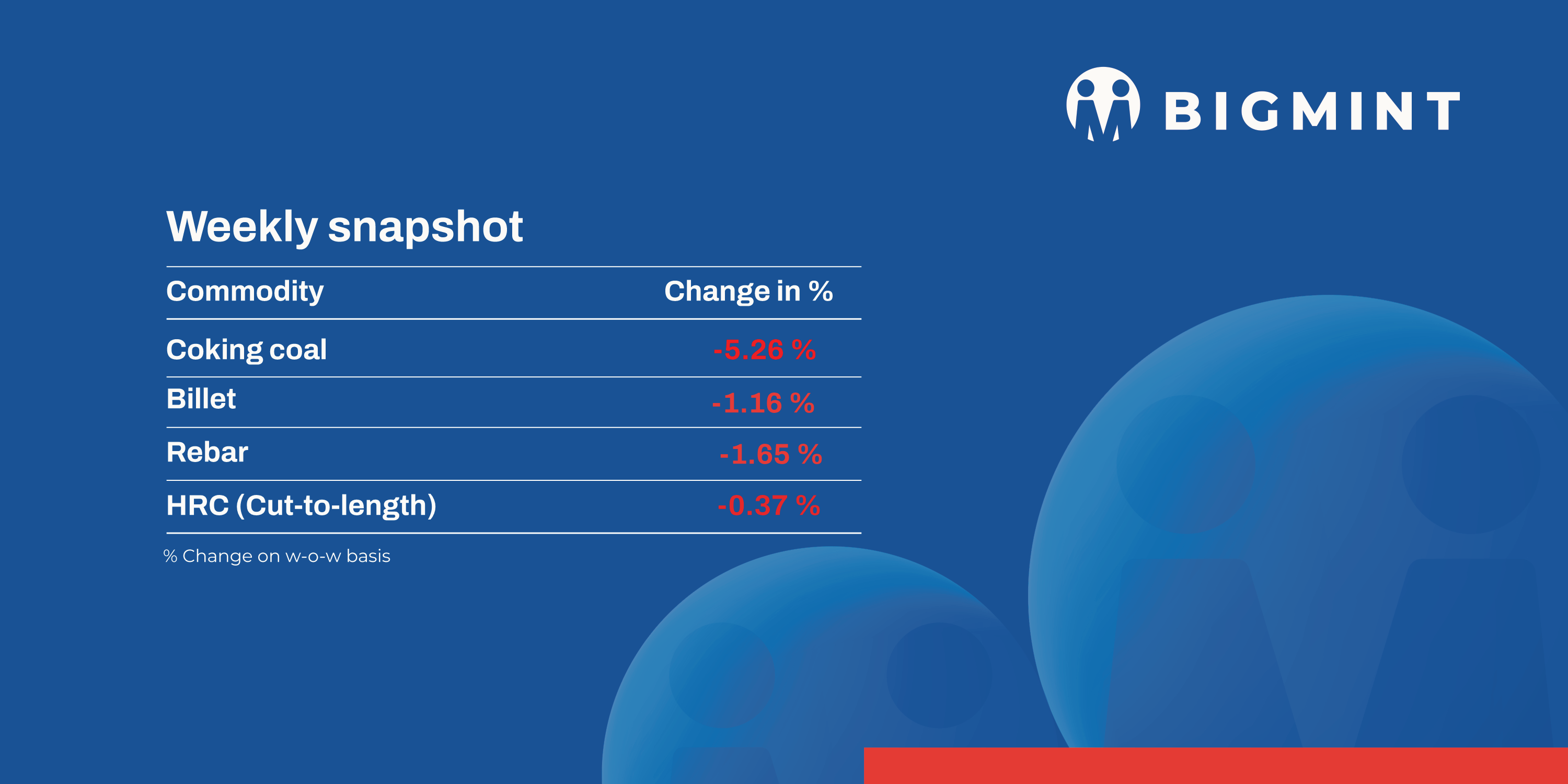

The domestic steel market saw mixed trends during week 23 (2-7 June, 2025). Semi-finished steel prices varied within the range INR 100-800/t, while flat steel prices remained unchanged. Most mills have confirmed prices for June, but a few others are yet to make official announcements.

Iron ore & pellet

NMDC has decreased list prices of iron ore CLO (calibrated lump ore) and fines. The miner has fixed prices of DR CLO (10-40 mm, Fe 67%) at INR 7,050/t ($82/t) and of iron ore fines (-10 mm, Fe 64%) at INR 5,350/t ($62/t), a decrease of INR 150-160/t ($2/t). Prices are on FOR basis from its Bacheli complex and include royalty, DMF and NMET.

Jindal Steel and Power (JSP) emerged as the highest bidder for Roida-I Iron Ore and Manganese block auction offering a premium of 117.5%. The block, of around 104.84 Ha, is located in Keonjhar district, Odisha and has geological resources of 126.05 mnt. The mine comprises deposits of average-grade Fe 59.97% at 45% Fe cut-off.

BigMint’s bi-weekly domestic pellet (Fe63%) index remained stable w-o-w at INR 9,250/tonne (t) ($108/t) DAP Raipur on 6 June. Raipur-based pellet producers kept offers for Fe 62/63% (+/- 0.5%) at INR 9,100-9,200/t ($106-107/t) exw. Around 120,000 t of trades took place this week in Raipur region by local suppliers.

Coal

South African thermal coal prices at Indian ports dropped by INR 50–100/t last week due to reduced inquiries and monsoon-led disruptions. RB2 (5500 NAR) was assessed at INR 7,800/t and RB3 (4800 NAR) at INR 6,850/t exw-Gangavaram, with few confirmed trades. Buyers quoted unrealistic bids, especially for lower NAR coal. Thermal coal portside stocks in India rose 3% w-o-w to 15.40 mnt.

Domestic coal prices fell again this week due to subdued industrial offtake and steady supply. The 4500 and 5000 GCV grades dropped by INR 50/t to INR 4,250/t and INR 4,750/t exw-Bilaspur, respectively. In recent trades, 5000 GCV coal was booked for West Bengal at INR 6,900/t exw-Raipur. Additionally, an ECL G4 grade cargo of 6,000 t was sold at INR 6,650/t, reflecting selective restocking.

Metallurgical coke prices in India extended downtrend last week, with 25-90 mm BF grade falling by INR 700/t to INR 30,800/t ex-Jajpur and INR 200/t to INR 30,600/t ex-Gandhidham. Poor steel sector demand and cautious procurement led to reduced enquiries. Chinese coke markets also softened, with a third price cut likely. Outlook remains bearish amid policy uncertainty and tepid global cues.

Ferrous scrap

Imported scrap remained largely stable last week, with shredded scrap prices assessed at $366/t CFR, unchanged w-o-w. Trade activity stayed subdued despite a wide range of offers-shredded between $365-375/t CFR and HMS 80:20 between $340-355/t CFR. Some deals were concluded at $360-365/t for shredded and $340-345/t for HMS, but most buyers resisted higher levels. A slight rise in freight rates towards the end of the month provided marginal support to supplier offers, though overall demand remained weak.

Around two bulk vessels arrived this week–one at Kandla carrying approximately 32,000 t of mixed US-origin scrap, and another at Chennai with about 27,000 t of Korean-origin material. The market was already oversupplied, and these fresh arrivals have added further pressure to an already weak sentiment.

Last week around 6,000 t of imported scrap was booked including HMS, HMS 80:20 and PNS from Brazil, the Caribbean, West Africa and Bahrain.

Ferro Alloys

Silico manganese

Indian silico manganese prices witnessed a slight decline of INR 300/t ($4/t) w-o-w to INR 71,200-71,900/t ($830-838/t) in the key regions of Durgapur, Raipur and Vizag. The price stability reflects softening demand in the steel segment, which kept alloy buyers cautious and market sentiment subdued.

Meanwhile, export prices of the 65-16 grade declined by $19/t w-o-w to $913/t FOB Vizag/Haldia, India, amid limited inquiries.

MOIL reduced manganese ore prices effective 1 June, slashing ferro grades (above and below Mn 44%) by 5%, and SMGR grades (Mn 30%, Mn 25%) by 5–15%.

Additionally, on 5 June, Sandur Manganese and Iron Ore (SMIORE) conducted an auction for 25,704 t of manganese ore (fines and lumps, Mn 18-35%, -10 to 100 mm). Of the total quantity offered, only approximately 8,568 t (33%) was successfully sold, with prices ranging between INR 2,520/t and INR 10,310/t. Consequently, around 17,136 t remained unsold.

Ferro manganese

Indian ferro manganese (HC 70%) prices dropped by INR 400/t ($5/t) w-o-w to INR 72,100/t ($840/t) exw in Durgapur. Meanwhile, prices, exw-Raipur, also decreased by INR 550/t ($6/t) to INR 72,250/t ($842/t). Buyers pushed back against higher offers due to lacklustre demand, sufficient inventories, and weak market sentiment across major regions.

Ferro silicon

Indian ferro silicon prices eased by INR 2,300/t ($27/t) w-o-w, settling at INR 92,000/t ($1,072/t) ex-works Guwahati. Bhutanese prices also softened by INR 2,900/t ($34/t) to INR 92,000/t ($1,072/t) ex-works. This decline followed Bhutan’s preliminary price announcement, which is intended as a market probe rather than a definitive monthly rate.

Ferro chrome

Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices inched up by INR 500/t ($6/t) w-o-w, reaching INR 100,500/t ($1,171/t) ex-works Jajpur. The marginal increase was driven by reduced availability in the spot market. Market sentiment is cautiously optimistic, with upward pricing potential. However, the trajectory will largely hinge on buyer response and overall market participation in the coming days.

Semi-finished steel

Indian semi-finished steel prices showed mixed trends, as per BigMint’s assessment. Domestic billet prices in all key locations decreased by INR 100-800/t, while a major drop of INR 800/t was seen in Mumbai. Similarly, sponge iron prices showed a downward trend, moving down by INR 100-300/t, with a major decrease of INR 300/t seen in the Mandi Gobindgarh region.

Indian DRI (Direct Reduced Iron) export offers decreased by $2 for CPT Raxaul to $332/t, while CPT Benapole offers decreased by $2/t to $332/t.

Finished long steel

IF-rebar: India’s induction furnace route rebar prices continued to face pressure this week, recording further declines. Trading activity remained sluggish across regions, with buyers only purchasing based on immediate needs. The gap between bid and offer prices led manufacturers to lower their offers to stimulate sales. Retailers remained cautious, avoiding bulk buying due to market uncertainty. This slowed demand, increased sales pressure at mills, and led to an inventory pile up. Prices are likely to remain subdued amid no clear signs of recovery.

On a weekly basis, rebar prices declined in the range of INR 100-1,800/t across regions.

The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 41,500-41,900/t exw Raipur and INR 45,200-45,800/t exw Jalna.

The trade reference price of heavy structural steel for base size 150mm channel stands at INR 43,700-44,200/t exw Raipur.

Trade reference prices of wire rods hovered at INR 42,200-42,700/t ex Raipur.

BF-rebar: Indian Tier-1 mills reduced rebar list prices by up to INR 1,500/t for early-June deliveries as against prices prevailing in end-May. Post-revision, list prices were INR 54,500-55,500/t on landed basis. It should be noted that mills had offered discounts/rebates to augment sales last month.

Trade-level BF rebar prices declined by INR 1,200/t w-o-w to INR 54,300/t exy-Mumbai on 6 June. Prices are exclusive of GST at 18%.

In the projects segment, prices witnessed a drop of INR 1,000/t w-o-w to INR 53,000-53,500/t FOR Mumbai.

Flat steel

Leading Indian steel manufacturers have kept their list prices of hot-rolled coils (HRCs) and could-rolled coils (CRCs) unchanged for June sales.

While most mills have confirmed this price stability, a few are yet to make official announcements. Notably, only one mill offered a rebate of INR 500/t for May.

As of 6 June, BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) decreased by INR 100/t ($2/t) w-o-w to INR 51,300/t ($620/t). However, CRC (IS513, Gr O, 0.9 mm/CTL) prices fell by INR 100/t ($1/t) w-o-w to INR 58,200/t ($703/t). These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

The recent decline in steel prices can be attributed to a combination of softening demand and the early arrival of the monsoon season.

As per BigMint’s vessel line-up data, bulk imports of HRCs and plates continued to decline m-o-m. The cumulative import volume touched 293,922 t in May as against 306,260 t in April and 408,762 t in March.

Indian mills are not actively offering to the Middle East due to competitive Chinese offers and higher domestic realisation. Indian HRC export offers to Europe remained rangebound m-o-m due to slow domestic demand in the EU.

![]()

Leave a Reply