- Trade prices drop by INR 500-600/t m-o-m in May

- Outlook bearish amid monsoon-led demand decline

Indian steel manufacturers, both leading and new, have kept their list prices of hot-rolled coils (HRCs) and cold-rolled coils (CRCs) unchanged for June 2025 sales.

While most mills confirmed this price stability, a few are yet to make official announcements. Notably, only one mill offered a rebate of INR 500/tonne (t) ($6/t) for May 2025.

Leading steel manufacturers’ list prices of HRCs (2.5-8 mm, IS2062, Gr E250 Br) stood in the range of INR 52,150-54,000/t ($608-630/t) ex-Mumbai. CRCs (0.9 mm, IS513 CR1) were priced between INR 57,650-60,750/t ($672-708/t).

New entrants priced HRCs slightly lower, at INR 51,900-52,000/t ($605-608/t) ex-Mumbai.

Market scenario

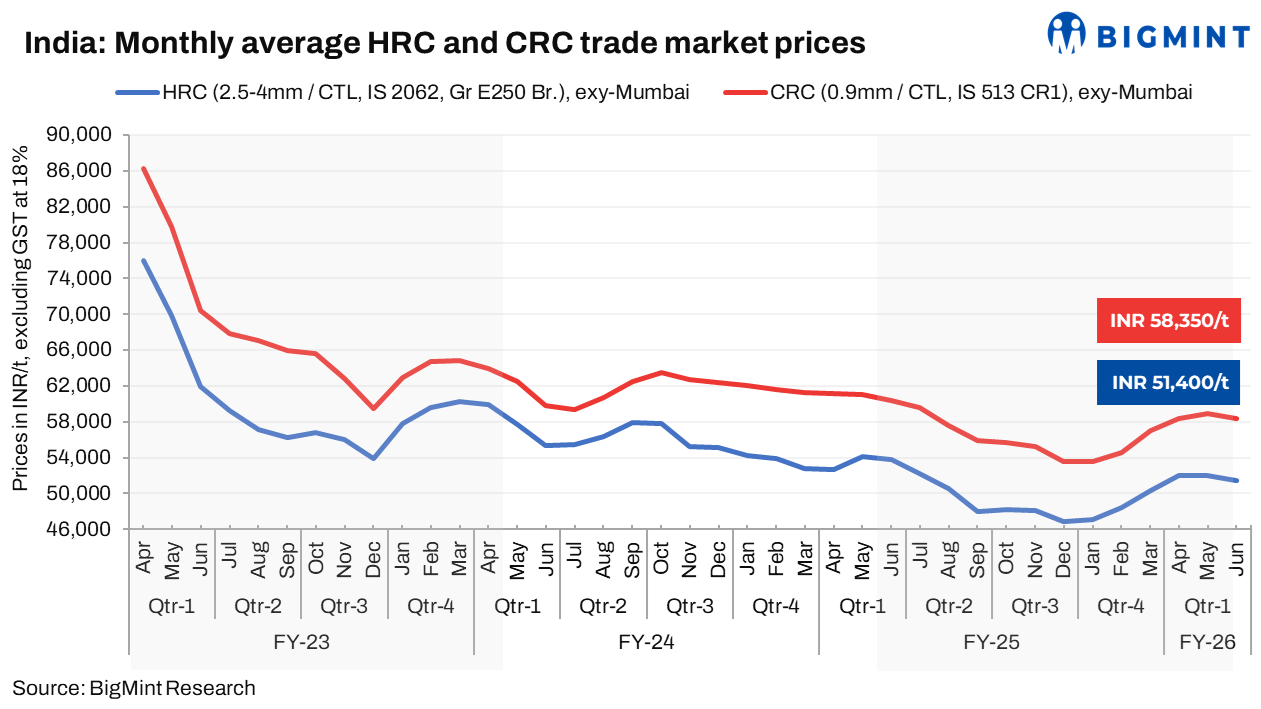

Domestic trade prices decrease m-o-m: In the trade segment, the average monthly price of HRCs decreased by INR 600/t ($7/t) m-o-m to INR 51,400/t ($599/t) in May 2025. CRCs saw a decline of INR 500/t ($6/t) to INR 58,400/t ($681/t).

The recent decline in steel prices can be attributed to a combination of softening demand and the early arrival of the monsoon season.

The early monsoon prompted market participants to reduce inventory levels by selling existing stocks. This proactive destocking was driven by expectations of decreased demand during the monsoon period.

Furthermore, as both demand and inquiries slowed, expectations of further price drops led to sellers ramping up efforts to liquidate stocks. However, buyers delayed purchases, expecting potential rebates or further reductions in list prices.

“During the month, extreme heat in the north and early monsoon across several regions impacted market activity. Labour shortages, driven by weather conditions and agricultural work, also slowed down construction and related demand. Following the onset of the monsoon, sellers are offloading material to maintain leaner inventories during the season,” a market participant noted.

Downtrend in imports continues: As per BigMint’s vessel line-up data, bulk imports of HRCs and plates continued to decline m-o-m. To illustrate, the cumulative import volume touched 293,922 t in May, while it was 306,260 t in April and 408,762 t in March.

Export market remains slow: Indian mills are not actively offering to the Middle East due to competitive Chinese offers and higher domestic realisations. Meanwhile, Indian HRC export offers to Europe remained range-bound m-o-m due to slow domestic demand.

Weekly assessment update

As of 6 June 2025, BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) decreased by INR 100/t ($2/t) w-o-w to INR 51,300/t ($620/t). Additionally, CRC (IS513, Gr O, 0.9 mm/CTL) prices fell by INR 100/t ($1/t) w-o-w to INR 58,200/t ($703/t). These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Outlook

Indian HRC and CRC prices will continue to face downward pressure. While major mills rolled over June list prices, softening demand and the early monsoon are likely to pull down trade values. Sellers will continue to intensify efforts to liquidate existing stock, while buyers may keep putting off purchases, expecting further price drops and rebates.

Leave a Reply