- Cyclones, port disruptions drag down Australian exports

- China limits imports amid struggling property segment

- India’s exports drop 47% on waning Chinese demand

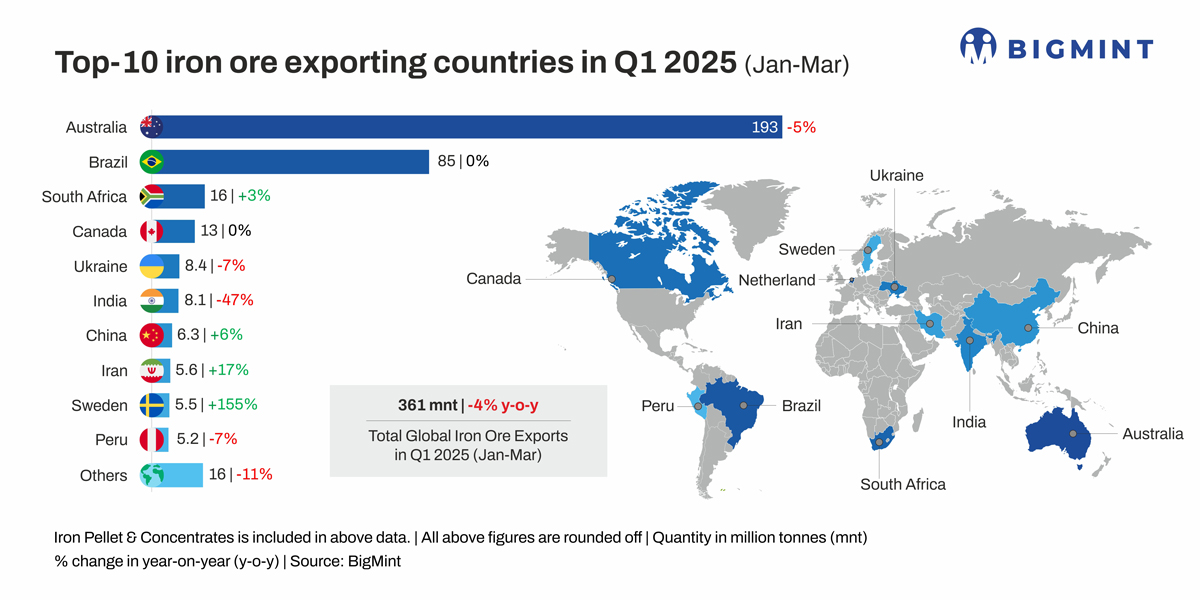

Morning Brief: Global iron ore exports (including pellets and concentrates) edged down by 4% y-o-y to 362 million tonnes (mnt) in Q1CY’25 (January-March 2025) against 378 mnt in the corresponding period last year.

The drop was triggered by lower shipments from Australia and India, while Chinese mills also showed limited interest in sourcing material. BigMint goes behind the scenes.

Factors influencing global iron ore exports in Q1CY’25

Adverse weather disrupts Australian shipments: Australia’s iron ore exports dropped 5% y-o-y to 193 mnt in January-March, which brought down the overall volume. Export activity in Australia was impeded by the destruction caused by Cyclones Sean, Taliah, Vince, and Zelia, among others. Logistics operations were affected at ports such as Hedland and Dampier, and the key iron ore hub of Pilbara witnessed severe flooding.

Global steel production inches down y-o-y: The first quarter of the year recorded a slight 0.4% drop in global steel production at 468.6 mnt, worldsteel data shows.

The drop was attributed to sluggish steel trade globally, driven by the steady export onslaught from China (volumes up 6% y-o-y in Q1) and the economic slowdown in regions such as the US, China, EU, Japan, and South Korea.

Sluggish steel demand limits China’s import appetite: China, the largest beneficiary of global iron ore imports, saw an 8% drop in iron ore and concentrate arrivals to 285 mnt in Q1CY’25, customs data shows.

While weather-related disruptions in Australia were the primary factor behind the fall, China’s domestic steel demand was also subdued, with the property segment continuing to struggle. To illustrate, the infrastructure growth rate averaged 5.47% in Q1CY’25 against 6.3% in Q1CY’24, while real estate development growth was –10% in Q1CY’25 compared to –9.2% in Q1CY’24.

In line with the demand slump, crude steel production was down 1.5% y-o-y in January-February, though the trend reversed in January-March, with a 0.6% uptick.

Other factors which led mills to adopt a guarded approach to iron ore sourcing were the government’s announcement of production cuts, as part of plans to restructure the domestic steel industry, and the tariff war sparked off by President Trump, which stirred up a storm of uncertainty.

Additionally, China’s portside iron ore inventories were higher by 10% y-o-y at 143.7 mnt in Q1CY’25. Evidently, mills tapped into these stocks while shying away from imports, considering that there was a 3% drop in volumes from Q4CY’25.

Key miners see drop in production y-o-y: Rio Tinto’s iron ore production dropped 10% y-o-y to 69.8 mnt, while its shipment fell 9% y-o-y to 70.7 mnt in Q1CY’25. Additionally, BHP’s production remained largely flat y-o-y at 67.8 mnt, while sales slipped by 4% to 66.8 mnt.

The spate of tropical cyclones in Australia disrupted operations of both miners.

Meanwhile, Brazilian miner Vale recorded a 4.5% decline in iron ore production to 67.7 mnt due to seasonal rainfall and other external and operational factors.

India’s iron ore exports halve in Q1CY’25: India’s iron ore exports plunged 47% y-o-y to 6.03 mnt in Q1CY’25, precipitated by a 48% drop in offtake by China, the largest buyer of Indian iron ore. As a result, India slipped from the 4th spot among global exporters to the 7th.

The sharp export decline could also be attributed to weak sentiment in China, stemming from the tariff tensions. Additionally, domestic crude steel production climbed up by 7.5% y-o-y to 40.09 mnt last quarter, which led to increased domestic consumption of iron ore.

Outlook

The decline in steel consumption worldwide is likely to continue weighing on global iron ore demand and, consequently, exports. Reports suggest that China’s crude steel production will taper off in line with the depression in demand, which may slow down the country’s iron ore procurement. Other hindrances include weak mill margins, high portside stocks, escalating trade tensions with the US, and the traditional construction off-season from June.

Meanwhile, with operations normalising at major Australian miners and production guidances remaining unchanged, a supply glut may materialise. Consequently, prices are expected to move below the $100/tonne (t) mark in the next few quarters. This may lead to opportunistic purchases, but overall, demand will remain need based.

Leave a Reply