- Chinese billet prices gain despite weak market

- Turkish scrap offers decline as Eid approaches

The global billet market showed mixed trends in week 23 of CY’25. The Asian steel billet market remained subdued amid weak demand and a cautious outlook, particularly in China. Seasonal slowdowns and logistical challenges impacted buying across the region. While East and Southeast Asia saw relatively stable prices and steady export activity, some markets experienced tight supply and soft demand.

East Asia saw slight price declines amid weak activity, while Southeast Asia, CIS, and South Asia witnessed stable pricing. The Middle East experienced a minor price uptick, though export demand remained weak.

On the supply side, regions such as North Africa and Southeast Asia announced strategic investments in billet production and downstream integration to boost self-sufficiency. Overall, market activity is expected to stay quiet in the near term as mills prioritise margin preservation amid limited demand. However, despite subdued demand in the short term, long-term prospects are supported by capacity expansions and efforts to strengthen regional supply chains.

Turkish scrap prices erode amid trade slowdown

Imported deep-sea ferrous scrap HMS (80:20) prices in Turkiye declined by $6/tonne (t) w-o-w to $341/t CFR, as trading slowed amid weak finished steel demand and the approaching Eid al-Adha holiday. Mills paused bookings, preferring to conserve cash in a high-interest-rate environment and await clearer post-holiday market direction. While scrap availability remains sufficient, mills also need to secure material for July.

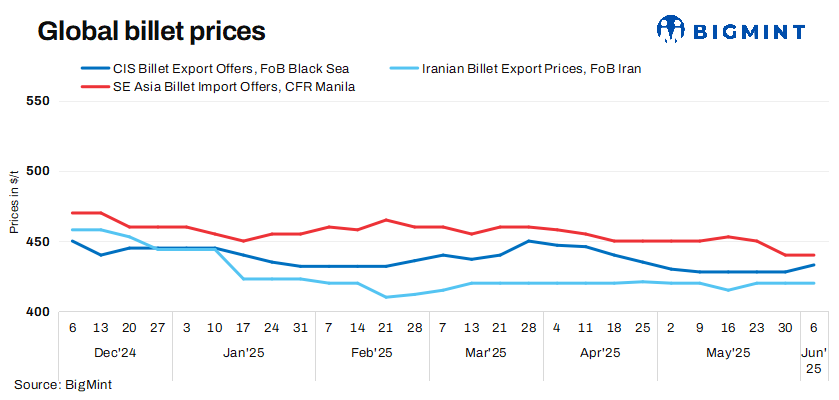

Market highlights

- Vietnam’s steel market sentiment remained weak this week amid seasonal slowdown and limited BF-route billet export offers. While domestic players wanted to increase prices, with importers flooding the market at cheaper rates, buyers began to favour imports, with Indonesian-origin billets emerging as the preferred option. Around 40,000 t were booked at $445/t CFR, sources informed BigMint.

- Indonesia’s billet market remained under pressure this week amid weak demand and a holiday-related slowdown. As per reports, Chinese-origin 5sp 150-mm billet offers stood at $445-450/t CFR Jakarta, but interest was limited due to reduced infrastructure spending. Sellers offered 3sp 150-mm billets for September shipment at $428/t FOB, with some talks indicating trades near $425/t FOB.

- In the Philippines market, billet offers for CFR Manila stood firm w-o-w at $440/t CFR as of 6 June. Market activity was limited, as buyers stayed cautious. Meanwhile, futures continued their uptrend this week, weighing on market confidence.

- The Russian billet index, FOB Black Sea, inched up by $5/t to $433/t w-o-w.

- Iran’s semi-finished steel export market saw little movement this week. Billet offers for 130 x 130 mm 3sp, FOB Bandar Imam Khomeini, remained unchanged w-o-w at $420/t. The domestic market also showed limited activity amid continued logistics disruptions and severe power outages.

- Chinese billet prices saw a slight uptick of RMB 20/t ($3/t) w-o-w to RMB 2,910/t ($405/t), including 13% VAT, on 6 June compared to 30 May, despite prevailing market weakness. The modest price increase was supported by improved sentiment following recent China-US talks and a slight rebound in raw material prices such as iron ore and coking coal. Moreover, SHFE rebar futures recorded a marginal gain of RMB 14/t ($2/t) w-o-w, closing at RMB 2,975/t ($414/t).

Leave a Reply